Although popular in Europe, short-sea shipping remains underutilized in North America despite its potential to offer cost-effective service with low greenhouse gas emissions. In the United States, short-sea shipping encompasses the domestic movement of goods along the coasts and through the St. Lawrence Seaway and the Great Lakes. Its use is limited, and it moves only a marginal amount of U.S. domestic goods. It may not be the mode of choice for shippers that require just-in-time delivery, but short-sea shipping can deliver goods in a timely, reliable manner and at a good price. It also offers a relatively cost-effective, safe, and low-emission alternative for transporting goods between coastal cities.

Short-sea shipping has the potential to play a greater role in two significant markets. First, it is suitable for transferring imports from large hub ports to smaller "spoke" locations, in what is known as the "feeder ship" market. Second, shortsea vessels can move goods between coastal U.S. cities, running parallel to major north-south highways and railways.

The main advantage of short-sea shipping is that it alleviates infrastructure congestion, particularly around major ports. When you consider that the volume of domestic shipments is expected to increase by 24 percent between 2007 and 2027 (from about 13.8 billion to 17.1 billion short tons) without a corresponding increase in infrastructure, it seems logical that short-sea shipping should gain a more prominent place in the U.S. transportation network. After all, one small vessel with a capacity of just 400 TEUs (20-foot equivalent units) eliminates 400 trucks from a highway. So, for example, using short-sea vessels to move incoming container traffic from the Port of Los Angeles/Long Beach to nearby feeder ports such as San Diego could help ease the notorious highway congestion in Southern California. It also could improve port throughput and decrease dwell time by reducing the number of containers waiting to be loaded onto chassis or railcars.

Even though short-sea shipping competes with north-south long-haul trucking, it can also create new opportunities for short-haul trucking companies. These motor carriers can form partnerships with shippers to deliver goods from secondary ports to end users. Short-sea shipping also may create a need for new warehousing and distribution opportunities at secondary ports.

Moreover, the mode provides an attractive alternative for shippers that want to reduce their carbon footprint and fuel costs. It allows for the consolidation of multiple truck shipments onto one vessel, many of which are now able to run on low-sulfur diesel fuel. While a truck can move one ton of freight 155 miles on one gallon of diesel, a typical barge or short-sea vessel can move one ton of cargo 576 miles using the same amount of fuel.

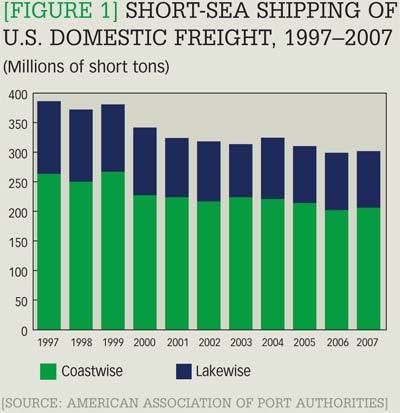

Despite all of these advantages, short-sea shipping, with its limited network, still holds a very small share of the domestic freight market. In 2007, just over 300 million short tons of domestic freight moved coastwise and lakewise, a decline of 21.9 percent from the 385 million short tons carried by barges and feeder vessels in 1997 (see Figure 1). These shipments, which include both domestic and import tonnage, accounted for about 2.2 percent of the total freight moved within the United States in 2007.

These numbers pale in comparison with the volume of short-sea shipping in the European Union (EU). More than 40 percent of the EU's freight moves along the coast and on inland waterways. The addition of inland waterway traffic to coastwise and lakewise shipments in the United States increases water transport's share of domestic tonnage to only about 6.7 percent in 2007.

Vessels on the Great Lakes have long carried bulk commodities, including iron ore, coal, and grain, for manufacturers, power plants, and end users in the U.S. Midwest and in Canada, but coastwise shipments have remained more limited. Nevertheless, more coastal initiatives have been emerging in recent years. Successful initiatives are adding value and flexibility to local supply chains and often complement rather than compete with railways and motor carriers. One example is the Port Inland Distribution Network (PIDN) of the Port of New York and New Jersey. In addition to the distribution of cargo from the port by rail and truck, barges move containers to the nearby ports of Bridgeport, Connecticut; Camden, New Jersey; Providence, Rhode Island; and Boston, Massachusetts, helping to reduce air pollution and alleviate congestion on the busy I-95 highway corridor that runs along the Northeastern coast of the United States.

Fortunately, short-sea shipping is beginning to attract a greater degree of federal support. The U.S. Maritime Administration is currently leading the Marine Highway Initiative (MHI), which conducts public outreach to advocate short-sea shipping's benefits to the public. It is working with other modes, private entities, and state and local governments to identify projects for expanding the short-sea shipping network. In addition to efforts by the St. Lawrence Seaway Development (U.S.) and Management (Canada) corporations, the U.S. Department of Transportation is collaborating with its Transport Canada counterpart to further encourage shipping on the Great Lakes. On January 22, 2009, the U.S. House of Representatives introduced the Short Sea Shipping Promotion Act of 2009, which would exempt certain cargoes from the harbor maintenance tax.

In short, federal, state, and port authorities are beginning to recognize that short-sea shipping provides an environmentally sustainable way to respond to continued growth in trade, consumption, and shipping. In addition, short-sea shipping does not require investment in extensive fixed infrastructure, aside from ports. Furthermore, an expanding short-sea industry could spur shipbuilding in the United States because of the Jones Act, which requires that the vessels participating in coastal trade be built, crewed, and operated domestically.

In the meantime, short-sea operators should actively court motor carriers and rail lines in order to form partnerships and offer greater flexibility to customers. Short-sea shipping companies must be able to offer a seamless transition of both containerized and bulk goods from ports to other modes of transportation. Motor carriers, in turn, can expand their area of coverage by offering flexible, "greener" options with a short-sea component. For their part, shippers should explore short-sea shipping options to see how this mode can fit into their supply chains. The savings in both cost and emissions may be well worth the consideration.

{kind=link}