During the Trump Administration, significant tariffs were launched against China to curb the flow of Chinese imports into the United States and assist in trade-deficit reduction. These tariffs were continued by the Biden Administration, with the stated rationale that they could be used as leverage against China in future negotiations. Unfortunately, we find that these tariffs have not effectively reduced the U.S. dependence on Chinese goods, particularly intermediate inputs. It is also unlikely that the new round of increased tariffs from the Biden Administration, although targeted to specific industries, will have a significant impact on Chinese imports, or diminish a reliance on goods originating from China in the mid to short run.

At first glance, it may appear that the tariffs have been successful, as the United States has reported that Chinese imports fell by $100 billion between 2020 and 2023. However, a February 2024 article from The Economist suggests that declines in Chinese imports may not be as great as initially reported. The article states that the Chinese government reports exports to the United States rose by $30 billion between 2020 and 2023. The article goes on to say, “If China’s data are correct, the country’s share of American imports has still declined, but by much less.”

How is this so? In addition to incentives by interested parties to report favorable outcomes, firms are finding ways to circumvent the tariffs. At the moment, U.S. firms are understating imports from China by 20% to 25%, and prices are rising due to increases in transaction costs along a growing network of partners willing to offer alternative routes for Chinese goods. As a result, it becomes increasingly difficult to identify the effectiveness of the tariffs.

When the Trump Administration tariffs were launched against Chinese imports, China quickly created an additional tier in the supply chain by shipping through middlemen in other countries. This strategy created a buffer against the tariffs, passed through costs, and made money both for China and the middlemen. During the same time, China has encouraged exports by cutting taxes on their exporter firms. Thus, the White House’s attempts over two presidencies to “derisk” trade with China, despite being the cornerstone of its foreign policy, is not working.

For example, U.S. officials have been particularly keen to limit imports of advanced manufacturing products from China. Between 2017 and 2022, the share of imports arriving from China did indeed decline by 14% while imports from more “friendly” countries—such as Vietnam, Taiwan, India, Thailand, and Malaysia—have grown. However, the share of Chinese imports into these countries is rising fast, as China is also establishing subsidiaries in these countries and shipping intermediate parts and components to and through these touch points. “Tariff-jumping,” or production within a friendlier environment, is a well-known phenomenon in global trade circles.

The rerouting of shipments through countries that are U.S.-friendly has implications beyond changing trade routes. China has increased its share of exports to the ASEAN (Association of Southeast Asian Nations) bloc in 69 of 97 product categories. Likewise in Mexico, 40% of offshore investments in automotive manufacturing comes from China, and China is exporting more than twice as much volume to Mexico as it did five years ago. The newest tariffs proposed by the Biden Administration include tariffs on electric vehicles of 100%, those on steel and aluminum products of 25%, and a doubling of the rate on semiconductors to 50%. These moves will probably further encourage “friendshoring” activities by Chinese firms.

Control of maritime trade

Moreover, the Chinese government’s influence and control over global maritime trade touch points has also become pervasive. China resembles a massive mercantilist holding company that competes with the outside world while controlling supply and distribution within its borders. The country’s State-owned Assets Supervision and Administration Commission of the State Council (SASAC) is the world’s largest economic entity as of 2021 and controls 97 centrally owned companies with a vast constellation of subsidiaries. This structure is replicated at the provincial and local levels, leading to even more centrally controlled businesses operating in maritime markets.

In a communist country, the state also controls the banks that finance and lend money to producers, thus participating in all aspects of the value chain. In terms of the maritime shipping industry, this means that the Chinese government controls the supply and distribution of key raw materials used to build ships, such as the iron and coal that is converted to steel, as well as the enterprises that build ship components. In addition, the Chinese government exerts control over terminal services, container handling, and logistics, as well as part ownership of terminal operations control software.

