After the pandemic hit in 2020, many companies realized how vulnerable their supply chain operations were and put a tremendous amount of investment into supply chain technologies. However, to for these investments to be effective, companies need to set clear objectives and success criteria up front and be ready and willing to make the changes needed so they can achieve these desired outcomes. Indeed, companies should be selective about what investments to make, as not every technology is right for every company. And more importantly, companies should strive to not just execute a technology implementation but also monitor its effectiveness.

To see what progress has been made in terms of supply chain tech advancements and what more is still needed, the consulting company PwC surveyed over 300 executives responsible for supply chain and procurement operations. PwC’s “2023 Digital Trends in Supply Chain Survey” revealed that many of the companies surveyed are using technology to improve their supply chains. Here are some quick insights to consider as you evaluate your own progress.

Where are we with investments?

The vast majority of companies surveyed by PwC reported that they are seeking to increase their digital supply chain capabilities (see Figure 1). For example, 84% of executives said that they had either partially or fully adopted a cloud-based common data platform, which is unsurprising given the steady evolution of cloud solution providers and the expanded reliability of cloud solutions. Other popular technologies—including the internet of things, scanning and intelligent data capture (such as optical character recognition), and third-party spend analytics tools—also ranked among the top investments and adaptations for supply chain leaders. In terms of future spending, artificial intelligence (AI) and machine learning are seeing the highest planned investments, with 22% of executives saying their companies plan to invest at least $5 million in those technologies.

FIGURE 1: Technology adoption levels and future investment areas

When you dig further into the data, you can see that different industries have different investment priorities. For instance, there are much higher rates of adoption and planned investment in AI and machine learning in technology, media, and telecommunications industries than in other sectors. Meanwhile, energy, utilities, and resources companies have adopted and/or are investing in drones more than other sectors.

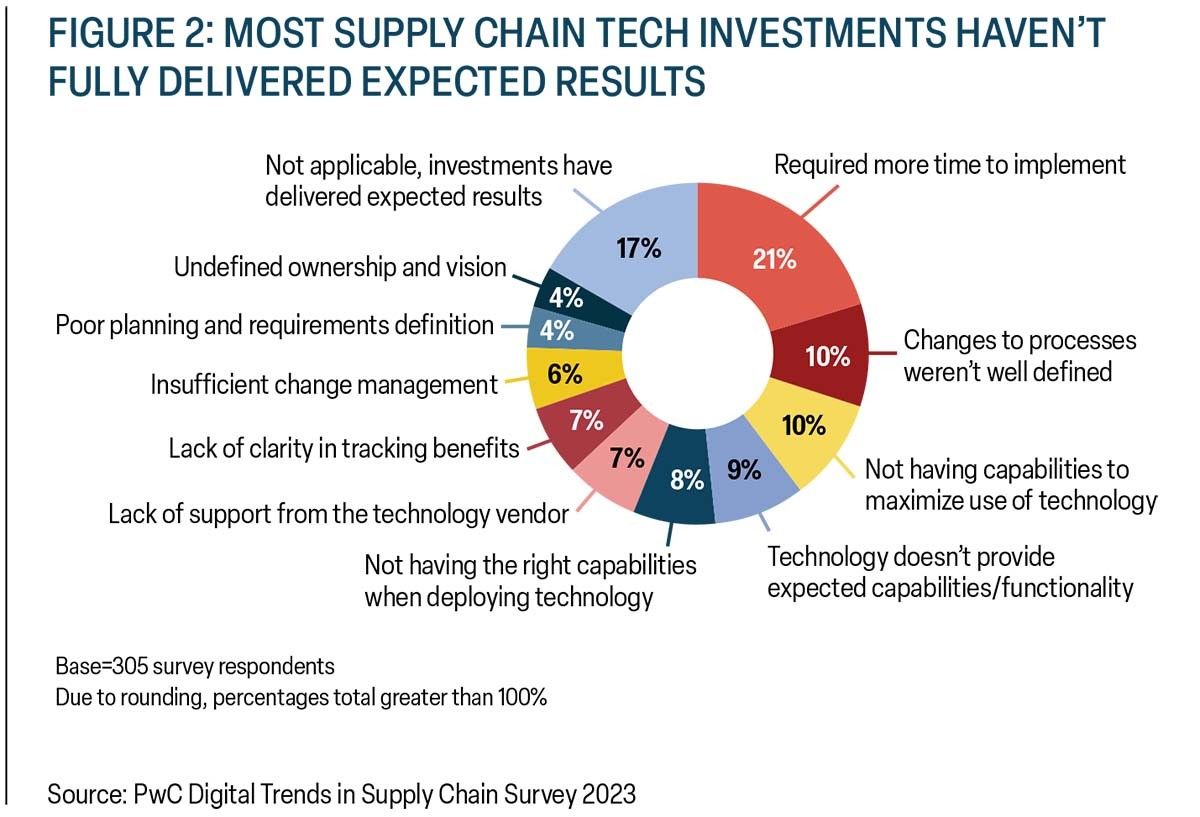

While adoption levels are high, many companies are not yet thoroughly satisfied with their implementations. (See Figure 2.) In our survey, only 17% of respondents said that their technology investment had delivered the expected results. For the majority of respondents, the issue did not lie with the technologies themselves; only 9% indicated that the technology didn’t provide the expected capabilities/functionality. Instead, many of the answers indicated that the problem lay with how the company was implementing those technologies, be it not having adequate time, the necessary capabilities, or change management skills.

