The past few years have been turbulent ones for the logistics industry, leaving many supply chain professionals asking themselves, “Whatever happened to predictability?”

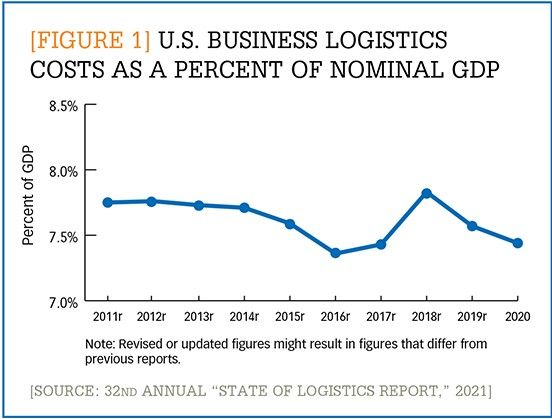

In particular, 2020 was a chaotic year of sudden stops, stuttering starts, dips, drips, and explosive rises—all while trying to reroute assets on the fly. As a result of this unpredictable, pandemic-driven year, U.S. business logistics costs fell 4.0% to $1.56 trillion, or 7.4% of 2020’s $20.94 trillion U.S. gross domestic product (GDP), according to the Council of Supply Chain Management Professionals’ (CSCMP’s) 32nd Annual “State of Logistics Report.” (See Figure 1.)

[Figure 1] U.S. business logistics costs as a percent of nominal GDP

Enlarge this image

The main driver of that drop was the decrease in inventory carrying costs, which plunged 15%, due to the sudden decline in manufacturing and commerce early in the year caused by pandemic shutdowns.

This meant transportation volumes also fell. However, costs for many transportation and warehousing services rose, as networks dealt with capacity shortages, port congestion, and major shifts in consumer demand as well as assets that could not be deployed or redeployed efficiently. According to the report, 2020 exposed logistics systems that were optimized for cost and efficiency but were fragile and lacking resiliency in the face of disruptions.

“The 2020 upheaval of supply chains created chaos that placed gigantic demand on logistics, resulting in higher prices for logistics services despite a shrinking economy,” said Michael Zimmerman, one of the authors of the report and a partner with the consulting company Kearney at a press conference. “At the same time, due to halted economic activities during lockdowns and decreases in financial costs, logistics costs account for a lower percentage of GDP at 7.4% compared to the 7.6% in 2019.”

Sector-by-sector breakdown

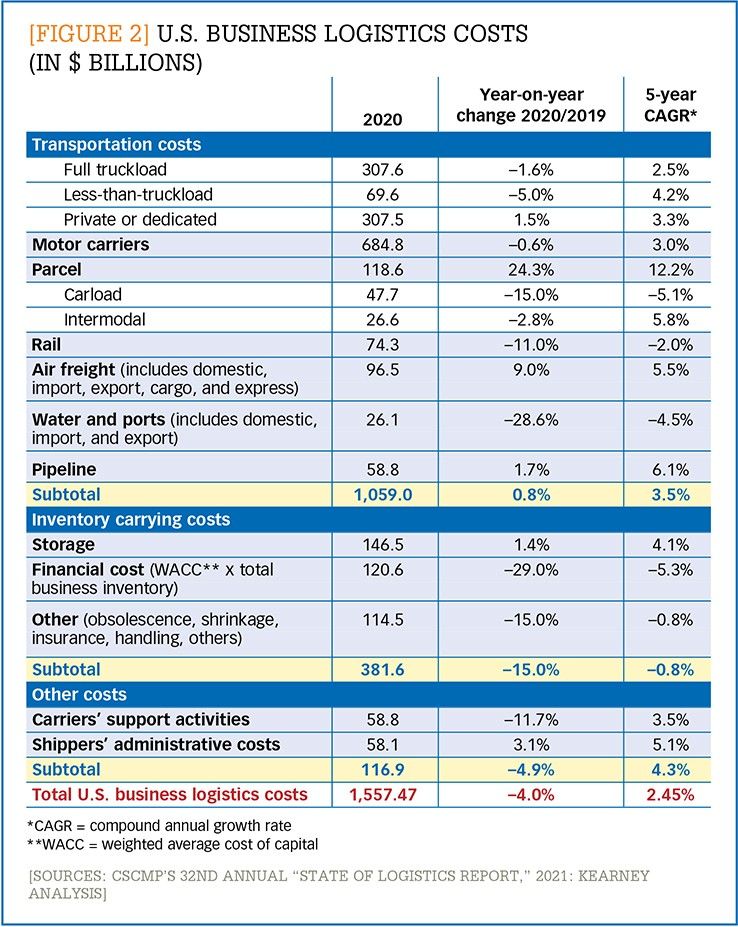

Some segments of the market did better than others in riding out the storm. Figure 2 and the summaries below provide a quick look at how some of the key modes and segments fared. (For more in-depth analysis, see the report itself, which can be downloaded from cscmp.org.)