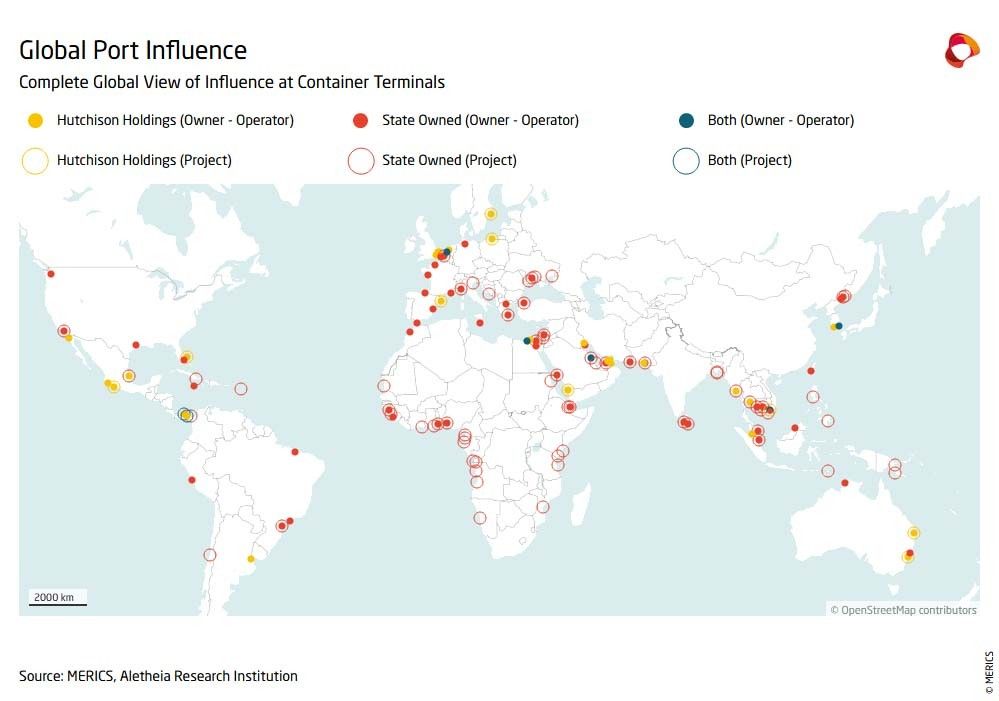

Through SASAC, the Chinese Communist Party (CCP) also controls shipping giant COSCO (the China Ocean Shipping Corporation), one of the largest operators of ships and container terminals in the world (think of a state-run Maersk). Further investment to private firms also takes place through Hong Kong entities such as Hutchison Holdings and its subsidiaries. Although Hutchison companies are not officially state-owned, COSCO is now a part owner in a number of their operations.

Several Hutchison Holding subsidiaries and SASAC enterprises have been successful in establishing control at deep-water terminals around the world by winning concessions and terminal leases. (See Figure 1.) This position then extends inland to other supply chain touchpoints as the benefits of vertical integration are sold to host countries on the grounds of cost savings. In addition to operating the terminals and financing the development of ports, Hutchinson and SASAC offer the technology and equipment to manage the terminals and provide resources for industrial projects such as inland logistics channels that include railways, roads, and cross-docking stations for truck shipments. At that point, Chinese state-controlled enterprises are in a position to exert a significant amount of economic and political pressure on host economies. This influence can then extend to neighboring countries. For instance, China developed a large port in Angola, and then quickly followed up by extending rail lines and truck routes through Zambia to Congo to export cobalt from mines that Chinese firms also controlled. Although China lost control over this $1.2 billion port in 2023, Chinese firms still control many of the supply chain touch points in the hinterland.

In many cases, Chinese-affiliated firms maintain control of the ports they develop after becoming operational. Controlling the port means controlling the entry points to hinterland operations and the flow of goods out of the host country. This control can amount to a great deal of cost savings for participants along the vertically integrated supply chain and thus, can shift business away from natural low-cost trade partners. Data analysis by Aletheia Research Institution has found that when Chinese firms operate all terminals in at least one port, the following trends can be identified:

- Exports to China increase by +76% after 12 years,

- Imports from China increase by +36% after 12 years, and

- Exports to the rest of the world decrease by 19% after 12 years.

Figure 1 shows the growth in China’s control of ports, particularly in the European Union (EU), Middle East, and Africa in a geospatial projection developed for a report by MERICS and Aletheia Research Institution. This is a shocking level of growth; it also illustrates that Chinese firms have a number of options available to alter the potentially negative effects of tariffs. The United States’ dependency on Chinese intermediaries for supply chain inputs essentially renders tariffs ineffective, and workarounds through an international network of logistics channels make them insufficient for attaining the U.S. strategic objectives.

FIGURE 1: Global Port Influence

Ineffective policy

In short, tariffs have had almost no effect on imports from China, nor are they likely to in the future. At the moment, we are seeing an increase in the costs of protection without the concomitant payoff in industrial development and consumer welfare. Although tariffs will reduce direct shipments from China and provide U.S. firms with production opportunities, it may be too little too late. Chinese inputs will still be needed for manufacturing or reliant firms may go under. More importantly, scalable production growth for U.S. firms may be impossible in many industries due to first mover advantages. The only way out for U.S. firms would be to innovate in ways that reduce their dependency on specific Chinese provided inputs.

In expectation of further U.S. trade protection measures, China has continued to increase its hold on global supply chains. When Chinese firms operate global supply chain touch points, they increase power and lock in countries to their value chains. They also divert trade from other natural trade partners by subsidizing exports and reducing the transaction costs of transport. While countries benefit from the partnership with China in the short run, they become locked into a close partnership that, in the long run, may not always be to their benefit. It is very difficult to pivot away from China once you commit—a lesson many regions will begin to understand soon. At the moment, it is a difficult choice between greater protection and higher prices, or acceptance of low-cost subsidies at a cost of national economic independence.