The global financial crisis triggered by the collapse of Lehman Brothers in September 2008 ushered in a new era of monetary policy making. Central banks across the globe—such as the U.S. Federal Reserve and the Bank of England—slashed interest rates and invented new ways to inject stimulus into their economies. Although the scars of the crisis are still evident, the global economy is far healthier now than it was ten years ago, thanks in large part to actions taken by central bankers. The recession would have been far worse without their aggressive and harmonized monetary response.

Now ten years removed from entering crisis management mode, policymakers must figure out if (and how) they wish to undo these extreme measures to mitigate some of their unwanted side effects. Doing this would have the benefit of preventing inflation, impeding financial bubbles from developing, and making it easier for central banks to soften the damage in future crises. The trade-off is that it makes it costlier to finance business investments and consumer purchases, which has a negative impact on economic growth and international trade.

Essentially, the question for policymakers boils down to whether they can remove stimulus without significantly reducing demand for goods and services. The answer to that question will vary greatly for different economies, given the uneven nature of their recoveries and an assortment of risks that must be taken into consideration. Nevertheless, those decisions will have a profound influence on global trade flows over the next few years. Aggressive removal of stimulus could ground trade to a halt, but maintaining low interest rates for too long could stir up even bigger problems down the road.

Fed makes the first move

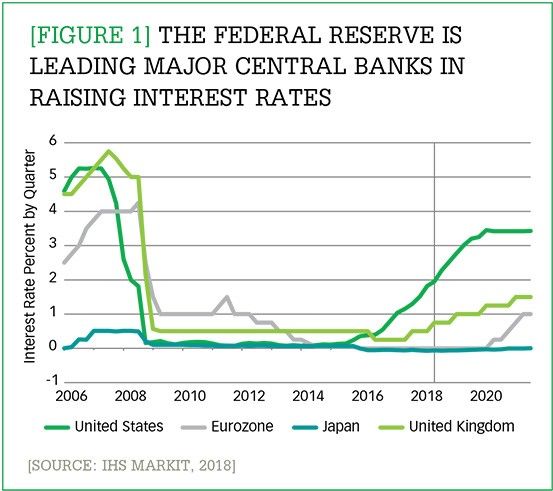

The U.S. recovery has outpaced those of other advanced economies, and so it is further along in its efforts to normalize monetary policy. From 2015 to 2017, the Federal Reserve (Fed) raised interest rates in irregular intervals and only by small amounts. However, in 2018 as U.S. economic growth accelerated, the Fed began raising interest rates more steadily and at more predictable intervals. (See Figure 1.) Heading into 2019, the Fed intends to raise interest rates further. Interest rates are now more than halfway back to what the Fed considers neutral—a rate which is neither restrictive nor accommodative of economic growth. The Fed has also backed off its commitment to keep rates low for an extended period and has begun winding down its balance sheet assets, selling off some of the assets and bonds that it bought in the recession. Both of these actions will contribute to tighter financial conditions.

What the Fed's path should be going forward is more difficult to handicap, given questions about how much further the economic expansion has room to run. The Trump administration's fiscal stimulus measures—tax cuts and additional government spending—are designed to have their peak impact on economic growth in 2018. By late next year, these measures will no longer be supporting growth, andthe U.S. economy will be more vulnerable to higher interest rates.

This may create a policy "fork in the road," at which point the Fed must decide whether to prioritize lengthening the expansion or fending off inflation. Inflation is currently relatively muted, but labor market tightness and tariff-induced price pressures should have a larger impact next year. On the other hand, the recent surge in financial volatility—a de-facto tightening of financial conditions—threatens to slow global growth (and therefore U.S. growth) on its own if it persists in 2019. This balancing act may create some policy uncertainty with spillover effects into the rest of the global economy.

Brexit uncertainty remains elevated

The Bank of England (BOE) followed the Fed's lead in the aftermath of the global recession by slashing interest rates, engaging in quantitative easing (or buying large amounts of government bonds and other financial assets to stimulate the economy), and introducing forward guidance (or communications about what their future monetary policy will be) to keep rates low for an extended period. In early 2016, it looked as if the BOE was poised to follow the Fed's lead on raising interest rates, but that prospect became increasingly uncertain after the 2016 referendum in which the United Kingdom voted to separate from the European Union (EU). The uncertainty caused by Brexit prompted the BOE to temporarily lower rates instead of increasing them. However, since late 2016, the U.K. economy has lowered its unemployment rate and managed enough growth to warrant slightly higher interest rates.

