Today's hypercompetitive business environment has contributed to a shift from the traditional organizational focus on a limited set of competitive priorities to a need to focus on a range of changes, uncertainties, and risks. As a consequence of the turbulent business environment, which causes disruptions along supply chains, organizations cannot rely on the traditional means and ways of managing their operations. This is evident in Ketchen and Hult's idea of "best value" supply chains. The key premise of this contemporary supply chain concept posits that traditional supply chains focus on limited outcome factors (that is, speed and cost), while the best value supply chain "excel[s] along an array of uniquely integrated priorities," such as cost, quality, speed, and flexibility.1 These supply chains are associated with the notion of supply chain agility—a key capability for organizations thriving in a turbulent and constantly changing business environment.2

Supply chain agility enables organizations to swiftly sense and respond to changes that are internal and external to their supply chains in reactive, proactive, and, ultimately, predictive manners by relying on their supply chain relationships in order to fulfill customer requirements.

One example of how supply chain agility is playing out in the real world is the production of Apple's iPhone and Boeing's 787 Dreamliner aircraft through manufacturing networks spanning several regions and even continents. While these manufacturing networks are not new, their dispersion and scale have significantly increased due to technological advancements and trade-policy liberalization.3 Over the past four decades, trade in manufacturing networks has grown at a much faster pace than total world manufacturing trade.4 For example, manufacturing networks account for almost half of Australia's manufacturing exports.5

![[Figure 1] Survey respondents' job titles](/media-library/20170622toward-supply-chain-agility-ex1.jpg?id=53611846)

![[Figure 2] Ranking of key factors associated with strategic agility across the supply chain](/media-library/20170622toward-supply-chain-agility-ex2.jpg?id=53611847)

[Figure 2] Ranking of key factors associated with strategic agility across the supply chainEnlarge this image

![[Figure 3] Ranking of key factors associated with operational agility across the supply chain](/media-library/20170622toward-supply-chain-agility-ex3.jpg?id=53611848)

[Figure 3] Ranking of key factors associated with operational agility across the supply chainEnlarge this image

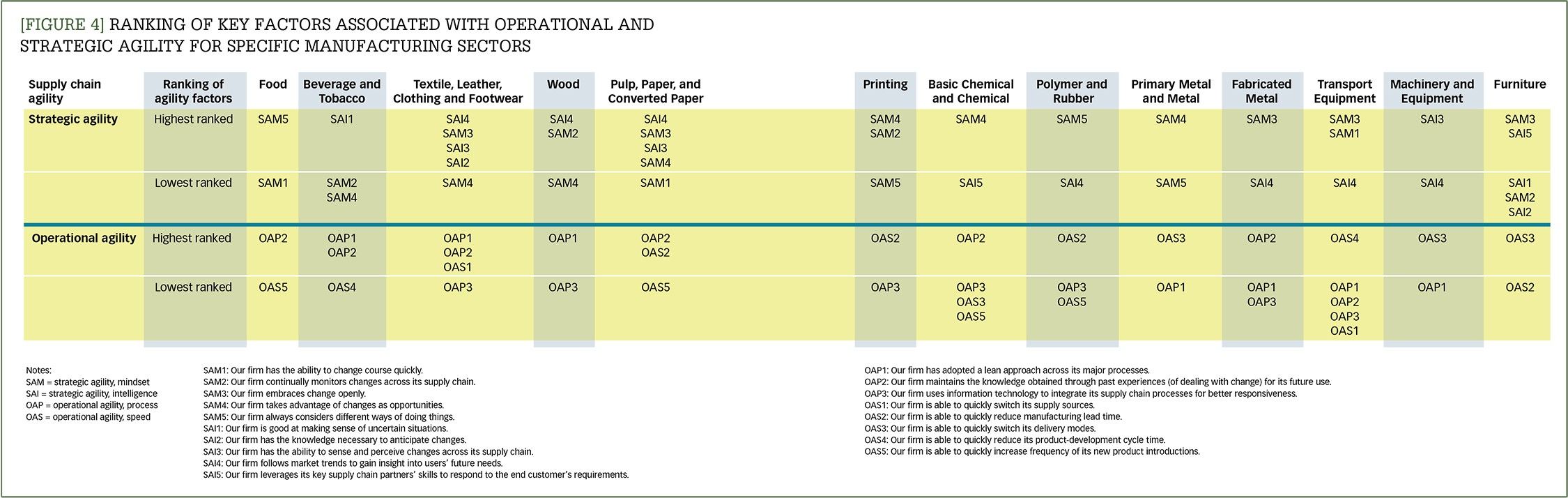

[Figure 4] Ranking of key factors associated with operational and strategic agility for specific manufacturing sectorsEnlarge this image

![[Figure 5] A framework for supply chain agility development](/media-library/20170622toward-supply-chain-agility-ex5.jpg?id=53611850)

Operating as an integrated network to process a block of production based on their geographical, labor, and knowledge resources and capabilities creates considerable cost benefits for the involved organizations, industries, and economies.6 Therefore, it is important that they proactively consider manufacturing networks as a platform for global integration, market and resource accession, and risk management, especially when the domestic market becomes less attractive or too costly to sustainably operate.

