The U.S. economy will end 2024 with weaker demand being met by largely adequate inventories. From a supply chain perspective this means that shippers can expect sufficient freight capacity, with continued adequate distribution center and warehousing availability.

In the last few years, transportation and logistics services providers added capacity in response to the boom in the purchase of goods and shipping during the pandemic. Those capacity additions remain, especially in trucking, where carriers have been slow to downsize or exit the industry, leading to excess capacity and low rates.

Weaknesses in manufacturing, housing starts, and business fixed investment are among the combination of factors leading to slower economic growth in the second half of 2024. However, low unemployment and resilient consumer spending means that the economy is still experiencing wage and price inflation above the U.S. Federal Reserve Board’s target of 2%.

Due to persistent inflation, especially in services, we expect that the Federal Reserve Board won’t reduce interest rates until December of 2024. As a result, capital costs will continue to be elevated for longer than expected. The slower economic growth will provide a headwind to freight demand that derives from consumer and business spending, manufacturing, and inventory building.

Slowing economic growth

The S&P Global Market Intelligence 2024 U.S. macroeconomic baseline forecast is for real gross domestic product (GDP) growth of 2.5%, about the same as for 2023. However, the pace of growth will slow through the rest of the year, where the relatively strong first two quarters of the year will be followed by two quarters averaging 1.7% annual growth. No recession is in the forecast, but the weakness in the U.S. economy will continue next year with real GDP growth of 1.6% in 2025, primarily due to the Federal Reserve Board focusing its monetary policy on reducing inflation to its 2% target.

Consumption in the economy is a key driver of freight demand, especially goods consumption. (Although services consumption does indirectly generate associated freight demand.) Consumption is now forecasted to slow to a 2% annual growth rate for the third and fourth quarters of 2024, following an average growth of 2.7% in the first two quarters of 2024. Sustained employment levels and growth in equity and home values supported household consumption spending in the first half of the year. However, we anticipate that consumption levels will moderate as the lagged effects of higher interest rates and declining residential investment dampen consumer demand. The inflation fight is forecasted to be won in 2025 but at the cost of below-potential economic growth, including unemployment rising to 4.2% by the end of 2025.

Interest rate increases are reducing consumer demand by raising the cost of credit. For durable goods purchases, such as autos financed with loans or homes financed with mortgages, lender limits on consumers’ debt service-to-income ratios constrain purchases consumers can qualify for. The higher mortgage rates will lead to a downturn in residential fixed investment in the second half of 2024. Housing starts will end the year at 1.4 million, below the 2023 level. The weakness in residential investment will be accompanied by weaker associated furniture and home furnishings markets.

Interest rate increases are affecting business, where the higher costs of capital reduce firms’ capacities to afford new plants and equipment or invest in substantial safety stock inventory. Business fixed investment is expanding but at a slower pace, forecasted to grow 2.9% in 2024 compared with the 4.5% pace of growth seen in 2023. For some businesses that are dealing with higher costs from inflation, increased capital costs can result in a negative cash flow or even insolvency. Some new-entrant truckers, who paid high prices for new equipment in the 2021–2022 boom, have become vulnerable in this higher-interest rate, lower-growth environment, which has led to contractions in for-hire trucking capacity. Trucking supply, however, still exceeds demand.

Weak U.S. freight outlook

Based on the forecasted demand for goods and inventory levels, we expect U.S. freight volumes to start mixed and end the year mostly weaker. The pace of consumption and inventory rebuilding seen in the first half of 2024 won’t be sustained all year, leading to demand and freight tonnage growth less than GDP growth. The S&P Global Transearch baseline forecast overall is for freight tonnage to increase 1.7% for 2024.