In recent months, however, the U.K. economy has taken a turn for the worse, and there remains a heightened amount of uncertainty about ongoing Brexit negotiations. The possibility that the U.K. and the EU might fail to strike a deal that would smooth the U.K.'s departure presents daunting downside risks. Firms would face new trade tariffs, potentially severe cross-border delays, and disrupted domestic supply chains, prompting the delay or cancellation of investment projects. In addition, the household economy would be hit via substantial losses in real income and wealth. This uncertainty creates a headache for the BOE, which cannot reasonably commit to raising interest rates until there is resolution regarding post-Brexit relations. As such, monetary policy will likely be on hold in the U.K. until the Brexit deadline in late March.

Baby steps for Europe and Japan

The European Central Bank (ECB) and the Bank of Japan (BOJ) took even more extreme measures to combat their sluggish economic recovery; they have been operating with negative short-term interest rates for several years (meaning that depositors must pay to keep their money in the bank). Now, each finds itself in a similar situation to the BOE—ready to begin removing accommodation but unable to do so with confidence, given the numerous economic and political risks.

Marking a significant step toward normalizing monetary policy, the ECB announced in June its intention to cease new asset purchases at the end of 2018. While the bank is likely to follow through with this commitment, there is a high degree of uncertainty as to when (or if) interest rates will rise. The bank has committed to keeping rates low until at least late 2019. Even then, the economy and risk profile would have to improve for policymakers to feel comfortable tightening monetary policy in a gradual manner. Economic expansion—which ECB chief Mario Draghi described one year ago as having "unabated growth momentum"—has lost steam recently, coinciding with rising tensions over the Italian budget standoff and deteriorating financial markets conditions, in addition to heightened uncertainty over a U.K. exit.

The ECB is in the unique situation of having to manage the outlooks of member countries with very different vulnerabilities. Germany's heavy reliance on exports, for example, makes it somewhat more exposed to shocks that erode global trade flows (such as protectionism), while a country like Italy is more susceptible to exchange rate swings and financial market gyrations due to its precarious budget situation. The types of threats that emerge over the next year will have varying impacts on euro countries, which makes it difficult to tease out a clear outlook for monetary policy by the ECB. The most likely scenario is one in which the ECB errs on the side of being cautious, opting to keep policy accommodative for longer given the numerous risks.

The BOJ is even further away from normalizing policy. The bank is expected to maintain yield-curve control for Japanese government bonds, which involves keeping its 10-year government bond yield at zero to raise the profitability of banks. It is also expected to keep its negative interest rate policy with aggressive monetary easing (or boosting of the supply of money) to achieve its 2-percent inflation target. However, modest inflationary expectations and delays in structural reforms will hinder the attainment of that target. It will be years until BOJ raises interest rates above zero, as the risks of slow economic growth are greater than the threat of inflation for Japan at the moment

China balancing stability and growth

China's economy has seen a similar slowdown in 2018 as it endures some growing pains during the transition toward a more service-based economy. The previously announced hike in tariff duties on US$200 billion in exports to the U.S. has been delayed for at least 90 days, a good sign that trade talks are becoming less hostile. Still, uncertainty about trade policy has led to dampened export orders for some Chinese goods. Additionally, tighter government financial supervision and regulation has slowed fixed investment, notably infrastructure and real estate investment. As growth slows, the government is shifting its policy balance toward growth support. In addition to fiscal measures taken by Beijing—including personal income tax cuts and export tax rebates on selected products—the People's Bank of China (PBOC) has chipped in by reducing banks' reserve requirement ratio. PBOC is likely to maintain a balanced or slightly accommodative stance in the near term so long as the yuan does not weaken significantly against other currencies. Although the tariff rate increase has been delayed, the risk of trade war escalation will be a key determinant in PBOC policy, and those developments are very much uncertain at this point.

Emerging markets fighting off currency depreciation

Rising interest rates in the United States have led to a much stronger U.S. dollar, which has put intense downward pressure on exchange rates for emerging-market currencies. Some of the emerging-market woes are also homemade, including poor governance, lack of structural reforms, increased political uncertainty, and a piling-up of debt, both in foreign and domestic currencies. These problems will get in the way of strong autonomous rebounds in emerging markets and developing countries (which account for about 40 percent of global gross domestic product). Emerging market central bankers will have a tough and unpredictable road ahead as they look to stem capital flowing out of their economies and currency depreciation, while also supporting growth.

Multiple forks in the road

The various challenges facing central bankers make for a highly uncertain policy landscape as the global economy enters the latter stages of expansion. Economic growth is due to slow, so policymakers must be careful not to remove accommodation too abruptly and cause a downturn. At the same time, there is good reason to believe there are benefits to be gained from returning to conventional monetary policies. Further muddying the path toward normalized policy is the elevated nature of global geopolitical risks that have developed recently. This raises the possibility that policy may unexpectedly deviate from its expected path, which could make for some disruptive financial market volatility over the next few years. This alone should not cause a big shock to the real economy, but it elevates the importance of policy choices that are made in response. As such, monetary policy will play a crucial role in determining the relative performance of global economies, and in turn, the manner in which the global supply chain adapts to shifts in demand.