Agility is a significant lever and capability for organizations, industries, and economies to develop and maintain their competitiveness and ensure sustainable integration into manufacturing networks.7 This is largely due to the ability of agile systems (for example, supply chains) to proactively deal with uncertainties and disruptions through rapid adaptation and reconfiguration of their resources, structures, and relationships. For example, IBM showed the significance of agile capability when it managed to revive from its business-model struggles during the 1990s.8 In contrast, Kodak's decline proved the consequences of being sluggish in responding to paradigm shifts.9

Recognizing the importance and benefits of supply chain agility in the context of manufacturing networks, we have undertaken a study to assess the current state of agility across various Australian manufacturing sectors as well as to identify how these supply chains can enhance their agility and remain attractive to important players in the manufacturing networks. First, we provide key considerations for operations and supply chain managers regarding how to improve their supply chain agility when developing their organizational strategies. Second, we propose a road map that will guide managers in developing such strategies.

Supply chain agility in Australia's manufacturing sector

We collected data using a self-administered, paper-based survey questionnaire. All of the items in the questionnaire (except the demographic section) were continuous and measured using a five-point scale, with 1 = strongly disagree and 5 = strongly agree as its anchors. The contact details of a sample of 2,000 Australian manufacturing organizations were obtained to form the sample frame of this study. Two rounds of contact with the sample organizations were made: first, distribution of a pre-notification letter, and second, distribution of a survey package. Finally, a total of 190 responses were received and, after data screening and cleaning, a sample size of 185 (a response rate of approximately 10.5 percent) was used for the analysis.

Following the Australian and New Zealand Standard Industry Classification (ANZSIC) system, 13 subdivisions in the manufacturing division were used in order to identify the industry structure in the sample. The largest group of respondents represented the machinery and equipment subdivision (25.4 percent). Figure 1 outlines the respondents' job titles, highlighting that the majority are experienced, top-level executives/managers in their respective organizations.

We used descriptive statistics to draw the findings associated with the agility of Australian manufacturing supply chains. These findings are discussed from three perspectives: (1) general manufacturing, which communicates our general findings of the entire manufacturing sample; (2) specific manufacturing industries, which communicates our findings based on specific manufacturing industries; and (3) size of manufacturer, which communicates our findings based on the size of the manufacturing organizations. We have also discussed supply chain agility in terms of strategic agility and operational agility to make the findings even more accessible for operations managers. Strategic supply chain agility is focused on sensing and responding to long-term changes in proactive and predictive ways, whereas operational supply chain agility deals with short-term changes and an organization's capability to swiftly sense and respond to such changes in both reactive and proactive ways.

GENERAL MANUFACTURING

STRATEGIC AGILITY

The practitioners' responses to the questions related to the level of strategic agility across their supply

chains reveal that they are highly engaged in identifying and applying different methods for solving business problems.

This indicates that Australian manufacturers have a behavioral capacity to instigate a proactive response to uncertainties

at strategic levels when and where needed. Moreover, respondents consider that their organizations are actively taking advantage

of the opportunities that change presents and that they also have the required readiness to openly embrace these changes.

The results indicate the relative lower ranking of strategic agility factors that pertain to developing and maintaining mechanisms for better understanding changes across supply, product, and demand. In fact, the notion of following market trends to gain insight into users' future needs was the lowest-ranked item. Moreover, manufacturers' ability to sense and perceive changes across their supply chains, and their ability to leverage key supply chain partners' skills to respond to the end customers' requirements were ranked ninth and eighth, respectively. The relative lower ranking of the above-noted items implies the need for further work on strengthening the business intelligence capability of organizations within the Australian manufacturing sector (see Figure 2).

