Emerging from 2019, trucking industry players widely shared a sense of uncertainty about how 2020 would play out. While trucking generated a whopping $791.7 billion in revenue in 2019, just 1% less than 2018’s revenue, the year was broadly characterized as a tough and challenging one for the industry. Excess capacity (built during the growth periods of 2017–18), relentlessly rising costs, the slowdown of freight market volumes, and tariff wars, all combined to further depress what were already unsustainable rates. It’s understandable why, against this backdrop, there were nearly 800 trucking company failures in the first three quarters of 2019.

On the positive side, trucking remained an essential business and a key player in the United States’ economy in 2019. The American Trucking Associations’ (ATA’s) recently released report, “American Trucking Trends 2020,” stated that the industry moved 74% of the nation’s tonnage freight in 2019. Many remained optimistic that industry dynamics would improve starting in the second quarter of 2020 and hold steady throughout the second half of the year.

Various data points, like the ATA Tonnage Index and anecdotal evidence from carriers, did indicate a strong first quarter especially with the surge in consumer-staple buying due to the COVID-19 pandemic. However, this strong showing was largely short lived, as the virus continued to rage, and a nationwide shutdown ensued. The industry saw a 10.3% decrease in the Tonnage Index in April compared to March.1

As states started to reopen, the Tonnage Index did see an 8.7% increase in June compared to May.2 Based on current market dynamics, the latter half of the year looks to stabilize and improve, but uncertainties will continue to be a recurring theme, especially as the pandemic show signs of resurging on a regional basis.

Business as unusual

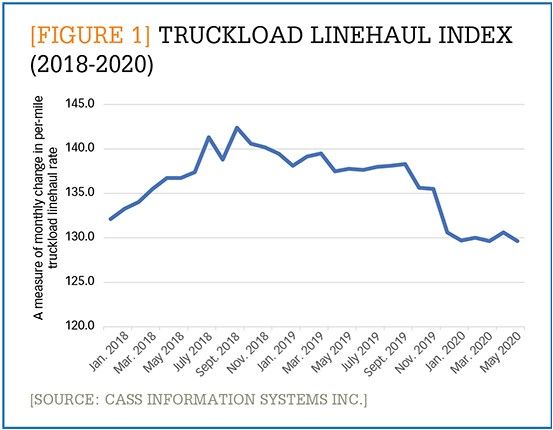

While regions continue to re-evaluate their reopening phases, the freight market is slowly finding its footing and continuing to truck along. The Cass Linehaul Index, which many transportation industry executives and analysts consider to be the most accurate gauge of freight volume and market conditions, shows that 2020 rates have fallen back to pre-2018 levels (see Figure 1). This is partially because, although contractual rates are heavily influenced by recent spot market movements, they are, in general, more stable and are reliant on annual cycles. Coming into 2020, contractual rates continued to remain under pressure from shippers due to the soft 2019 spot market and oversupply of capacity. As the figure shows, rates decreased 6% year-over-year in January, and the COVID pandemic and related economic repercussions had limited, if any, impact at that point. Throughout the first half of the year, the linehaul index remained consistent, averaging a –0.1% month-over-month change.

Enlarge this image

While the impact of the pandemic on contractual rates will be not be immediate, we could see upward movement as we enter 2021. The current FreightWaves July Outbound Tender Volume Index is showing that truckload volumes have recovered faster than expected during the pandemic and remain up 25% over 2019 and 23% above 2018.3 Typically there is a seasonal drop off in volume from July 4 to October. There is little evidence, however, that the drop off this year will be significant. As regional lockdowns loosen and consumer demand reestablishes itself, freight volumes should rise. As freight volumes grow, carriers will become more selective of the loads they carry versus earlier stages of the pandemic. The latest analysis by DAT Solutions is showing national dry van spot rate continuing to climb closer to contractual rates.4

What does all of this mean? Overall, the market is signaling that contractual rates have likely bottomed out and should rise during the next renewal cycle. While carriers are in a good position this summer, the trucking industry is still far off from 2019 levels, and uncertainties are tempering the optimism. For the savvy shipper, this may be an opportune time to reassure their transportation providers about their partnership, while locking in improved rates before spot rates push contractual rates upwards.

