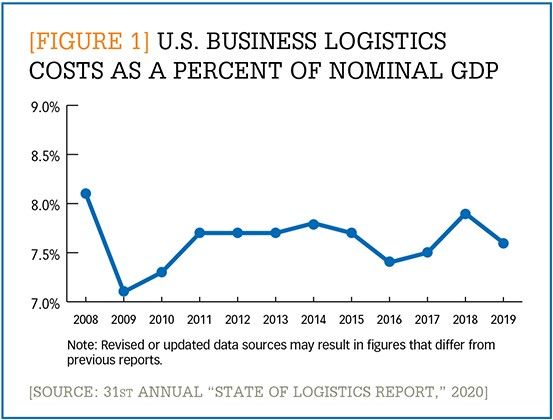

Just one year ago, in our annual “State of Logistics” special issue, we predicted that after navigating tight transportation capacity and soaring freight rates during 2018’s economic boom, shippers and carriers would spend 2019 trying to “bring back a sense of normalcy.” And things did seem to be headed in that direction. Total U.S. business logistics costs in 2019 grew by just 0.6%, a relief after the staggering 11.4% increase seen the previous year. Costs in 2019 represented 7.6% of the $21.43 trillion U.S. gross domestic product (GDP), down from 7.9% in 2018. (See Figure 1.)

Enlarge this image

But by early 2020, however, “normal” was out the window. The global COVID-19 pandemic has “decimated supply chains, scrambled logistics capabilities, and destroyed huge swaths of demand,” write the authors of “Resilience tested,” the Council of Supply Chain Management Professionals’ (CSCMP) “31st Annual State of Logistics Report.” Yet they were able to sound at least one positive note amid the crisis: The pandemic has made it obvious to all that logistics is essential to the economy and to the public good. The report also reinforces an important lesson: In times of disruption, supply chain resilience, flexibility, and agility will be fundamental to companies’ success, and even to their survival.

Written for CSCMP by the consulting firm Kearney and presented by Penske Logistics, the “State of Logistics Report” provides an overview of U.S. business logistics costs for the past year. It also includes a review of macroeconomic factors affecting logistics costs, analysis of each major logistics sector, historical data, and a look at trends that will shape logistics activities in the future. This year, each sector is also considered in the context of the pandemic, with recommendations for shippers and service providers on how to mitigate its impact.

Transportation costs: Up and down

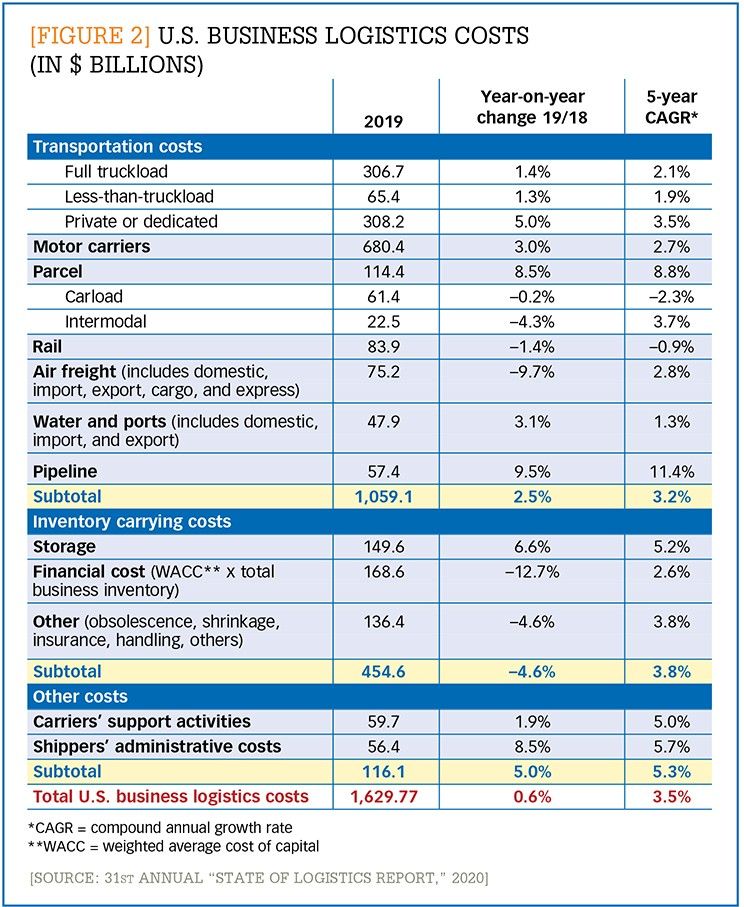

For three decades, the core of the annual report has been its analysis of the previous year’s business logistics costs, which are broken down into three main categories: transportation costs, inventory carrying costs, and “other” (support and administrative) costs. The grand total for 2019 was $1.63 trillion, with the lion’s share—$1.06 trillion—attributed to transportation. (See Figure 2.)

