Talk to enough retailers, wholesalers, and manufacturers, and they'll tell you that building up their omnichannel fulfillment networks is imperative for maintaining market share. But dig a little deeper, and you'll soon realize that omnichannel retailing is not a single bullseye target, but rather a diverse mosaic of operations that can include everything from shuttling inventory between brick-and-mortar storefronts to offering BOPIS, or "buy online, pick up in store," services.

Many practitioners have traditionally defined "omnichannel" as "distribution from anywhere," including the distributor's distribution center (DC), direct from the supplier, or shipped from a store or third-party logistics partner (3PL). But today, the term "omnichannel" seems to have almost as many definitions as the number of players in the marketplace.

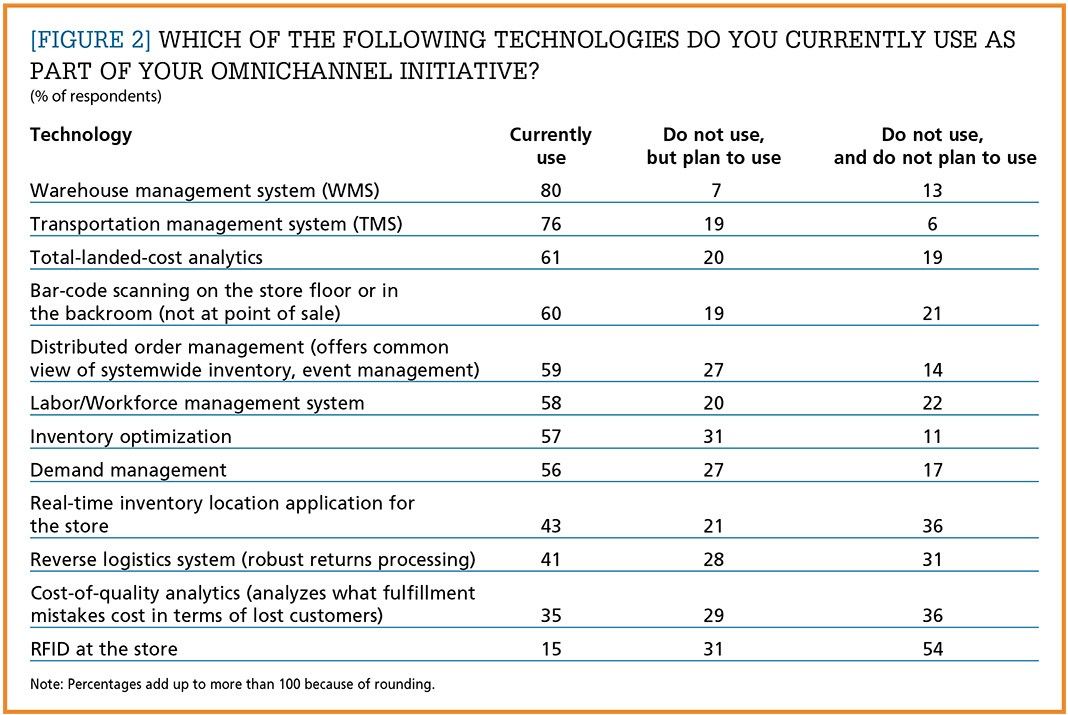

Which of the following technologies do you currently use as part of your omnichannel initiative?Enlarge this image

To learn more about the current state of omnichannel fulfillment practices, Supply Chain Quarterly's sister publication DC Velocity teamed up with ARC Advisory Group, a Dedham, Massachusetts-based management consulting firm, to conduct an industry survey. Respondents answered 32 questions about their approach to meeting current challenges in omnichannel commerce, with a focus on order fulfillment and, especially, the changing role of the retail store in helping companies deal with a surging tide of online orders. (For more information on the study, see the sidebar.)

Many different shades

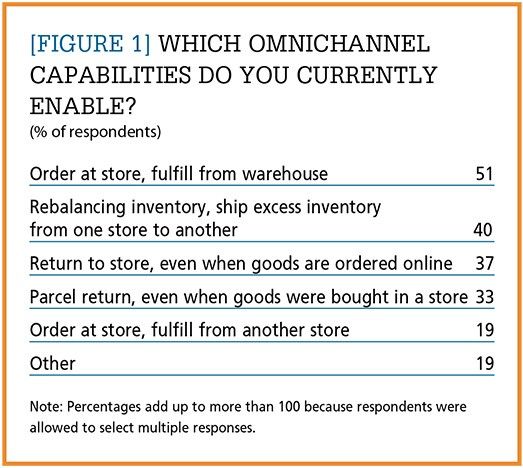

The survey revealed that retailers deploy a broad spectrum of cross-channel tactics to support sales in today's challenging omnichannel environment from "order at store, fulfill from a warehouse (or another store)" to "return to store, even when goods are ordered online." (See Figure 1 for the full rundown.) The survey also looked at what particular tools respondents rely on to get those jobs done. The data showed that the most common technologies or applications currently used by respondents as part of their omnichannel initiatives are warehouse management systems (80 percent), transportation management systems (76 percent), and total-landed-cost analytics (61 percent). (See Figure 2 for the complete list.)