OPERATIONAL AGILITYWhen considering operational agility, Australian manufacturers rely on various processes focused on knowledge retention, lean operations, and information technology (IT) systems to enhance their supply chain agility. Our findings indicate that this process-driven approach dominates operational agility development where, for example, knowledge gained from past experiences dealing with change and the adoption of lean approaches are heavily practiced by organizations. This highlights an important area of attention for operations and supply chain managers concerning business process (re)engineering in light of knowledge management, lean thinking, and IT integration priorities as part of supply chain agility development. Conversely, the bottom two-ranked operational agility factors relate to the ability of the manufacturing organizations to reconfigure resources for new product development through increasing the frequency of new product introductions or reducing the product-development cycle time. This is a major area of concern, as it reveals the weakness of Australian manufacturers when it comes to operational agility and exercising the right speed of response to deal with changes such as customers' change of product/service preference or demand for shorter lead times (see Figure 3).

SPECIFIC MANUFACTURING INDUSTRIES

STRATEGIC AGILITY

When we broke down the results by industry, they showed that the furniture and the beverage

and tobacco industries have completely different dynamics in their strategic agility compared

to those for general manufacturing. More specifically, within the beverage and tobacco industry,

"making sense of uncertain situations" was ranked as the top strategic agile capability, followed by a

culture that "openly embraces change" across the supply chain. However, this industry does not sufficiently

monitor changes in the business environment, nor does it take advantage of changes as opportunities, as these

were the lowest-ranked factors. This implies that the beverage and tobacco industry, while cognizant of

internal and external changes across the supply chain, is not prepared to translate this cognizance into

focused actions in support of their strategic agility.

On the other hand, the situation within the furniture industry is different, with leveraging key supply chain partners' skills to respond to the end customer's requirements ranked first. This manifests the primacy of creating business intelligence as part of strategic agility via effective collaboration with partners to ensure the attainment of adaptable resources and skills. Furthermore, fabricated metal and machinery and equipment are the two other industries that have different top-ranked agility factors than those for general manufacturing. However, these industries follow the same pattern identified across general manufacturing in terms of the lower-ranked strategic agility factors. Overall, a comparison of descriptive statistics across specific manufacturing industries reveals that the transport equipment industry has the highest and the primary metal and metal industry has the lowest level of strategic agility in the Australian manufacturing sector.

OPERATIONAL AGILITY

The results show that the polymer and rubber, transport equipment, machinery and equipment, and furniture

industries have a different state of operational agility than does manufacturing as a whole. More specifically,

across these four industries, the ability to quickly switch delivery modes is ranked first (machinery and equipment, furniture) or second (polymer and rubber, transport equipment). Furthermore, respondents across these industries have consistently ranked factors that equate to speed of response higher than those related to systems and process for developing operational agility.

While respondents in the machinery and equipment industry perceived their ability to quickly increase the frequency of new product introductions to be high, respondents within the polymer and rubber industry ranked it as the lowest factor in their operational agility dimension. Further, in contrast to respondents in the polymer and rubber industry, who gave high marks to their ability to quickly reduce manufacturing lead times, furniture industry respondents viewed it as a challenging area across their operations. Other factors that are ranked low by the above-mentioned industries include adoption of a lean approach across major processes (transport equipment, machinery and equipment) and use of IT to integrate supply chain processes (polymer and rubber, transport equipment). Overall, a comparison of the descriptive statistics across specific manufacturing industries reveals that the textile, leather, clothing, and footwear industries have the highest level of operational agility, and the beverage and tobacco industry has the lowest level of operational agility in the Australian manufacturing sector (see Figure 4).

SIZE OF MANUFACTURER

STRATEGIC AGILITY

Analysis of responses from manufacturing organizations of various sizes demonstrates a clear

distinction between their high- and low-ranked factors associated with strategic agility.

This evidently indicates that organizational size does influence the ways through which

organizations strive to develop and maintain strategic agility across their supply chains.

In this regard, responses from small manufacturers tended to favor behaviors resulting from

a mindset that promotes embracing change and translating it into opportunities. Medium-sized

manufacturers ranked making sense of uncertainties and responding through quick changes of

course as their top strategic agility levers. Lastly, within the large companies, their

top-ranked factors reveal their focus on the sensing, perceiving, and monitoring of changes

across the supply chain.

With regard to the low-ranked factors, it can be seen that small Australian manufacturers have less ability to sense and perceive changes across their supply chains. This is followed by lack of attention to following market trends in order to improve their understanding of the customer's needs, which can be associated with their limited resources and project-based operation. Similarly, medium-sized companies show fewer tendencies to continually monitor changes across their supply chains. However, large manufacturers face issues with respect to finding different ways of solving business problems and making sense of uncertain situations, as indicated by their low ranking of these factors.

