U.S. business logistics costs for 2023 dropped 10% to $2.4 trillion, or 8.7% of last year’s $27.4 trillion gross domestic product (GDP), according to the “2024 State of Logistics Report” released today. The annual report—which is produced by the analyst firm Kearney for the Council of Supply Chain Management Professionals (CSCMP)—says this is the first time that costs have declined since the start of the pandemic four years ago.

“This was not unexpected,” said Josh Brogan, Kearney partner and lead author of the report, during the press conference announcing the results. “After the initial impacts of COVID were felt in 2020, we saw a steady rise in logistics costs, even in terms of total GDP. What we are seeing now is a reversion more toward the mean. We are starting to see a reversion in certain [transportation] modes toward prepandemic levels of cost.”

Now in its 35th year, the “State of Logistics Report,” which is sponsored by third-party logistics service provider Penske Logistics, provides a yearly review of the health of the primary logistics subsectors and of the industry as a whole.

According to Brogan, the biggest drop in costs was seen in asset-heavy transportation sectors, such as air cargo and ocean shipping, driven mostly by rate decreases. While modes such as motor freight have also seen decreases due to soft volumes and ample capacity, these decreases were not as large as air and water transport. Additionally, storage costs dropped last year with the market seeing a reduction in rents for the first time since the pandemic.

“By and large we are seeing reductions in logistics costs across the board,” summarized Brogan.

Breakdown by mode

The 60-page report, which is free for CSCMP members and $299 for nonmembers, breaks down these overall costs by mode and sector (see chart below) and provides an in-depth analysis of expectations for the coming year.

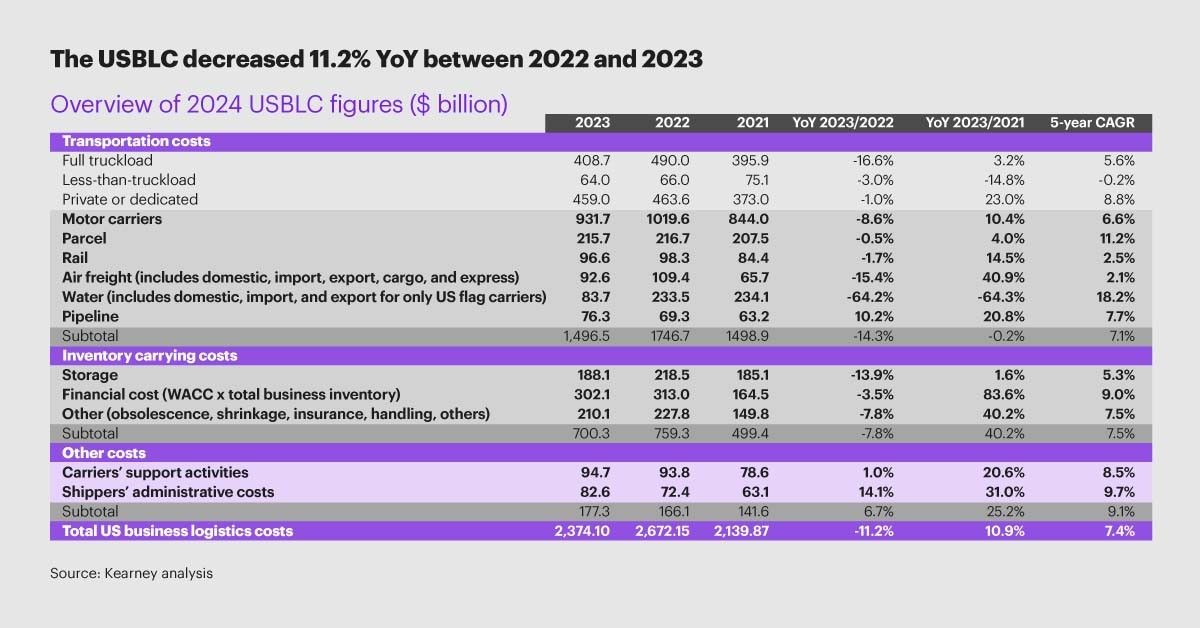

FIGURE 1: The USBLC decreased 11.2% YoY between 2022 and 2023

Some key insights include:

- Motor carriers: Costs decreased 8.6% in 2023 as the downturn in consumer demand, plus a lingering surplus in capacity, led to rates remaining steady and lower than in the past few years.

- Parcel: Costs held relatively steady with a slight 0.5% drop. Volume fell for UPS and FedEx, as shippers looked to use more regional and local carriers.

- Rail: The largest railroads saw a 2% decline in revenue and an 11% decrease in operating income due to a drop in intermodal volume, higher fuel prices, and greater labor expenses.

- Air freight: Costs dropped by 15.4% as passenger traffic returned to normal, bringing online more belly capacity for transporting freight. In addition, some ocean carriers added air freight capacity in effort to broaden their offerings.

- Water: Waterborne freight saw sluggish demand and excess capacity. As a result, shippers were able to negotiate better contracts, leading to a 64.2% decrease in costs.

- Storage: Demand for new warehouse space has cooled and rents have dropped, causing costs to decline by 13.9%.

Future outlook

Looking ahead, the market will continue to favor shippers over transportation providers for the near term. The report recommends that shippers take advantage of the opportunity to lock in lower rates and diversify their carrier portfolios. The report’s authors do anticipate that capacity will begin to tighten in the second half of the year, resulting in an upturn in rates.

In general, both shippers and providers will have to contend with a muted level of global economic growth. Economists are predicting that the global GDP will grow by 2.5% in 2024, down from 2.7% in 2023. Additionally military conflicts and geopolitical tensions are putting stress on global supply chains, adding costs and friction. As a result, many companies are looking to “rewire” their distribution networks. These redesign efforts are driven not just by cost concerns but also by efforts to enable greater capacity, agility, and flexibility.

"The interesting part of the equation is how much of that is going to be onshoring/nearshoring versus more friendly offshoring," said Brogan. "There isn’t a consensus, there’s a lot of debate about what those strategies mean and obviously that has big implications for overall logistics costs in the long and medium term."