If you had to pick only one word to describe the airfreight industry in 2020, “fragile” would be a good choice.

Air freight’s interdependency on passenger flights to move freight means that it has faced opposing demand shocks this year. Passenger demand plummeted as nations closed their borders and airlines grounded hundreds of aircraft. At the same time, demand for time-critical personal protective equipment (PPE) for first responders surged.

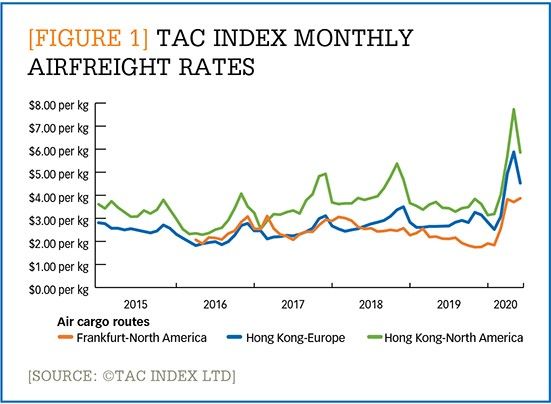

Overall demand for air cargo declined by 20% in June, but capacity dropped by 34%.1 The result was drastic price increases for cargos that absolutely had to move, such as medical supplies to combat the pandemic. The monthly TAC Airfreight Rate Index (Figure 1) reported a 45% increase in May over the previous 5-year high, which occurred prior to 2019 tariff implementations. Anecdotally, a few of my clients reported rates in excess of $10/kg on individual shipments from China to the United States. I’d be surprised if this weren’t reflective of a broader trend.

Enlarge this image

Full speed ahead

The COVID-19 turmoil has also served to accelerate a number of trends that were already developing in the airline industry, such as the retirement of older aircraft—especially in the wide-body space, including the 767, 747, and A380. It’s doubtful that many of these planes will see service as cargo freighters. There are no conversion kits left for the 747, and the A380 are likely too expensive to be deployed profitably. However, retired 767s are seeing new life in DHL’s fleet; the company ordered three more passenger-to-freighter conversions in June.

Replacing these aircraft are more modern widebodies, like the 787 and A350 XWB. While the order book remains several years deep, airlines have cancelled over 800 orders for 2020 through June, or roughly 15% of Boeing’s total logbook. Almost 90% of the aircraft deliveries this year, however, have been widebody models. Depending on the configuration, the passenger and cargo capacities of the new planes are similar to the aircraft they are replacing. The impact on capacity in the market, however, will depend on the level of acceleration of retirements relative to new deliveries.

Meanwhile the pandemic disruption has impacted key airfreight routes throughout the globe. Shippers have reported circuitous routing for their shipments through new gateways. This has introduced longer transit times, both due to longer routes themselves and due to delays related to clearance of cargo passing through new customs jurisdictions. The shutdown of passenger flights has temporarily made Anchorage, Alaska, the world’s busiest cargo airport, rising from sixth to first place on the Air Cargo News’ “Top 20 Cargo Airports” list.

Another change worth noting is a general awakening to the value of resiliency in the design of a global supply chain. This will impact the use of air freight in several ways in the near term. First, the strategic importance of air freight as a safety valve has been proven during the first half of 2020. Few shippers with a global footprint will risk going without a robust air contingency capability in place. Second, Kearney’s 2020 U.S. Reshoring Index report, “Trade War Spurs Sharp Reversal in 2019 Reshoring Index, Foreshadowing COVID-19 Test of Supply Chain Resilience,” found a renewed focus on reshoring away from China to other low-cost countries (LCC), principally Vietnam. Because Vietnam has much slower ocean transit times than China (Maersk publishes a 22-day transit time to Los Angeles, California, versus 11-day service from Shanghai), the air option will be increasingly important contingency for Vietnam-manufactured goods.2

One trend that remains on pace is the adoption of digital freight platforms for bookings. After a short blip down during the peak of COVID-19 airfreight demand, Freightos’ Webcargo marketplace saw e-booking orders grow by over 700% in June 2020 with up to 15% of global airfreight capacity available on digital marketplaces.3 The principal features that made e-booking attractive before COVID-19, namely the convenience and transparency into rate and capacity, have even stronger appeal in a constrained market. Similar to other types of e-commerce platforms, digital airfreight marketplaces have reached a level of adoption in 2020 that was not expected to be achieved until years from now.

Volatility ahead

Given all the change and disruption happening in the industry, the big question on shippers’ minds is when we will get back to some semblance of normalcy. Many shippers have postponed airfreight negotiations with their forwarders, and many of our clients are asking us when they should follow through with their annual air tenders.

The short answer is we’re unlikely to see stabilization through the end of the year. COVID-19 continues to spread across much of the U.S., and many Americans will be reluctant to fly anytime soon. Both of these issues will factor into passenger demand and the reintroduction of widebody belly space into the market. The International Air Transport Association’s (IATA’s) own forecast is that passenger volumes will not return to 2019 levels until 2024.

If that’s the case, then we can expect quite a bit more volatility ahead. Shippers—recognizing the need for air freight as an expensive (but necessary) lever to enhance the resiliency of their global network—will need to be nimble to deploy it at a reasonable cost. However, the adoption of tools like digital marketplaces can provide more transparency to enable better decision making. Even the largest users of air freight are facing the same issues, so those shippers that make the best of the current situation will be those leveraging all the tools available.

Notes:

1.1. Air Cargo Market Analysis,” IATA (June 2020): https://www.iata.org/en/iata-repository/publications/economic-reports/air-freight-monthly-analysis-june-202022

2. To obtain this data, Maersk’s scheduling tool was accessed on July 31, 2020 (www.maersk.com).

3. Damian Brett, “Digital air cargo bookings continue to grow despite COVID-19 outbreak,” Air Cargo News (July 20, 2020): https://www.aircargonews.net/airlines/digital-air-cargo-bookings-continue-to-grow-despite-covid-19-outbreak