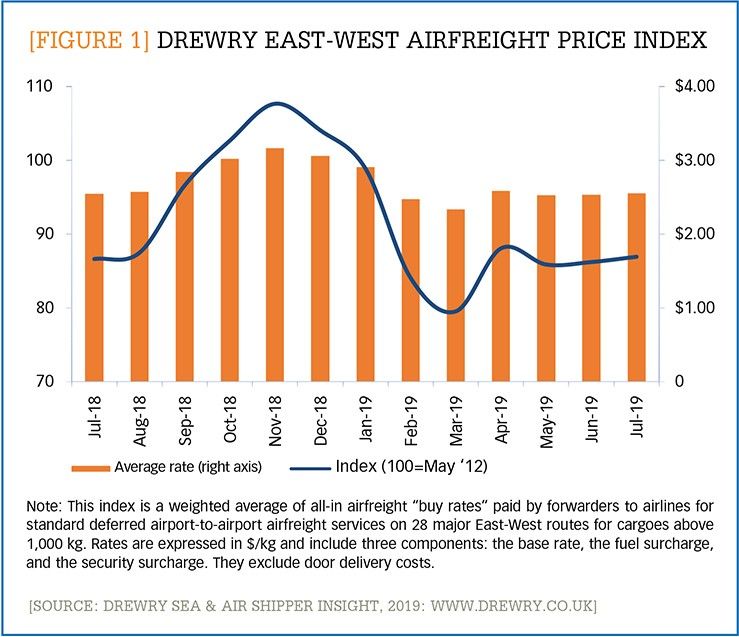

The looming threat of tariff increases caused the airfreight market to turn white-hot in 2018, as shippers pulled extra inventories forward in an attempt to beat the added costs. In response, rates jumped last year, with the Drewry East-West Air Freight Rate Index peaking at over $3.00/kilogramin November. (See Figure 1.)

But some level of stability on the trade front developed when the Trump administration cancelled the round of tariffs slated to take place in June (only to reimplement them, then postpone again in August), and airfreight markets cooled down considerably during the first half of the year. The industry saw both volumes and rates erode in key international markets. Since November 2018, rates have declined by over 15% and international volumes by 4%, according to the International Air Transport Association (IATA). This drop marks the first decline in seasonalized freight tonne kilometers (FTK) growth since 2015. Some carriers like Cathay Pacific have responded by managing capacity.1 But IATA has also reported that demand volumes have slowed faster than capacity has left the market.

Innovation heats up

While airfreight service providers were wrestling with a tough market, innovation was kept at bay in the industry. As a result, the development of digital air forwarding solutions has lagged relative to other modes of transportation. But in the past year, digital has taken center stage. In addition to digital offerings, other technological innovations, such as the possibilities of drone transport, are becoming more real, with cargo-focused drones being tested—and now contracted—for commercial cargo lift.

Startups in the digital forwarding space are graduating from beta status. For example, SkySpace Cargo announced late in 2018 that it had eclipsed 50,000 users of its booking platform. SkySpace and other companies like Cargo.One are focused on creating transparency in pricing and capacity for small- and medium-sized forwarders. This increased visibility enables smaller forwarders to compete more effectively with larger companies.

For shippers wanting to explore digital forwarding, companies like Freightos are creating solutions for both forwarders and shippers. Freightos' WebCargo Sky solution allows other forwarders to book directly with large airlines via a network of real-time APIs (application programming interfaces). The solution also allows shippers themselves to compare and book airfreight and ocean freight shipments with global forwarders and ocean carriers. Freightos has also created a hub of distribution centers that feeds directly into Amazon fulfillment centers, enabling smaller manufacturers to achieve levels of scale comparable to much larger shippers.

Cargo drones are also driving changes to the airfreight ecosystem. Drones are generally discussed as candidates for last-mile package delivery. Now, however, companies developing bulk cargo drones are at an advanced enough stage to enter into commercial contracts. Sabrewing Aircraft Co. signed a $40 million contract in Alaska to test cargo deliveries on an isolated island more than 700 miles from Anchorage.2 The deal includes 10 drones that have a capacity of between 800 and 4,400 pounds. Natilus, another startup, is planning to test comparable seaplane drones in 2020, with ambitions of bringing 130-ton freighter drones on line.3

The implications of cargo drones on the industry will be enormous. The cost of drones is significantly lower because the airframe is design tailored specifically to move cargo, not people. Additionally, the drone's slower airspeeds will also substantially reduce fuel consumption. Finally, the fact that drones do not require a crew will provide further cost savings. Ultimately, Natilus believes their large-scale drones will operate at half the cost of the current generation of air cargo planes while creating a new class of service that bridges the gap between existing air and ocean transit times.

While the familiar pattern of boom and bust for rates is playing out in the airfreight industry, shippers reliant on air freight for their networks can get ready for these game-changing technologies. Regular dialogue with digital forwarding providers to understand the maturity of their capabilities will enable shippers to identify when the time is right for partnerships and to unlock new capabilities like dynamic spot bids and other new abilities. And while it might be several years before shippers are booking space on drones, keeping an eye on providers and building relationships with innovators now will help both sides. Innovators will get critical support to test and build value propositions for their solutions whileshippers have an opportunity to shape the development solutions tailored to their unique needs.

Notes:

1. Damian Brett, "Cathay Pacific Cargo says flexibility is key in tough market," Air Cargo News (June 26, 2019), https://www.aircargonews.net/airlines/cathay-pacific-cargo-says-flexibility-is-key-in-tough-market/

2. Woodrow Bellamy III, "Sabrewing finds first customer for Cargo EVTOLs in Alaska," Aviation Today (March 21, 2019), https://www.aviationtoday.com/2019/03/21/sabrewing-finds-first-customer-cargo-evtols-alaska/

3. Randy Woods, "Drone-maker Natilus completes prototype taxi tests, releases images," Air Cargo World (May 31, 2018), https://aircargoworld.com/allposts/drone-maker-natilus-completes-prototype-taxi-tests-releases-images/