The COVID-19 pandemic is an example—albeit an extreme one—of the supply and demand shocks that can convulse supply chains today. There are many ways that supply chains can gird themselves against these shocks, but one that we believe merits much more attention is to develop a resilient sales and operations planning (S&OP) process.

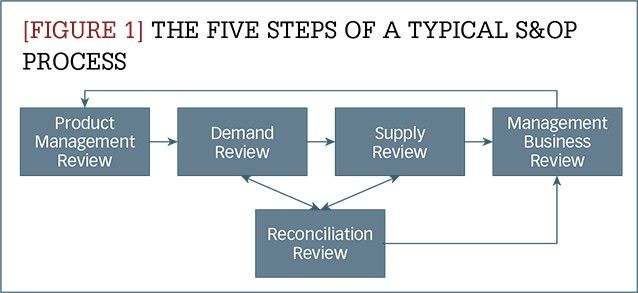

S&OP was developed over 20 years ago as a mechanism for synchronizing operations with changes in demand and supply. While S&OP processes vary between organizations, a consensus has formed that the S&OP process is comprised of the five steps outlined in Figure 1:

- Align the product portfolio with current strategy (product management review),

- Assess and shape demand (demand review),

- Assess and optimize supply (supply review),

- Reconcile gaps in supply/demand to form a rolling business plan (reconciliation review), and

- Present the plan and any unresolved issues to the leadership team (management business review) to ensure that it is aligned with current organizational objectives.

Enlarge this image

When these five steps are implemented, the process sometimes falls under the moniker of "integrated business planning" (IBP). But in our experience, most organizations continue to use the term "S&OP" rather than IBP when referring to the supply and demand balancing process even when implementing a five-step process.

An effective S&OP process has many benefits. When it culminates in a management business review, S&OP generates forward-looking operating plans that are aligned with organizational goals and objectives. The management business review works to create alignment among the sales, operations, marketing, and finance organizations. It typically reduces operational costs and working capital and has the potential for increasing sales through more efficient resource utilization. The process also ensures that stakeholders move from a static business plan to a rolling consensus-based business plan because the S&OP process is executed, most commonly, on a monthly cadence.

However, the typical S&OP process is not currently designed to cope effectively with the impacts of large-scale disruptions such as COVID-19. Its pursuit of alignment tends to focus on business-as-usual events, such as promotions or factory maintenance, while other processes, such as business continuity planning (BCP), concentrate on planning for unexpected events. Because the S&OP process, in general, does not incorporate the outputs from BCP processes and discards unforeseen events, it can work against an organization's efforts to achieve resilience.

Recent events—from the coronavirus's impact on the entire world economy to shortages of chicken at Popeyes and Kentucky Fried Chicken restaurants—suggest that organizations can pay a high price for deficits in resilience. Yet with some changes, the S&OP process could be a potent defense against the effects of extreme fluctuations in supply and demand. In order to extend S&OP's scope to cover supply chain resilience, it will need to integrate planning for unexpected events identified through other processes such as BCP. We call the enhanced S&OP process, "resilient S&OP."

To be sure, creating a resilient S&OP process will not be easy. It requires a comprehensive assessment of resilience, a challenge that is far from resolved in most organizations.

Strengths become weaknesses

A key characteristic of S&OP processes is that they bring visibility to operational functions within organizations, thereby exposing hidden buffers (be they excess inventory or capacity) that supposedly protect the enterprise against what is often viewed as departmental "bad behavior." Examples of such bad behavior include sales representatives inflating their forecasts to ensure adequate supply, or operations maintaining extra inventory to account for low forecast accuracy. When an organization implements S&OP, these hidden buffers become visible because each stage of the S&OP process seeks to remove unplanned slack and improve efficiency by causing inflated forecasts to shrink and inventory caches to disappear.

While such benefits are laudable, they do present a significant downside: The efficiency-building measures promoted by S&OP can produce business plans that can be quite rigid, making it hard for organizations to respond to unexpected disruptions. Consequently, when a resilience-based approach is not integrated into S&OP, the strengths that distinguish the process can become liabilities. Here are some examples of benefits that can become pitfalls.

Forecast-bias reduction. S&OP helps to reduce the forecast bias that creates systematic over- or underforecasting in organizations. When overforecasting diminishes, there is a one-time inventory reduction, as the buffers mentioned above are eliminated because there is no longer a need to support nonexistent demand. When systematic underforecasting is reduced, capacity buffers are eliminated because this obviates the need to maintain capacity to support unplanned demand. In general, these moves help to improve supply chain efficiency. However, the removal of buffers can also reduce the organization's resilience when it experiences an unforeseen disruption.

Forecast-based inventory balancing. S&OP also seeks to stop organizations from setting inventory levels based on speculation or conjecture. Before implementing S&OP, it is quite common for supply organizations to "build a little bit less" than sales' projections because commercial operations often overforecast to "make sure that we have enough product." This practice leads to inventory levels that are based on conjecture rather than joint agreement between the two groups. When S&OP is implemented, a large part of the initiative is getting commercial operations and supply to work together to build trust, align inventories and forecasts to "real market needs," and create joint agreements about proper inventory levels. As a result, most organizations do not include speculative supply and demand events in their primary S&OP forecast.

In most instances, organizations do keep upside and downside forecasts which are adjusted when deemed appropriate to account for planned promotions, shelf space increases/decreases, customer gains/acquisitions, and imminent weather events. In each case, however, these events are predictable and the decision to include them in the S&OP plan is a matter of timing.

