As transportation costs continue to rise, some analysts are saying that Mexico is once again becoming an attractive manufacturing location for serving customers in North America. Those taking another look at Mexico may be interested in the results of an annual survey of nearly 1,000 manufacturers by the Manufacturing Performance Institute and Industry Week magazine.

When it comes to supply chain integration, the survey found that Mexican plants are ahead of their counterparts in the United States and Canada. Some 28 percent of the Mexican plants canvassed said they had extensive integration with suppliers—compared to just 10 percent of U.S. plants and 8 percent of Canadian factories. In addition, 36 percent of Mexican plants reported that they were extensively integrated with their customers, compared to 14 percent of U.S. manufacturers and 16 percent of Canadian manufacturers. One factor accounting for this higher level of integration, according to the study, may be that Mexican plants are more likely to ship product to their own companies' facilities, whereas U.S. and Canadian plants are more likely to ship to other companies. The study did note that U.S. ownership or operation of the Mexican plants contributed in part to these close relationships, although integration was high even among plants with no U.S. affiliation.

Supplier and customer integration is not the only area where Mexican plants led U.S. and Canadian counterparts. Mexican plants also had the highest median inventory turns at 15, compared to 12 for Canadian plants and 8.8 for American manufacturers.

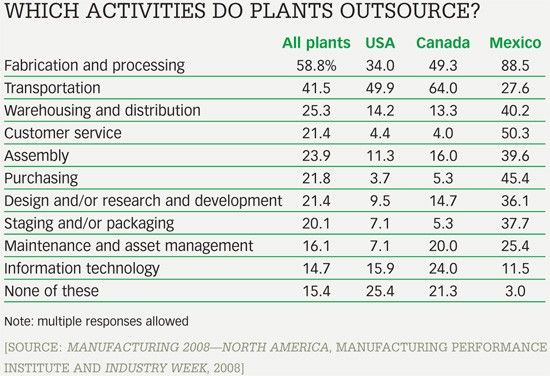

When it comes to operations, Mexican manufacturers outsource many more functions at a much higher rate than do U.S. and Canadian plants. For example, 88.5 percent of Mexican plants surveyed outsource fabrication and processing, compared to 34 percent for U.S. and 49.3 percent for Canadian factories. Some 40 percent of Mexican production facilities used third-party warehousing, compared to about 14 percent in the United States and a little over 13 percent in Canada. Perhaps the greatest difference was in the area of customer service, where 50.3 percent of Mexican plants used outsiders, compared to only 4.4 percent in the United States and 4 percent in Canada. The only functions that were not outsourced at a higher rate in Mexico than in the United States and Canada were transportation and information technology. (See "Which activities do plants outsource?" for details.)

One area in which Mexican manufacturing plants lagged behind their U.S. and Canadian competitors was in cost control. More than half (53 percent) of all respondents reported that manufacturing costs increased over the past year. Despite that hike, a fair number of U.S. plants—40 percent—said that they had managed to reduce their costs. Only 30 percent of Canadian plants and 25 percent of Mexican plants reported cost reductions.

[Source: Manufacturing 2008—North America, Manufacturing Performance Institute and Industry Week, 2008: www.mpi-group.net/thoughtleadership]