Concerned about rising transportation costs and longer lead times, nearly half of the supply chain professionals who took part in a new survey on procurement are considering sourcing materials and parts closer to home.

CSCMP's Supply Chain Quarterly conducted this exclusive survey earlier this year to find out if business and economic conditions were motivating companies to consider changes in their sourcing strategies. Practitioner members of the Council of Supply Chain Management Professionals were contacted via e-mail and invited to complete an online questionnaire about their current procurement strategies. Thirty-two CSCMP members provided useable responses to the questions.

For the most part, the survey respondents hailed from large corporations. A little more than one-third said their companies reported more than US $5 billion in revenues last year, and 31 percent of respondents said their companies typically spend more than US $1 billion annually on overseas procurement. The majority are U.S.- based, with 28 of the 32 survey takers naming the United States as their home country. However, the respondents came from a variety of market sectors, including 24 percent from retail, 21 percent from consumer packaged goods, and the remaining 55 percent scattered among a variety of industries, such as computers, chemicals, apparel, and automotive.

Perhaps not surprisingly, all of the respondents said they were obtaining product from China. After China, the most popular regions or countries for sourcing were Western Europe, Canada, Southeast Asia, Eastern Europe, and India (see Figure 1). Most respondents' companies appear to be limiting the number of countries they buy from: 41 percent were sourcing from six to 10 countries, and 37 percent acquired parts or material from fewer than five countries. Only 22 percent of respondents said that they sourced from more than 10 countries.

Cost seems to be the main factor influencing the respondents' initial sourcing decisions. Twothirds said they were prompted to seek offshore suppliers in order to obtain a lower delivered cost for materials or components. The second most frequently cited reason for offshoring was to obtain a lower purchase price. In general, most respondents are satisfied that their offshoring efforts are achieving those initial goals, rating them an "8" on a scale of 1 to 10.

And yet, the element of risk seems to weigh on the minds of those engaged in offshore procurement. Eighty-two percent of survey respondents said that risk issues like product-quality problems or geopolitical instability would lead them to seriously reconsider their current offshoring decisions.

Although offshoring requires a considerable long-term investment, those plans are not set in stone. The supply chain professionals who participated in our survey indicated that they re-evaluate their offshore sourcing decisions on a regular basis.

One of the most interesting findings was that, despite indicating that they are satisfied that offshoring has helped to achieve their cost objectives, 82 percent of respondents said they currently are reexamining the locations of their supply base. As stated earlier, almost half (46 percent) of survey takers said they are at least considering moving their sources of supply closer to their home country.

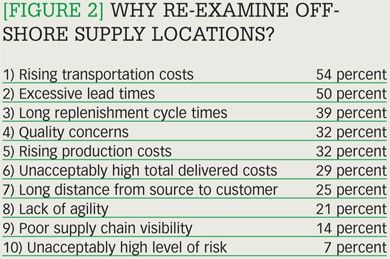

They're doing so for reasons of both time and money. Production costs may still be favorably low overseas, but the total cost picture is changing. The main culprit is transportation. Some 54 percent said that rising transportation costs were causing them to re-examine current sourcing locations. Meanwhile, the pressure to get new products to market more quickly is causing many to question their current sourcing network. Fifty percent of respondents cited excessive lead times and another 39 percent said long replenishment cycle times were among the most important reasons for rethinking their supply base (see Figure 2).

These factors will be playing key roles in the selection of new sourcing locations for materials, components, and finished goods. Fifty-six percent said that the number-one factor driving that decision would be lower total delivered cost. Another 21 percent said the primary driver would be faster replenishment.

"This survey highlights the true global and increasingly fluid nature of today's supply chains," says Dwight Klappich, a vice president with the analyst firm Gartner, who helped to develop the survey questionnaire. "The survey validates our research that finds that businesses are no longer wedded to specific sources for their goods and that risk and changing cost structures will force companies to continuously revisit their sourcing strategies."