Change as a constant

Other uncertainties that could affect operations for truckers in the near term include changing regulations, increased use of technology, and persistently rising costs. For instance, the Federal Motor Carrier Safety Administration published the long-awaited final rule on changes to hours-of-service (HOS) regulation. Many in the industry appreciate the flexibility of the new rules, effective September 29, 2020, but also question its effectiveness on safety.

Meanwhile carriers must also contend with rising insurance premiums caused by increased, and sometimes intensive, litigation; jury awards; and highly unfavorable settlements. According to the American Transportation Research Institute’s “2019 Operational Cost of Trucking” report, insurance premiums have increased 12% year over year, becoming a top concern for carriers. Insurance premiums could rise even further if a proposed amendment to the INVEST in America Act passes. The amendment would raise the minimum amount of liability insurance that carriers must hold from $750,000 to $2 million. This increase may drive up costs even further, especially for smaller carriers, which could result in even tighter market capacity and higher rates.

As a result, many carriers are looking to do more with less and to do more remotely, especially given COVID-19. They are beginning to more fully embrace technologies like optical character recognition, robotic process automation, and machine learning. These technologies will help streamline and automate manual processes such as accounts payable, leading to increased efficiency and cost effectiveness.

The new norm for shippers

No doubt, the COVID-19 pandemic has had unprecedented impact on the supply chain and our economy due to its scale and depth of disruption—domestically and globally. Moreover, there appears to be no clear end in sight. However other significant disruptions—including 9/11, Ebola in 2013–16, SARS in 2002–2003, and natural disasters (such as tsunamis)—have occurred in the past. This is unlikely to be the last one that we’ll see.

What do shippers need to do, both in the near and long term, to better prepare for such disruptions, and how should they pivot to improve flexibility and resilience within their supply chains? A key trait of high-performing organizations is that they seek out and adopt transferable best practices from peer and non-peer groups. They also focus on controllable aspects of their business that are governed by data, like cost and operational efficiency. Fundamentally, a disciplined focus on cost control and operational efficiency enables the execution of contingency plans through gains in “financial bandwidth.”

Shippers should review and renew their freight rates today, as rates are approximately 6% lower than they were in 2019. They should take advantage of market softness and leverage competitive bidding and comprehensive contracting, even if it is “off cycle” for them. Contractual rates seem to have bottomed out, and the next renewal cycle may see increases. They should renew their rates whether they have significant freight today or not, because doing so should provide some level of security when freight picks up and capacity tightens due to increased volume across the markets and/or reductions in fleet count.

Shippers should also evaluate their entire freight network and lane utilization. This process will help them better negotiate contracts, forecast accurate cost models, and prevent future spend leakage. They should consider sharing demand planning details to help their partners plan for assets to support their business. These steps will help reduce complexity and resulting cost for both themselves and their carriers. Finally, shippers should consider improving dock efficiencies as the new HOS regulations and electronic logging devices will increase visibility and scrutiny on driver hours and utilization.

Pandemic or not, one thing is certain. High-performing organizations will constantly seek to adapt to new conditions and changing market dynamics. Those companies that have invested in cost and data management while still valuing flexibility will stand a far better chance of weathering future disruptive events and reaping benefits compared to their competition.

Notes:

1. “ATA Truck Tonnage Index Jumped 8.7% in June,” American Trucking Associations press release (July 21, 2020): https://www.trucking.org/news-insights/trucking-moved-1184-billion-tons-freight-2019

2. Ibid

3. Seth Holm, “Volumes stay strong, up 25% year-over-year in a recession,” FreightWaves (July 18, 2020): https://www.freightwaves.com/news/volumes-stay-strong-up-25-year-over-year-in-a-recession

4. Dean Croke, DAT Freight & Analytics (July 15, 2020): https://www.dat.com/blog/post/recent-outbreaks-create-uneven-freight-recovery