FIGURE 2: Most supply chain tech investments haven't fully delivered expected results

People first

Another key challenge to getting more value out your tech investment is whether employees have the right skills and motivation to effectively use the new digital tools. According to the survey, 31% of executives said that a top challenge to digitizing their supply chains was getting employees and teams to work differently, perhaps through using a mix of new tools and processes while also maintaining existing ways of working. Additionally, 25% said they had difficulty attracting, developing, and retaining the “digital native” talent needed to transform their supply chain.

In fact, more than two-thirds of respondents expect digitizing their supply chain to require some upskilling of employees. Responses to the 2023 survey indicate that companies may be planning to work more with current employees rather than recruit new talent. Compared to 2022, fewer executives say they will need to add more employees overall, and more say they will retrain employees for different jobs because their current roles will no longer be necessary.

For their part, employees say they are eager to learn more about innovative technologies in the workplace. In PwC’s recent “Global Hopes and Fears Survey,” 52% of workers selected at least one positive statement about the impact of generative AI on their career—that it will increase productivity, bring opportunities to learn new skills, or create job opportunities.

However, only 7% of supply chain executives said digital upskilling was their top priority. This highlights the need for organizations to invest in training, to clarify and measure what “new ways of working” really entails, and to make the necessary process changes so that they can make better use of their technology investments.

Technological innovations will likely persist, so upskilling your employees should also be an ongoing process that is refreshed and re-evaluated regularly. Digital transformation should be approached with a people-first mindset. Training should focus not just on helping employees better perform their day-to-day jobs but also on adapting to new ways of working and executing strategic goals.

Companies should go beyond simply teaching employees how to use the new technology tools. They should also help them understand why these tools will make their jobs better and what the tools’ full capabilities are. This sort of instruction can be provided through use cases, situation scenarios, and practice exercises. In this way, companies can emphasize outcomes and value-added results and not just implementing a new tool or way of working.

Investing for the long term

One challenge that many companies face is transformative actions continue to compete with more traditional priorities. Many supply chain leaders are still tackling day-to-day fires while trying to activate a new way of working. Finding the bandwidth to make transformative changes is challenging. Leaders may find themselves leaning into cost-related or more near-term initiatives rather than long-term ones. For instance, more than half of respondents (51%) said optimizing costs was a top objective when investing in technology.

It is less evident how companies are factoring their digital investments into long-term business strategies, if at all. Although 53% said that driving growth was a top objective of their supply chain technology investments, other objectives that have the potential to advance returns on digitization long term were far less popular. Less than one-third (30%) cited exploring new innovations and only 16% said implementing a different business model was the top objective for their technology investments.

Another long-term focus for technology investment should be risk and resilience, especially given the disruptions of the last few years. Indeed, 86% of survey respondents either agreed or strongly agreed that their company should invest more in technology to help identify, track, and measure supply chain risk. However, just 34% of operations leaders cited increased resilience as one of their top objectives when investing in supply chain technology. These statistics suggest that companies are either considering investments in the context of current and traditional definitions of risk or have not yet thought about how to merge the intent of wanting to do broader risk management with the technology that will allow them to do it. Either way, this gap should be closed.

That’s not to say that companies should only focus on unlocking long-term growth and not on cutting costs. Rather both should be happening simultaneously, so that they can help feed each other. Technology often is at the heart of that. Solutions today can not only address some of your current issues but also evolve to enable the kind of business you will need to have in the future. Investments made today are a “cost,” but they will often help save money in the future. More importantly, these are investments in capabilities that will likely be required for the future. It can be beneficial to have something that can fit your purpose now and in the future, so that value capture can be sustained and growth can be properly supported and achieved.

More thoughtful implementation needed

If you have not already done so, now is the time to reset your technology enablement strategy. Make investments based on your company’s needs, so you can set up your people for success and help them take advantage of digitalization implementations. Examine not only what has worked but dig into why investments haven’t worked. Be honest about the potential gaps in planning, the quality of execution, and the effectiveness of leaders and staff as well as how well the solution delivered versus what was promised.

Companies that begin to think smarter about their tech investments and consider these strategies in tandem will often be more prepared to deal with disruptions, get a higher return out of their investments, and help to capture the growth opportunities that digitalization has to offer.

{kind=link}