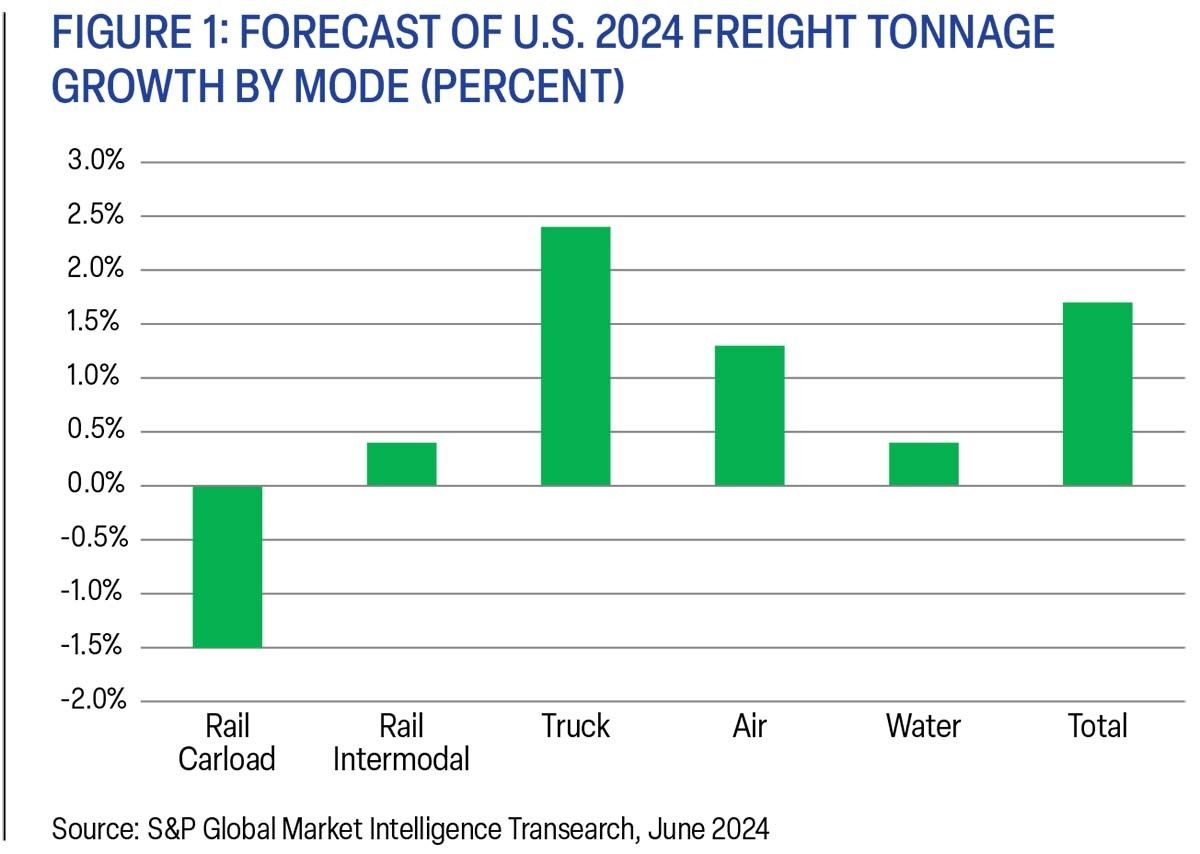

Not all freight modes have the same prospects. As Figure 1 shows the range of modal tonnage growth forecasts vary from a 1.5% drop in rail carload tonnage up to a rebound of 2.4% growth in total truck tonnage.

FIGURE 1: Forecast of U.S. 2024 freight tonnage growth by mode (percent)

Carload rail tonnage will suffer from the drop in volumes of the number-one carload volume category of coal. This drop will not be offset by modest growth in manufactured carload commodities, such as chemicals and autos. In contrast, intermodal rail experienced strong growth in the first half of 2024 from growing imports, inventory restocking, the import market share shift back to West Coast container ports, and an early start to peak season. However, intermodal rail tonnage growth for 2024 as a whole will be limited by competitive domestic trucking rates and service times.

The baseline trucking demand forecast is for 2024 tonnage to grow by 2.4%, driven by a 2.6% growth in the substantial private trucking sector. Meanwhile for-hire truckload and less than truckload (LTL) will see more moderate recovery in 2024 volumes.

Air cargo tonnage growth is forecasted at 1.3%, reflecting slowing growth in e-commerce, despite a surge in e-commerce imports in the first half of 2024. The maritime baseline forecast is for a 0.4% growth in tons compared to 2023 levels due to declines in coal tonnage plus concerns with water levels for the Mississippi River system and the Panama Canal.

What this means for shippers

For supply chain managers, the baseline freight forecast implies continued market power, qualified by instances where carrier capacity adjustments and their increased fixed operating costs may limit rate advantages to shippers. There remain threats of temporary operating capacity limitations, such as have been experienced recently at West Coast ports for import rail shippers or from the risk of potential disruption at East and Gulf Coast ports with the expiration of the International Longshoremen's Association (ILA) contracts in September. However, most supply chain managers will see domestic freight carrier performance and rates improve compared with where they were from 2020–2022.