Enlarge this image

Overall, transportation costs grew 2.5%, a sharp drop from the 9.2% increase seen in 2018. Costs rose for trucking, parcel, and water but fell for air and rail. The following is an overview of last year’s important developments in each segment.

Motor carriers. Overall motor freight costs reached $680 billion in 2019. Expenditures on full truckload (FTL) hit $307 billion, a year-on-year increase of 1.4%—a far cry from last year’s 7.6% jump. Similarly, less-than-truckload (LTL) costs, at $65 billion, were up 1.3%, a respite from 2018’s 8.3% increase. Costs for private fleets and dedicated contract carriage rose by 5%, to $308 billion, as shippers sought to insulate themselves from the capacity problems and high prices of the previous year. On the spot market, average dry van rates tumbled 22%, largely due to the overcapacity that resulted when carriers’ record investments in new trucks collided with declining cargo volumes. The result was a market where shippers “regained buying power, negotiated lower rates, and secured capacity” and carriers had to worry about profitability, the report said. In the first half of 2019 alone, more than 600 truckers went out of business, citing declining demand, falling rates, and higher insurance and labor costs. The second half was even worse as shipment volumes continued to plummet.

Parcel. The U.S. parcel segment grew by 8.5% percent to $114 billion. The parcel sector’s fate rises and falls on e-commerce sales, which grew nearly 15% in 2019. Increased competition and consumers’ rising expectations pushed carriers and shippers to improve last-mile service while reducing their per-package costs. Both FedEx and UPS, for example, began year-round seven-days-a-week delivery. Many shippers began offering a wider range of delivery speeds (such as same-day, time-definite, and two-hour) and alternative delivery options (nights and weekends, lockers, and pick up in store). Last year saw, for instance, both UPS and Amazon partnering with retail chains to begin offering the option of “buy online, pick up in store.”

Rail. The Class 1 railroads saw weaker demand in 2019, and revenues declined by 1.4%, due in part to an industrial recession and reduced demand for coal. Even intermodal volumes, a reliable source of growth—albeit one that is less profitable than carload—declined as lower truckload rates led shippers to shift some intermodal volumes to motor carriers. Nevertheless, the four largest U.S. railroads (BNSF, Union Pacific, Norfolk Southern, and CSX) were able to improve their operating ratios and operating incomes in 2019 through network optimization and productivity improvements.

Water and ports. Overall costs in this segment, which includes container shipping, coastal shipping, and inland waterway barge traffic, grew by 3.1% in 2019, despite declining volumes. On the container side, importers trying to beat the Trump Administration’s January 1, 2019, imposition of new tariffs on Chinese goods caused a surge in inbound shipments in late 2018; the resulting stockpile depressed demand early in 2019, and inbound volumes for the year fell 0.6%, with the biggest declines at West Coast ports. Still, trans-Pacific contract rates from May 2019–April 2020 were 15% to 20% higher than in the previous contract period. That didn’t help container carriers much, as weak volumes “wiped out most of carriers’ 2018 gains,” the report said.

Air freight. Air cargo volumes dropped 9.7% in 2019—the worst showing since the 2009 financial crisis, according to the report. The drop was due to several factors: a slowdown in industrial shipments, especially in the automotive industry; the trade conflict with China; and U.S. tariffs on European aircraft and agricultural products. Cargo tonne-kilometers (CTK) declined by 3.3% over 2018, while capacity increased by 2.1%. It came as no surprise, then, that the East-West average air freight rates, including surcharges, paid by forwarders fell 6% in 2019. Growth in e-commerce and shipments of health care products were among the few bright spots.

Inventory, other costs a mixed bag

Inventory carrying costs, which comprise storage, financial, and “other” costs, tallied $455 billion, a drop of 4.6% over 2018’s total. That was primarily due to a 12.7% year-on-year reduction in financial costs (weighted average cost of capital x total business inventory) and a 4.6% decline in the remaining costs, which include obsolescence, shrinkage, insurance, and handling.

The big story, though, was in storage costs, which grew by 6.6%, to $150 billion. Throughout 2019, warehouse and distribution center rents continued to rise, to an average $6.51 per square foot, while vacancy rates remained at historic lows of 4.8%. Demand, especially for smaller, urban warehouses for e-commerce fulfillment, was strong in the second half of the year, and the 300 million square feet of new supply built in 2019, including a record 100 million square feet in the fourth quarter alone, was quickly leased.