OPERATIONAL AGILITY

In contrast to the results obtained for strategic agility, small, medium, and large manufacturers

all ranked their operational agility factors in a similar way. Generally, all the manufacturers

perceived factors associated with systems and processes (such as knowledge retention, lean,

and IT) as their top-ranked and speed of response (across new product development) as their

lowest-ranked factors in relation to operational agility. This implies that regardless of

their size, and in line with what was discussed in the general manufacturing section, Australian

manufacturers tend to concentrate on knowledge management, lean principles, and IT capability

with relatively less resources spent on, for example, rapid new product introduction as part

of their operational agility practices.

So, how to develop a truly agile supply chain?

Building on the survey findings within the context of the Australian manufacturing sector, we

identified four key elements that constitute a road map toward development of supply chain

agility, which are represented graphically in Figure 5: (1) mindset, (2) intelligence, (3) process, and (4) speed. Mindset and intelligence contribute to the advancement of strategic agility, whereas process and speed are the cornerstones of operational agility. These elements can be process-based, relationship-based, or a combination of both, but what needs careful attention by operations and supply chain managers is that sole reliance on one or the other may not allow an organization and its supply chain to take full advantage of agile capability.

This is important, as global production sharing through manufacturing networks involves significant political, social, cultural, and institutional dynamics, requiring companies to have strong relational and behavioral competencies in order to swiftly sense and respond to market risks as part of their global integration efforts. Furthermore, for conglomerates and holding companies, it is important that industry-specific requirements and the scale of operations (in terms of size of the business) across the portfolio of businesses are considered in resource-allocation and investment decisions when developing strategic and operational agility. This will assist in targeted agility-development programs that can be aligned with the required level of strategic and/or operational agility for the business based on its supplier situations and customer requirements.

Let's take a brief look at each of these elements across strategic and operational agility.

STRATEGIC AGILITY

In the context of strategic agility, mindset refers to organizations' sensitivity

to change and their readiness to deal with and manage change. Thus, mindset entails the

awareness and identification of change, as well as the preparedness, openness/willingness,

forward-looking, and opportunity-seeking aspects of the agility concept.

It is important that operations and supply chain managers have a mindset that allows their organizations and supply chains to embrace and quickly respond to changes in today's turbulent business environment in order to seize opportunities and remain competitive. For example, when Apple launched its iPhone in June 2007, it immediately became a global sensation. Only a handful of organizations were prepared for the rapid adoption of smartphones and their increasing popularity. However, Samsung sensed the importance of this global trend and within three years developed and launched its first smartphone, the Galaxy S1, which became one of the top-selling smartphones in the world. Due to its quick rebound and agility-oriented mindset, Samsung became the world's leading smartphone manufacturer, with a one-third share of the global market.10

Intelligence refers to information processing power and the particular skills of organizations that can contribute to their ability to respond quickly. Intelligence highlights the thinking and understanding, know-how and experience, and diligence aspects of strategic agility. It is important that operations managers have analytical capabilities to develop advanced "sense making" skills, which are a significant contributor to attaining the necessary strategic agility. For example, when introducing a new mobile application, the banking company Barclays analyzed social media to quickly identify and respond to customer issues, which played a keyrole in the successful launch of its new application.11 Similarly, the online travel company Expedia analyzes about 80,000 social media comments each month to be able to respond to and learn from the negative customer feedback in order to improve its service. The Coca-Cola product VitaminWater involves more than two million Facebook in the development of a new flavor to ensure that its new products are more appealing to the consumers. 12

OPERATIONAL AGILITY

Process refers to the systems and processes that agile organizations implement across their

supply chains to respond to uncertainties and changes in their environment. Lean manufacturing,

inventory management, learning schemes (for example, the plan-do-check-act cycle), and planning

programs constitute the process dimensions of operational agility. One famous example of agile

processes is the Foxconn case in which Apple CEO Steve Jobs decided just before the launch of

the iPhone to switch the screen from plastic to glass when he found out that the plastic was

not durable and could be easily scratched. Foxconn's managers immediately reacted to Jobs'

decision by rousing 8,000 workers inside the dormitories. Each employee was given a biscuit

and a cup of tea, guided to a workstation, and within 30 minutes started a 12-hour shift

fitting glass screens into beveled frames. Within 96 hours, the plant was producing over

