The 2019 slowdown in U.S. freight markets affected volumes across modes of transport. The outlook for 2020 freight volumes is for weak growth in tonnage, driven by somewhat better conditions in manufacturing and agriculture as well as growth in import and export volumes.

The forecasted pace of modal growth depends on conditions specific to each mode as well as areas of continued competition between modes. Some of the key elements of the modal demand outlook are the strength of the freight-intensive portions of the economy, how businesses manage inventories and operations, government policies including trade policy, and the expectations of business and consumers. Our analysis of underlying 2020 macroeconomic and industry forecasts prepared by early February sees baseline freight volumes in 2020 growing weakly from the low 2019 base. Importantly, these forecasts were prepared before the 2020 impacts of the COVID-19 outbreak for the U.S. economy, global supply chains, and freight demand could be well-understood, so the downside risks to these forecasts are potentially significant in 2020.

The 2020 U.S. macroeconomic forecast has been revised up slightly, now with a projected 2.3% growth in gross domestic product (GDP). This suggests 2020 will be about flat with GDP growth in 2019, while remaining slower than the 2.9% pace of 2018. The 2020 GDP growth sees strengthening business investment, including additions to inventory, as well as a return to trade volume growth.

Last year's GDP growth depended more on government than business spending, and trade was a drag due to the fall in exports. There was also the strike against GM that hit auto industry shipments late last year.

This 2020 outlook is for growth that is slightly above-trend. Very low unemployment, higher workforce participation, constrained inflation, and improved productivity will all benefit the economy. Significantly for freight demand, the pace of 2020 import growth is forecasted to increase to 2.7% from the 1.3% increase seen in 2019. Perhaps more importantly, with the implementation of the United States-Mexico-Canada Agreement (USMCA) and the U.S.-China Phase I trade agreement tariff reductions, exports are forecasted to rebound from the 0.3% drop in 2019 to 1.6% growth in 2020.

In the first quarter of 2020, we will see a drag on GDP growth due to Boeing's shutdown of manufacturing for the 737 Max aircraft, the lag in trade response to the U.S.-China Phase 1 Trade Agreement, and the early Lunar New Year timing. Quarterly GDP growth will be higher in the second half of 2020, however. Year-over-year comparison of freight volumes will show an increase in tonnage volumes compared to 2019. In contrast 2019 did not compare well with the modal freight growth in 2018 that had been accelerated by advanced ordering and inventory building due to the changes in trade policies.

Not a rebound

The positive economic conditions driving 2020 freight demand are not a return to the pace of freight demand seen in 2018. IHS Markit's forecast of weak 0.7% growth in 2020 total freight tonnage will leave 2020 as another challenging year for carriers, including many companies still with excess capacity they are working down. This freight outlook is not for a rebound in underlying demand yet offers some hope to carriers that the trough in the cycle is past, and they can look for a better year than 2019.

For supply chain managers, this freight forecast outlook implies a potential return to transportation cost increases. However, the remaining excess capacity in the market will limit how much or how quickly those changes will affect them in 2020. For shippers, the pace of sales volume growth will remain moderate with a few exceptions such as for those export commodities seeing removal of retaliatory tariffs by foreign countries or even commitments from China to increase purchases.

However, there remain mostly downside risks to these baseline forecasts, including potential impacts from policy mistakes and/or sustained drops in business and consumer confidence, whether related to Covid-19 or other 2020 market disruptions.

Different modes, different pace

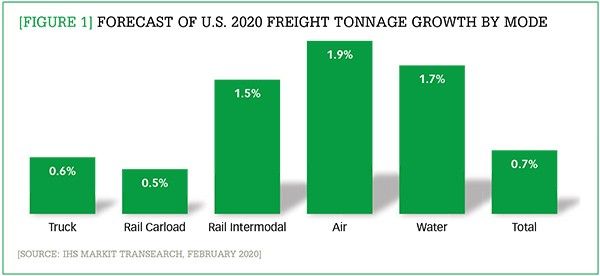

Not all modes of freight transport will see the same pace of 2020 growth; the IHS Markit Transearch 2020 tonnage forecast reveals significant differences by mode. While the overall freight tonnage forecast is 0.7% growth in the United States, air, water, and rail intermodal are all forecasted to see growth at more than twice this pace. These Transearch modal freight tonnage forecasts for 2020 are summarized in Figure 1.

In 2020, air cargo and waterborne tonnage are forecasted to increase by 1.9% and 1.7%, respectively, the fastest pace among freight modes. The air cargo and water modes will benefit from the 2020 recovery in international trade, with two-way growth anticipated in both import and export volumes. Air cargo will also benefit from expected growth in e-commerce shipping. IHS Markit forecasts rail intermodal tonnage to grow 1.5% in 2020. This increase will be driven by the growth in trade volumes, as well as less intense competition from trucking, due to the bankruptcies in the trucking industry and the industry's efforts to reduce excess capacity in 2019.

Trade volumes may be negatively impacted by delays in imports from China. Factories and inland transportation are expected to resume operations the second half of February, and trans-Pacific cargo flows will reach normal levels no earlier than early March.

The overall tonnage growth forecast is dominated by the huge importance of trucking (79% of total tons) and rail carload traffic (12% of total tons). With industrial production growing, albeit slowly in 2020, the more domestic-focused truck forecast is for growth of 0.6% while rail carload tonnage will see a 0.5% growth rate. This slow growth will be driven by manufacturing and agriculture moving up from the depths of 2019 production and shipments levels.