The focus on expected rather than unexpected events significantly improves forecast accuracy and makes supply chain planning more efficient. However, this approach tends to produce thin inventory buffers, which also increases the organization's vulnerability to unplanned events. And of course, the process does not take into consideration unexpected events, the results of which we are all experiencing now with the unexpected COVID-19 pandemic demand and supply swings.

Efficiency-driven capacity allocation. Another benefit of S&OP is that it seeks to reduce unplanned production changes. It is well known that, in most instances, unplanned production changes (such as last-minute customer orders or material shortages because a supplier's plant is closed for maintenance) reduce an enterprise's efficiency. Companies that implement S&OP can maintain much more stable production runs because they have fewer unplanned schedule changes. While this stability is due in part to having more accurate forecasts, it is more substantially the result of having a disciplined supply and demand balancing process that aligns the entire organization. We have observed that companies running S&OP processes tend not to alter their production schedules unless all the stakeholders agree to the change.

However, when production periods are fully allocated based on productive effort, there is a potential to reduce flexibility, rendering the organization vulnerable to a lack of production capacity when faced with unexpected supply/demand shifts.

Practical remedies

As part of a study carried out at the Massachusetts Institute of Technology (MIT) Center for Transportation & Logistics (CTL), we have identified practices that organizations are adding into their S&OP processes to override the above pitfalls. Three simple enhancements, hereafter discussed, provide ways to explicitly add buffers or flexibility back into the system that can help organizations increase their supply chain resilience.

Predict the potential impact of unexpected events. While few stakeholders classify forecast bias as desirable, from a supply chain resilience perspective underforecasting is likely to have a larger impact on supply chain resilience than overforecasting. A sensitivity analysis could be presented during the S&OP process to show stakeholders the potential impact of unexpected demand surges or supply shortages. The analysis would show the percentage of the potential "upside demand" that can be covered by current supply. This analysis is based on the organization's current supply capabilities and the percentage of expected demand if "downside supply" conditions materialize. The analysis also shows how much forecasted demand can increase or supply can decrease before the organization faces significant customer service issues. Using this information, S&OP stakeholders can develop a proxy for the resilience of their supply chain and understand how much buffer they should have if the unexpected occurs. Once the implications are understood, the organization can assess the costs and benefits associated with proactively adding capabilities to increase supply chain resilience.

Develop scenario-based inventory plans. By taking uncertainty into account when quantifying supply and demand and when making inventory plans, S&OP stakeholders can understand the risks that are being taken and opportunities that may be missed when they commit to a given level of supply or demand. For example, when planning promotions, organizations often balance the cost of inventory write-offs against the potential for lost sales.

To increase supply chain resilience, organizations could expand the pool of potential upsides and downsides to include unexpected events. Discussing unexpected events or scenarios as part of the S&OP process will help stakeholders from different organizational functions align around responses to unexpected disruptions. There is evidence that discussing potential issues and responses can have benefits should the events come to pass.

When convened, S&OP participants can discuss supply, demand, capacity, and other risk exposures to form a consensus around the level of vulnerability that the organization is willing to accept and the level of resilience required to reduce that vulnerability. For example, it is possible to scan for events that are unpredictable in nature, such as hurricanes and snowstorms, ahead of the season for these weather-related disruptions. There is evidence that organizations that plan for such disruptions can serve customers more effectively than organizations that only respond when the prospect of a specific disruption makes the news. Discussing unexpected events on a regular basis can help support the development of credible supply and inventory scenarios that support a more resilient supply chain.

Develop scenario-based capacity allocation plans. Organizations can use the resilient S&OP process as a forum for gaining consensus on how much capacity to reserve for a product. By incorporating a focus on resilience into capacity-allocation decisions, S&OP stakeholders can leverage the way they utilize their capacity to gain additional flexibility.

For example, using a resilient S&OP approach, organizations may elect to produce low-volume seasonal products in the off season in order to reserve capacity in season to respond to demand and supply fluctuations. Because these are low-volume products, the added inventory will have a minor effect on working capital, while the reduced changeovers will free up significant capacity to respond to shifting demand during the selling season.

In the same way, organizations concerned about the effect of a major disruption may consider adding optional production capacity that can be called upon when base capacity is exceeded. In general, the cost of reserving capacity at an external facility is less than the cost of holding the capacity in your own facilities. If an organization controls a facility, it can be difficult and costly to keep a portion of the facility available to cover for adverse events. For example, agricultural chemical companies often reserve capacity at co-packing facilities to cover overflow orders, as it is more cost effective than having that same capacity largely unused within their own facilities.

Without applying a resilience lens to capacity allocation, it is likely that capacity will be deployed in the most efficient manner leading to high utilization. As suggested above, this decision could lead to making the supply chain vulnerable to business operation disruptions and prolonged periods of product shortages and/or increased cost.

At a crossroads

None of the practices listed above are entirely new, and many organizations have implemented them by tweaking the S&OP process when responding to adverse events. Yet, we believe our proposed method captures many of the better approaches to integrating critical planning processes as well as building resilience into the business operations. As the speed and intensity of disruptions continues to increase, organizations are faced with a choice: accept the weaknesses of an efficient but narrowly focused S&OP process or make the process resilient by collectively and thoughtfully designing the business to respond with resilience.

The former path rolls back the gains that have been made under the S&OP banner; the latter path will continue to enhance the gains made by S&OP, resulting in rolling business plans that are more balanced from a resilience and efficiency perspective.