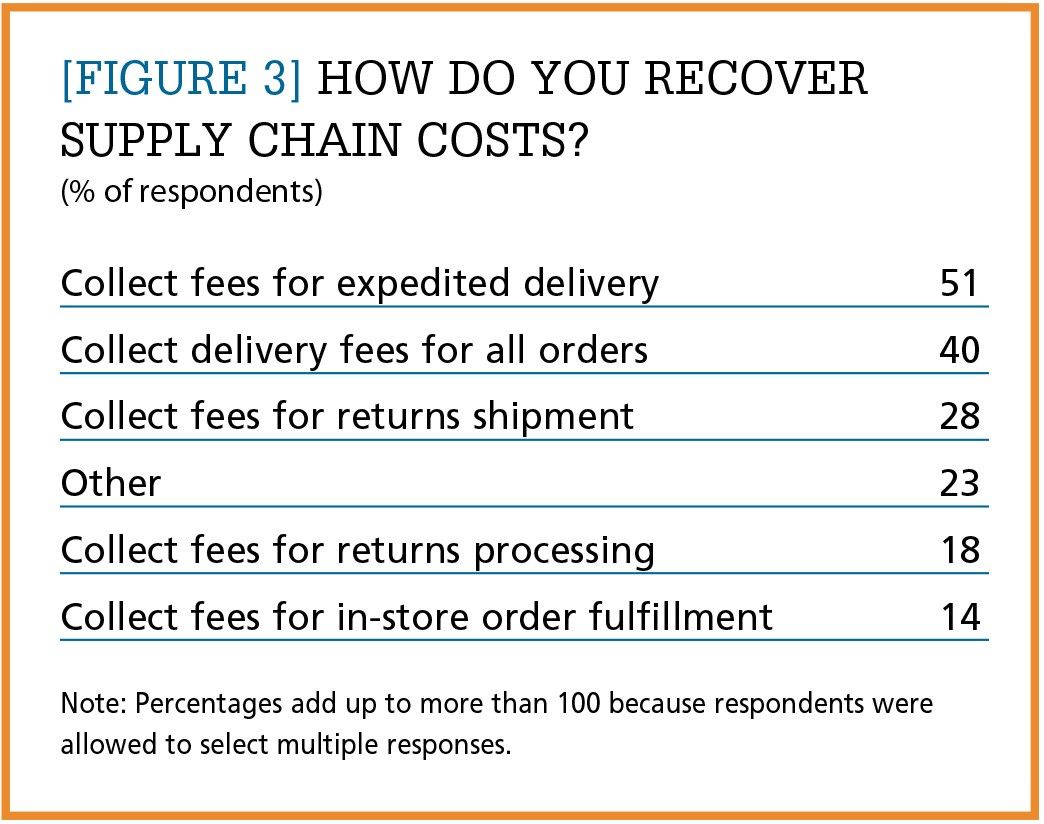

The respondents are also taking a variety of actions to recover the supply chain costs associated with fulfilling omnichannel orders. The numbers show that the most common approach is to collect fees for expedited delivery, cited by 51 percent of survey-takers. Next on the list was charging delivery fees for all orders (40 percent), followed by collecting fees for returns shipments (28 percent). (See Figure 3.)

Even with these efforts to recover costs, retailers' investments in their omnichannel capabilities (which include software, hardware, training, and shipping, among others) add up to serious money. So, what's motivating companies to continue adding tiles to the omnichannel mosaic? Respondents said the top four reasons they were participating in omnichannel commerce or intending to do so were: to increase sales (51 percent), to increase market share (50 percent), to improve customer loyalty (45 percent), and to increase margins (21 percent).

A growing role for stores

Over the past few years, there has been increasing attention paid to the practice of using store inventory to fulfill e-commerce orders. In response to this growing trend, this year's survey took a particularly close look at the role of the store in omnichannel fulfillment. While some major retailers, such as Walmart and Best Buy, are certainly using stores in this capacity, the survey found that the majority of e-commerce orders are still being filled from distribution centers. Sixty-eight percent of respondents said they were fulfilling at least some of their orders through a traditional DC that also handles e-commerce. Thirty-nine percent said items were shipped directly from the manufacturer or supplier, and 32 percent said they filled orders through a web-only DC. Only 26 percent of respondents said they were filling e-commerce from the store.

