To achieve global scale, companies need to design their supply chains to buy globally but execute locally. Not many companies have cracked this code. One company that has developed a unique approach to this challenge is Carter's Inc. (also known as the William Carter Co.), a U.S.-based manufacturer of children's clothing, gifts, and accessories. Sold under the Carter's and OshKosh B'gosh brands, the garments are merchandised at 600 company-owned retail stores as well as at thousands of department stores and some of the country's largest retailers.

The company's operations are complex. To satisfy demand, Carter's operates out of five domestic and international distribution centers, handling approximately 31,000 stock-keeping units (SKUs) at each location. It ships approximately 400 million selling units consisting of 700 million manufactured units per year. The company leverages global sourcing strategies to buy products at a lower cost, while deploying some unique process logic to drive mass customization during the assembly processes. Because of its success, Carter's was recognized as one of 15 companies in Supply Chain Insights' 2016 list of "Supply Chains to Admire."

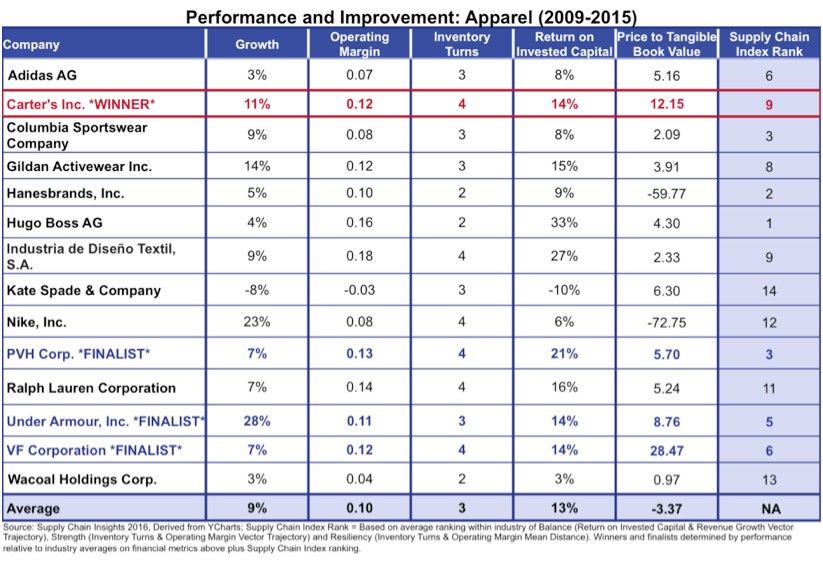

To meet the criteria for the 2016 Supply Chains to Admire list, for the period 2009-2015 companies needed to score better than their industry peer group's average on the performance metrics we call "Supply Chain Metrics That Matter": growth, inventory turns, operating margin, and return on invested capital (ROIC). They also had to show a higher level of improvement than two-thirds of their industry peer group and have driven a high level of shareholder value, expressed as "price to tangible book value." As shown in Figure 1, Carter's Inc.'s scores for the "Supply Chain Metrics That Matter" are significantly better than those of its peer group.

To learn more about how Carter's earned its spot on the Supply Chains to Admire list, we interviewed Peter Smith, the executive vice president of supply chain.

Q: You were recognized as a winner in the 2016 Supply Chains to Admire. What drove Carter's to achieve the level of improvement it did?

A. Necessity is the mother of invention. We manufacture 700 million pieces of clothing and service every channel in the U.S. along with international markets. The diversity is rising. This drove a need for complexity management and mass customization like I have not seen elsewhere. This market demand has spurred Carter's to create strategies, systems, and processes to focus on low prices and competitive marketplace distribution.

Today, we do not have a single, all-knowing, all-seeing, and seamless world-class information technology (IT) system. It just does not exist. This is not a place where one great "killer app" or technology has slayed the dragon, but the systems are malleable. Driven by the business, our teams in information technology/information systems ... found creative ways to invent solutions. Is it elegant? No. However, it is really effective for our processes.

In my experience, technologies like SAP are rigid. They are too inflexible for us. We need agility. As a result, Carter's runs an assemblage of systems focused on agility. They are modified collectively to deal with our complexity. For example, we created a bit of magic by repurposing our ERP dimension code to carry information about final retailer specifications in addition to style, color, and size. ... [The Carter's dimension code carries information on the pack size, retailer assembly instructions, and late-stage customization, It is assigned at a lot level when the product is cut to be assembled. This is months after contracting for third-party manufacturing.] This allows us to get the benefit of leveraging our purchase orders of 1 million units and manufacturing efficiency [while also using] dimension codes attached to the style defining the retail unit. We can purchase in large lots, postpone, and then pack out based on dimension codes. This gives us both economies of scale and flexibility.

Let me explain how this works. When the units come off the final assembly line, the third-party manufacturing company applies the value-added services like tagging and packaging, and then packs them based on the retailer's shipment-ready requirements. We pack once for the destination, and 90 percent of the units are never touched again. Customization [such as providing tagging, wrap, boxing, labels and hangers and more] happens as part of the manufacturing process, not in domestic distribution centers. We pull off this level of efficiency every day.