10,000 iPhones a day due to its superior lean manufacturing capabilities.13

Speed refers to the organization's quickness in responding to both expected and unexpected uncertainties and changes across the supply chain. The speed dimensions of operational agility include aspects such as swift partnership formation, manufacturing lead times, and product development. For example, the automobile industry's high costs of entry, economies of scale, and network challenges in regard to distribution, fueling, and service lead time make it difficult for new entrants to become successful. However, this was not the case for Tesla Motors, which overcame many barriers and successfully pioneered electric-powered cars. Tesla Motors reduced both its cost of entry and the learning curves through forming partnerships with Lotus for the chassis of its first car, the Tesla Roadster. By also leveraging Panasonic's capital to develop batteries, it was able to quickly bring products to market.14

Key considerations for managers

Agility is an important capability that organizations, industries, and economies should develop and

maintain to successfully integrate into global manufacturing and sustain their competitive advantage.

Based on findings from a large-scale survey from the Australian manufacturing sector, we provide key

considerations for operations and supply chain managers regarding how to improve their supply chain

agility from two interdependent dimensions: strategic perspective and operational perspective.

To improve their strategic agility, managers should focus on developing the right mindset for sensing changes and readiness to deal with and manage changes. Additionally, they have to develop their analytical capabilities to improve how they make sense of the business environment. As for achieving operational agility, managers should focus on developing their processes to accommodate changes and enhance the speed with which they respond to changes. Achieving supply chain agility should be developed across both strategic and operational agility dimensions to ensure that organizations, industries, and economies can respond to the challenges of operating within today's volatile global manufacturing networks.

Notes:

1. David J. Ketchen and G. Tomas M. Hult,

"Bridging organization theory and supply chain management:

The case of best value supply chains,"Journal of Operations Management 25, no. 2 (2007): 573-580.

2. Manisra Baramichai, Emory W. Zimmers Jr., and Charalambos A.

Marangos,

"Agile supply chain transformation matrix: An integrated tool for creating an agile enterprise,"Supply Chain Management:

An International Journal 12, no. 5 (2007): 334-348.

3. Shuhei Nishitateno,

"Global production sharing and the FDI-trade nexus: New evidence from the Japanese automobile industry,"Journal of the Japanese and International Economies 27 (2013): 64-80.

4. Robert C. Johnson and Guillermo Noguera,

"Accounting for intermediates: Production sharing and trade in value added,"Journal of International Economics 86, no. 2 (2012): 224-236.

5. Prema-chandra Athukorala and Tala Talgaswatta, "Global production sharing and Australian manufacturing" (Australian Government, Department of Industry, Innovation and Science, 2016).

6. Prema-chandra Athukorala and Nobuaki Yamashita, "Global production sharing and Sino-US trade relations,"China & World Economy 17, no. 3 (2009): 39-56.

7. David M. Gligor and Mary C. Holcomb, "Understanding the role of logistics capabilities in achieving supply chain agility: A systematic literature review,"Supply Chain Management: An International Journal

17, no. 4 (2012): 438-453.

8. Andrew D. White, Elizabeth M. Daniel, and Mohdzaher B. Mohdzain, "The role of emergent

information technologies and systems in enabling supply chain agility,"International Journal of Information Management 25, no. 5 (2005): 396-410.

9. Henry C. Lucas Jr. and Jie Mein Goh,

"Disruptive technology: How Kodak missed the digital photography revolution,"Journal of Strategic Information Systems 18, no. 1 (2009) 46-55.

10. Jaeyong Song, Kyungmook Lee, and Tarun Khanna, "Dynamic Capabilities at Samsung: Optimizing Internal Co-opetition," California Management Review 58, no. 4 (2016): 118-140.

11. Xin Li and Dan Roth,

"Learning question classifiers: The role of semantic information,"Natural Language Engineering 12, no. 3 (2006): 229-249; Deborah L. Roberts and Frank T. Piller, "Finding the Right Role for Social Media in Innovation,"MIT Sloan Management Review 57, no. 3 (2016): 41-47.

12. Jason Kincaid, "Facebook Just Got Its Own VitaminWater Flavor: 'Connect.' Seriously." (Techcrunch, January 7, 2010).

13. David Teece, Margaret Peteraf, and Sohvi Leih, "Dynamic Capabilities and Organizational Agility: Risk, Uncertainty, and Strategy in the Innovation Economy,"California Management Review 58, no. 4 (2016): 13-35.

14. Edward P. Stringham, Jennifer K. Miller, and J.R. Clark, "Overcoming Barriers to Entry in an Established Industry: Tesla Motors,"California Management Review 57, no. 4 (2015): 85-103.

{kind=link}