The third major segment of U.S. business logistics costs, “other costs,” encompasses carriers’ support activities and shippers’ administrative costs. The former, which includes freight forwarding and third-party logistics (excluding purchased transportation costs), packing and crating, port services, and similar activities, rose 1.9% over 2018. The latter, which includes shippers’ wages, benefits, and information technology costs, jumped a hefty 8.5%. The report’s authors note that both 3PLs and international freight forwarders contended with declining freight volumes, rising storage and labor costs, a trade conflict with China, and protests in Hong Kong during 2019. While asset-light 3PLs saw declining profits, asset-heavy 3PLs improved profitability by better managing their assets. Some of the biggest freight forwarders were able to grow revenues and profits in 2019, thanks to good capacity management, lower fuel prices, and inventory buildups, as well as a strengthened presence in emerging manufacturing regions like Southeast Asia.

Preparing for an uncertain future

As in past years, the “State of Logistics Report” includes analysis of important trends or developments the authors believe will have an indelible impact on logistics costs in the future. This year’s focus is on technology, including artificial intelligence, machine learning, augmented and virtual reality, blockchain, robotics, renewable energy, the Internet of Things (IoT), and the 5G wireless communication standard. The authors pay special attention to 5G, which they say will have a “profound” impact on logistics by improving the data transfer speed, capacity, latency, and reliability of autonomous communication among devices, vehicles, and infrastructure. This, in turn, will accelerate the rate of automation in logistics operations, reducing costs and increasing visibility across the supply chain.

In an important departure from previous editions, this year’s “State of Logistics Report” devotes as much attention to the present as it does to the past. Overshadowing every page is the global COVID-19 pandemic. The report considers the current impact of the pandemic on each logistics sector, forecasts the possible near- and long-term consequences, and offers recommendations geared toward each industry segment for navigating virus-related disruptions and mitigating their impact. The following are just a few highlights:

- Motor carriers: The recession brought on by COVID-19 will cripple or force out carriers that were already on shaky financial ground in 2019. Shippers should enhance their supply chain resiliency, be a supportive partner to their carriers, and prepare for another capacity crunch. Carriers, for their part, should focus on improving asset utilization, use technology to cut costs, and diversify their revenue sources.

- Parcel: Homebound consumers spurred rapid growth in e-commerce, straining carriers’ networks and pushing up costs while providing greater scale and route density. Shippers can mitigate rising costs by matching their service levels to customers’ actual needs. Carriers may benefit from investing in a mix of delivery options and cementing relationships with large shippers.

- Rail: Year-on-year traffic dropped by 25% in the first half of 2020, leading carriers to take locomotives out of service, furlough employees, and restructure services and schedules. Shippers can continue to press carriers on speed, reliability, and visibility, while carriers could make additional productivity gains and more use of technology.

- Ocean: Inbound container volumes dropped sharply in Q1 of 2020; carriers cancelled many sailings, causing ship and container imbalances, higher spot prices, and port congestion. While the situation has eased somewhat, bargain-hunting shippers should assess carriers’ financial stability and avoid contributing to consolidation and bankruptcies. Carriers, already shaky before COVID-19 hit, need to finalize contract negotiations with sustainable rates.

- Air: With nearly half of air cargo carried on passenger planes and 90% of passenger flights cancelled in March and April, capacity suddenly shrank and spot rates shot up. Shippers should expect continued service reductions; while all-cargo services are an option, they are hard-pressed to meet demand that normally moves as belly freight. Carriers can handle demand uncertainty by being able to quickly flex capacity and manage variable costs.

- Warehousing: Pandemic-related e-commerce is causing surging demand for warehouse space, especially for grocery and temperature-controlled products, and new facilities are being quickly snapped up. Shippers that plan to increase safety stock and position more inventory closer to online customers must consider how that will impact their space needs. Warehouse operators will face higher costs and more labor shortages, suggesting that the pandemic will lead them to adopt more automation.

The U.S. economy has yet to see the full impact of COVID-19. The pandemic will strongly influence logistics capacity, geopolitical forces, and regulations for some time, the authors of this year’s “State of Logistics Report” predict. To what degree and for how long will depend on the severity and longevity not only of the coronavirus outbreak but also of any resulting recession. Regardless of how it all plays out, shippers, carriers, and 3PLs alike will need all the flexibility, resilience, and creative problem solving they can muster as they navigate the chaos of simultaneous plummeting demand in some sectors and exploding demand in others.