When were retailers choosing to use stores to fulfill e-commerce orders? The primary reason cited was inventory constraints or stockouts at the local DC (63 percent). That was followed by distance to the customer delivery location (53 percent) and resource constraints at the DC (13 percent).

"Survey respondents indicated that they frequently use stores for e-commerce picking, packing, and shipping when DCs are unable to meet overall order volumes," said ARC Senior Research Analyst Chris Cunnane, who oversaw the research and compiled the results. "In this case, when the DC is flooded with orders and will not be able to meet delivery timeframes, it will [hand off] the order to a local store to make sure the customer gets the order when they expect it."

To get a better sense of store-based fulfillment practices, the survey also asked respondents how they handled e-commerce orders filled through a store. The overwhelming majority (94 percent) said the stores both picked orders and shipped them to customers. Another 59 percent said their stores picked orders and held them for customer pickup, while 47 percent said orders were shipped from the DC to the store for customer pickup. (Survey-takers were allowed to select multiple responses to this question.)

"The most popular method for store fulfillment, as selected by 94 percent of respondents, is to pick orders in the store and ship them to the customer," Cunnane said. "Compared to last year's survey, when fewer than 70 percent of respondents identified pick and ship from the store, this is becoming a bigger part of store operations."

Turning retail stores into fulfillment operations will not be easy, however. Survey respondents identified three main capabilities that were crucial to a successful in-store fulfillment program. More than half (58 percent) of respondents said that they needed to  have visibility of inventory across all locations (58 percent), while 53 percent said the fulfillment process had to be easy for store staff to implement. Finally, 42 percent acknowledged that store associates would have to be trained in how to properly pick, pack, and ship orders.

"Training is a big part of ship-from-store, as the skills required for floor staff and warehouse staff are significantly different," Cunnane said. "Training store associates on how to properly pick, pack, and ship speeds up the process while helping to eliminate errors or damaged merchandise."

Given the need for additional investment in time and training, retailers appear to be somewhat selective about the stores they use for e-commerce fulfillment. Only 40 percent of respondents said they had enlisted all or almost all of their stores in the effort. From there, the numbers dropped off quickly. Twenty-seven percent indicated they handled e-commerce fulfillment at "a widespread selection" of stores, and another 27 percent at "a select subset" of stores. Thirteen percent said they used stores on a limited pilot basis, and 7 percent indicated that they didn't use stores for e-commerce fulfillment at all.

Brick and mortar is still king

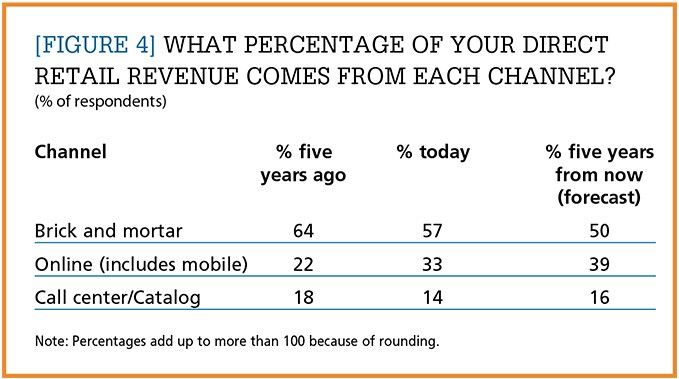

The e-commerce revolution is happening fast, and our survey showed that most retailers are investing large amounts of time, labor, and money to keep up. But every gold rush needs a reality check, so it's worth remembering that brick and mortar is still king. Asked what percentage of their direct retail revenue currently comes from each channel, respondents said 57 percent came from brick-and-mortar outlets, 33 percent from online (including mobile) sales, and 14 percent from call center/catalog sales.

Still, it's clear where the trend line is going. Just five years ago, brick and mortar generated a full 64 percent of sales, according to the survey respondents. Brick and mortar's share has slipped to 57 percent today, and respondents expect it to slide further—to 50 percent—in five years' time. By contrast, survey-takers see online's share, which stood at just 22 percent five years ago, rising to 39 percent by 2023. (See Figure 4.)

Work in progress

Taken together, the survey results indicate that omnichannel fulfillment is still in a state of flux. As retailers scramble to adjust to a shifting marketplace, they continue to fine-tune their networks, processes, and technologies. At the same time, they're adding tiles to the complex omnichannel fulfillment mosaic. To make it all work, they're relying more and more on a resource that was once just a bit player in the omnichannel game: the retail store.

Editor's note:Â A similar version of this article originally appeared in the November 2018 issue of DC Velocity magazine.