The COVID-19 disruption to the 2020 economy and subsequent recovery have hit freight modes hard, and the industry faces a weak outlook for 2021.

At the depth of the short pandemic recession, retail sales, shipments, and inventories all fell, as businesses closed and consumers did not shop for goods except for staples and groceries. Carriers that did not transport essential goods saw sharp declines in demand, leading to idled equipment and layoffs.

However, the very large U.S. federal fiscal stimulus put checks in consumers’ pockets while supplementing unemployment insurance payments. As a result, goods purchasing behavior, especially via e-commerce, reversed sharply in the third quarter with a record rapid quarter-to-quarter pace.

But as stimulus program payments have dwindled, this goods spending is fading. At the same time the virus spread is threatening another round of business closures and is temporarily increasing unemployment again. The outlook for 2021 freight volumes is for weaker freight tonnage, driven by fading economic growth, already rebuilt inventories, and slowing consumer spending on goods as opposed to services.

The pace of modal growth will depend on varying conditions affecting each mode’s customers as well as areas of continued competition between modes. A key element of the modal demand outlook will be how much the strength of the e-commerce portions of the economy balances out weaknesses in resource commodity sectors such as energy and agriculture exports.

Our analysis of underlying 2021 macroeconomic and industry forecasts, which were prepared in November, sees overall baseline 2021 freight tonnage volumes slowing 0.7% from the 2020 base. These forecasts include important assumptions, including the widespread distribution of a vaccine in the U.S. in the second and third quarter of 2021 but no new substantial federal fiscal stimulus program or trade policy shifts. Risks around this forecast are high given the large remaining unknowns about the course of the pandemic, consumer sentiment, and new government fiscal policy in 2021.

The 2021 U.S. macroeconomic forecast has been revised down, now at 3.1% growth in real gross domestic product (GDP). The very strong recovery seen in the second half 2020 is fading with lingering unemployment and service sector weakness coexisting with a new wave of virus spread. The U.S. economy is also facing a fiscal cliff with some government benefits payments stopping at the end of December, which will work to restrain a stronger recovery.

We expect the 2021 GDP growth to come from consumption increases of 3.6% as well as growth in residential and busines investment. Imports and exports are forecasted to continue to increase, although net exports will be a drag on 2021 GDP, as imports outpace exports by 0.8%. This outlook includes sustained record-low interest rates and constrained inflation, which will support spending by households not affected by unemployment. The freight-intensive construction sector is expected to fall 0.6% in 2021, as the decline in commercial construction won’t offset the 2.6% increase in residential construction.

Quarterly 2021 GDP growth will be higher in the second half of 2021, as the uptake of the vaccine allows more opening of the economy and increased consumer confidence later in the year.

Implications of weak freight tonnage

The economic conditions driving 2021 freight tonnage are not a return to the pre-pandemic pace of freight demand. IHS Markit’s forecast of a 0.7% decline in total freight tonnage will leave 2021 as another challenging year for carriers, with many seeing weaker demand than during the second half of 2020. There remains a structural mismatch in capacity, as freight networks have insufficient capability to handle e-commerce business at the same time as they have excess capacity aligned to support other supply chains. So, the freight outlook varies by modal segment and customer base.

The freight growth in 2021 is calculated from the base of the highly unusual 2020, which saw above-trend shipments in the second half of the year. For supply chain managers, this freight forecast outlook implies a continuation of high rates in intermodal, air, and some trucking segments, but potential rate relief in bulk waterborne and carload rail rates.

Capacity and operational limits will still impact most modes in 2021, especially in the first half of the year. For shippers, the pace of sales volume growth will be more moderate than in the second half of 2020, with a few exceptions such as for those export commodities that were impeded by operational and equipment availability. There remain significant risks to these baseline forecasts, including potential impacts from policy and/or business and consumer confidence, whether related to COVID-19 or other 2021 market disruptions.

Air and intermodal lead

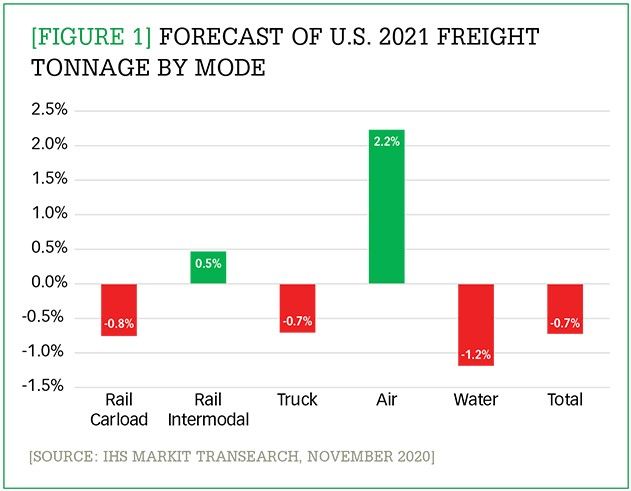

Not all modes of freight transport will see the same pace of 2021 growth; the IHS Markit Transearch 2021 tonnage forecast reveals significant differences by mode. While the overall freight tonnage forecast is for 0.7% decline in the United States, air and rail intermodal are forecast to see tonnage growth, continuing their strong end to 2020. These Transearch modal freight tonnage forecasts for 2021 are summarized in Figure 1.

Enlarge this image

The 2021 air cargo and rail intermodal tonnage are forecasted to increase 2.2% and 0.5%, respectively, mostly as a reflection of the strength of e-commerce-related shipping. The air cargo business also anticipates demand being driven by vaccine and personal protective equipment (PPE) shipments. The air cargo forecast reflects restoration of some passenger aircraft belly capacity that had been grounded for most of 2020 due to the sharp, sustained drop in air passenger traffic.

Meanwhile IHS Markit forecasts that waterborne tonnage will decline, down 1.2% in 2021. This drop will be driven by further declines in coal volumes and a modest drop in farm products tonnage due to constrained exports. We also believe that the boom in consumer spending on goods compared with services spending will fade in 2021. This development will affect overall trucking demand, as will continuing weaknesses in sectors such as oil and gas exploration and production. Within trucking, the less-than-truckload (LTL) sector is forecasted to benefit from e-commerce demand with tonnage increasing 0.3% in 2021. Rail carload tonnage is forecasted to fall 0.8%, as a result of weakness in the traditionally important coal business as well as modest declines in agriculture products shipping. Truckload trucking will see a decline of 0.6% in comparison with the 2020 recovery period, when volumes went up due to inventory rebuilding and e-commerce. It will also experience capacity constraints from limited driver workforce growth, despite lingering high unemployment in the overall economy.

The overall decline forecasted for freight tonnage is driven by the huge importance of trucking (79% of total tons) and rail carload traffic (12% of total tons). With industrial production growing, but slowly in 2021, as manufacturing and agriculture move up from the depths of 2020 production and shipments levels.