Q: How do you manage complexity?

A. It is a combination of strategy, people, processes, and systems. We are an international company supplying international trade. We desire and work toward postponing decisions about the allocation of finished units among our wholesale customers, our own 700 retail stores, and Carter's e-commerce [channel] to optimize inventory utilization. Once you have put on our retail tags, you have locked in the inventory. We do things downstream to improve flexibility and inventory-utilization efficiency. Multichannel distribution requires getting the most visibility possible. Our processes strive to recognize the uncertain demand in the world we live in and make the best of that reality.

Q: What is your next-generation supply chain strategy?

A. There is a significant amount of distance that we [still have to] go. ... We would like to get ever more granular through better postponement.

We are also trying to embrace all of the data around us. We have migrated planning and forecasting from big Excel spreadsheets to a cloud-based environment [in order] to process more data and data elements. We are in the early stages of using this "big data" environment. I am advocating that the organization lean into and embrace the cloud platform and tools. Ultimately the most efficient use of inventory relies upon being able to optimize the use of [our] units from the individual store shelf (at a wholesale partner's store or in our own retail store) all the way back up the chain so that we never miss a demand signal wherever and whenever it presents itself. We looked long and hard at packaged tools and concluded there's not enough flexibility, scalability, and speed ... in the packaged tools on the market. We are now in an incredibly powerful system [that is] scaled for demands larger than I think we'll throw at it, but [this system] will never limit us.

The strategy is simpler to say than to execute, but in a nutshell, it is better decisions, lots of postponement, mastering ever-increasing complexity in a leveraged way, and using all the data that we can get our hands on. .... I believe in the Internet of Things and see great opportunities to "connect the dots" of data that may impact demand and create opportunities for the companies that are agile enough to respond.

Q: How do you define supply chain excellence?

A. When I think of supply chain excellence, I believe that [it means] we never miss demand. Excellence occurs when there is minimal inventory ownership ... but the company never misses demand. Strategically, I have declared that as Carter's continues to grow, it is my responsibility every year to consume a smaller and smaller percentage of sales. If the supply chain total cost of ownership of sales is x, I want a downward tilting line for supply chain costs. Survival means that we must invest in big data analytics, customization, and postponement.

Q: Any insights on how to build next-generation supply chain talent?

A. We live in a world where the rate of change is the fastest I have ever seen. To stay current, we do "reverse mentoring" here. I am lucky because I have reverse mentoring with my 20-something[-year-old] kids. So I get a double dose of insights into millennial thinking.

One of the distressing things about [the apparel] industry is we are not [as] mature ... [in] career mapping and organizational development [as] I believe other fast-moving consumer goods companies [are]. I think the Procter & Gambles of the world "manufacture" their next-generation leaders. I have not seen this done well in the apparel industry.

The supply chain is so diverse in the things that we do, [but] as an industry we are poor practitioners of building next-generation leaders. Too many people get stuck in silos. Although they become subject-matter experts, they are "a foot wide and a mile deep." ... In my estimation, future supply chain leaders need to be subject-matter experts, or nearly so, in multiple disciplines. That happens by luck and chance or by great career mapping. I like the certainty of the latter.

Manufacturing the next generation of great supply chain leaders is expensive and requires commitment. I think this dedicated approach to building manufacturing leadership drives winning strategies, and I hope to continue to make it come to life within Carter's.

Q: If you could wave a magic wand and get anything you want, what would it be?

A. It would be a dedication to talent development, as I spoke of before. This should start early. I am fond of the apprentice programs used in Europe and the opportunity to get exposure in business they provide.

In a totally different vein, a year ago there was the buzz about the Internet of Things. We suffer from buckets of data that are not easily accessible or usable in different venues. It's still hard to get, collate, and standardize information for forecasting. Data is hard to get, hard to believe, and hard to use. [We need] real-time, accurate data ranging from what is happening in my factories and my distribution networks to [what is happening at] the customer point of sale. If we could connect all these dots seamlessly and in real time, we'd wring a lot of waste out of our industry. EDI (electronic data interchange) is a failed dream in my estimation. The Internet of Things holds hope.

Our take

Companies that aggressively make the pivot to buy globally and aggregate buying power can leverage lower-cost strategies. The key is using some mechanism like attribute-based forecasting, attach-rate planning, or postponement. The item-master and SKU-based logic used in most off-the-shelf software solutions is too restrictive and constraining. Carter's use of the dimension code and the rationalization of retailer platforms into a standard code allows the company to gain both economy of scale and flexibility to differentiate for the retail channel.

If you'd like to hear more about Carter's strategy and achievements, plan on attending Supply Chain Insights' Global Summit in Lake Oconee, Georgia, September 5-8, 2017. Peter is one of the three confirmed speakers. We will start accepting registrations in January and will release the full program in February. I hope to see you there!