The past five years in ocean container shipping have been interesting times for carriers and shippers alike. Large bankruptcies, driven by inflation-adjusted lows in market rates in 2016, were followed by the expansion of the Panama Canal and a rebalancing of trade flow among the West Coast and East Coast ports. Trade wars took shape soon after resulting in capacity crunches that pushed higher rates and better carrier profitability. Earlier this year, the International Maritime Organization’s (IMO) 2020 regulations to reduce sulfur oxide emissions was at the top of mind in the industry as new fuel standards were adopted.

It was against this backdrop that COVID-19 unexpectedly wreaked havoc on a global scale. Initial concerns were limited to manufacturing capacity in Asia and the potential impact on port and vessel operations. Epidemiologists suggested limited impact on ocean shipping, as the relatively long transit times of the mode limited the possibility of infection due to imported products. What wasn’t anticipated at that time was the massive health and economic impact COVID-19 would have as it spread to Europe and North America.

The net impact on ocean shipping has been a rapid decline in volumes. The Port of Los Angeles reported year-on-year total container reductions of almost 30% in May 2020, while on the East Coast, the Port of Savannah saw declines of almost 10%.

The power of discipline

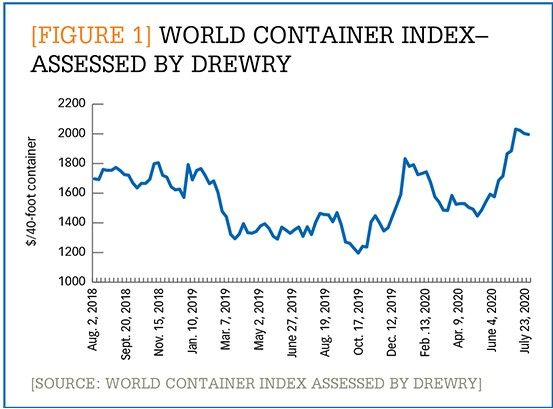

The historical response to similar reductions in demand has been a crash in pricing. But, as of the beginning of July, rates have maintained multi-year highs. (See Figure 1, which shows the World Container Index for the past two years.) The reason for that reversal has been new discipline on the part of carriers.

Enlarge this image

When an industry has high fixed costs, like ocean shipping does, there is significant pressure to chase market share. In the past, carriers have focused on filling ships, as the operating cost of adding an incremental container is quite low—in some cases below $100 per container. Carriers have long understood the relationship between supply and demand and have instituted policies like slow steaming that reduced fuel consumption and artificially absorbed capacity (it takes more vessels to operate a slower, but still weekly, service).

But in response to COVID-19, carriers have collectively adopted a new strategy of “blank sailings” and idling a significant portion of their fleet. Blank sailings are cancellations of entire voyages and reflect a change in strategy away from a market-share race to one of margin maximization. For this to work, all the carriers need to be coordinated and so far, they have been. Weekly blank sailings reached over 200 per week in April.1 Alphaliner, a proprietary database for the liner shipping industry, reported that at the end of May 2020, 551 vessels, representing 12% of the total capacity of the industry, were laid up in ports in support of this strategy.2 The logic behind this move is straightforward—by limiting capacity, the market can support higher rates.

Carriers staying afloat

This profit-maximization strategy carried the industry through the second quarter. Maersk, for example, reported lower volumes in the first quarter but was able to maintain profitability in its ocean operations.

The strategy does come at a cost, however. The average daily charter rate in 2019 was around $25,000 per day for an 8,500 TEU (twenty-foot equivalent unit) vessel. This means that an idle fleet could cost the industry over $4 billion over the course of a year. As a result, in June and July, we saw a redeployment of many of those vessels into the market. While carriers have been able to maintain higher rate levels (and several general rate increases in a short period of time), it’s unclear how long the carriers can maintain these elevated rate levels in the face of decreased demand and overcapacity.

Another—perhaps more traditional—survival strategy for the ocean shipping industry is the government bailout. Over $2 billion in government-guaranteed debt has been distributed thus far, with $1.2 billion collected by CMA-CGM, $0.4 billion by Hyundai, and $0.2 billion each by Yang Ming and Evergreen. Other major players, like Maersk, have leveraged their more stable financial position to raise investor-grade debt.

Shippers react

Shippers are also reexamining and revising their supply chain strategies in response to the societal and economic effects of the COVID-19 pandemic. As more consumers become acutely attuned to price concerns, many manufacturers are focusing on increasing the value of their products. At the same time, the pervasiveness of empty supermarket shelves has challenged the perceived benefits of “lean” supply chains. Finally, after being pushed to the back burner for the first half of 2020, supply chain sustainability is reemerging as a core objective for shippers.

Cost has always been a key focus in the world of ocean shipping. Now, with unemployment at staggering levels, value is also becoming increasingly critical to consumer brands. Recently, Alan Jope, the CEO of Unilever told Bloomberg Business Week, “Companies, ourselves included, should be thinking about value propositions and making sure that cash-starved consumers are able to access high-quality products at the lower-cost end of the pricing spectrum. And we’re busy with that.” As a result, international supply chain owners will need to implement an even tighter focus on cost as well. They will certainly need to rethink their network and take advantage of opportunities to shift away from air to ocean and to test for cracks in ocean carriers’ pricing resolve.

Resiliency has emerged as a theme across supply chains. Due to long lead times and service variability in ocean shipping, shippers have traditionally increased resiliency by increasing inventory levels. In response to COVID-19, however, shippers are beginning to look at resiliency differently, as evidenced in a recent Kearney study, “COVID call to action: supply chain resiliency beyond the pandemic.” During the pandemic, shippers struggled through challenges in basic execution and inventory management, and now they are looking at digital transformation as the real solution. In the ocean industry, our clients are developing strategies to partner with carriers and forwarders that are committed to higher service reliability and are investing in new in-transit visibility solutions. These partners will ultimately sync up with planned investments in the shippers’ own planning and execution solutions.

While resiliency is top of mind today, sustainability is on deck. In the transportation industry, cost and sustainable practices often go together, and shippers have found serendipity in ocean’s lower carbon footprint (relative to alternatives) and cost efficiency. Forward-thinking shippers are now exploring (and building) solutions like short sea shipping for the United States, Mexico, and Canada. These solutions are sub-scale today, as shippers are paying higher prices. However, the strategic value of moving volume off the road (for sustainability) and off the rail (for pricing leverage) has these shippers convinced the concept is the right answer for the long term.

Notes:

1. Costas Paris, “Ocean carriers idle container ships in droves on falling trade demand,” Wall Street Journal (April 8, 2020): https://www.wsj.com/articles/container-ship-operators-idle-ships-in-droves-on-falling-trade-demand-11586359002

2. “Idle box ship capacity reaches record high: Alphaliner,” Ship & Bunker (June 3, 2020): https://shipandbunker.com/news/world/698567-idle-boxship-capacity-reaches-record-high-alphaliner#:~:text=Idle%20capacity%20in%20the%20container,11.6%25%20of%20total%20global%20capacity.