- Motor carrier freight: Trucking costs, the biggest segment of U.S. logistics spend, fell by 1.6% year over year. A strong fourth quarter and a continuing economic recovery, however, indicate that rates will remain high through 2021. One silver lining of the pandemic is that the need to avoid “touch” processes drove many trucking firms to finally embrace digitization. New digital technologies, such as online freight booking and digital bill of materials, should lead to improved services levels in the future, predicts the report.

- Parcel: Homebound consumers caused e-commerce to explode in 2020, growing by 33% to $792 billion, or 14% of all retail sales. This rapid rise fueled a 24.3% year-over-year increase in parcel shipping spend, which totaled $118.6 billion, but it also had shippers scrambling to adjust their delivery offerings and solutions.

- Rail: Volumes and revenue were down overall for the rail industry, with spend dropping 11% year-over-year to $74.3 billion. This drop was due to reduced volumes in industrial products and coal. Intermodal, however, saw smaller declines as high trucking prices pushed some shippers to switch modes.

- Air freight: Air cargo costs totaled $96.5 billion in 2020, a 9% increase over 2019. Rates remain “shockingly high” even in mid-2021, as most airlines have not recovered from the cancellation of passenger flights in 2020. The authors expect that demand will continue to exceed supply in 2021.

- Water: Logistics costs associated with on-the-water shipping dropped 28.6% year over year, in part due to a one-time reclassification in the report’s methodology. However, the decrease in exports and in traffic on domestic waterways would have kept costs down substantially regardless of the recalculation. Rates and volumes, however, soared in late 2020 as retailers restocked and have remained high ever since.

- Pipeline: The COVID-19 pandemic brought about a sharp and unforeseen bust in the oil industry. However, the gas industry was one of the few areas that remained relatively unaffected by the pandemic. As a result, pipeline logistics costs rose by 1.7% year over year.

- Warehousing: The e-commerce boom spurred high demand for warehousing space especially in urban locations. At the same time, warehouse flows have become more complicated and labor conditions remain tight, leading more warehouses to turn to automation.

- Freight forwarding: While volumes declined in this segment, higher rates led to higher 2020 revenues. The report predicts that freight forwarding will see fierce competition as more traditional providers face off against new digital startups, carriers seeking to become end-to-end providers, and large monoliths such as Amazon and Maersk. They also predict more mergers and acquisitions ahead.

- Third-party logistics providers (3PLs): While many 3PLs saw higher revenue last year, some experienced cost increases, which harmed their profitability. The report authors predict that as supply chain and logistics become more complex, the sector will continue to grow.

[Figure 2] U.S. business logistics costs (in $ billions)

Enlarge this image

More change ahead

In spite of the upheaval of the past year, the report authors are hopeful. Logisticians proved themselves capable of quickly abandoning old plans, solving new problems, and handling disruptions. This ability to adapt will serve logistics professionals well in the future, as the report predicts that the pandemic’s aftereffects and “new surprises” will force logistics professionals to continually change their plans.

“There is no relief in sight,” said Zimmerman.

The list of potential future disruptors includes the trend toward “right shoring,” continuing technological advances, and climate-related disasters—to name just a few. Right shoring involves a company creating a mix of offshore and nearshore (or “reshored”) manufacturing operations. The goal with this trend is for a company not to be overly dependent on one supplier or region for its manufacturing operations and for production to be closer to consumption. While the idea on the surface is appealing, moving manufacturing operations out of low-cost countries in Asia is a difficult process and will make logistics needs even more complex.

The pandemic also accelerated interest in technology that improves visibility and automation. For example, Kearney has seen increased interest in control tower technology to improve and centralize companies’ access to critical data. Additionally, the report authors expect to see increased use of distributed sensors to collect that data and artificial intelligence and machine learning to analyze it. Meanwhile the difficulty of finding labor and keeping that labor safe from a contagious disease has fueled interest in automation technology and robotics.

Finally, the effects of climate change and extreme weather are making sustainability an increasing concern for logistics processes and companies. Logisticians are responding by taking a closer look at measures such as electric vehicles and alternative fuels; network redesigns, such as locating warehouses close to inland ports; and more efficient forms of transportation, such as rail.

The report authors also predict that the cost of logistics will rise as the scope of what the field encompasses grows. As an example, they point to last-mile delivery, which used to be a “domestic” activity performed by consumers and is now an increasingly commercial one.

After the stresses of last year, logistics executives are focused on rebuilding their supply chains to be more resilient. “State of Logistics Report” authors don’t expect these changes to be minor. They predict that in 2021 and beyond, executives will be fundamentally rethinking and redesigning their logistics networks. “In 2021, even if conditions prove less volatile, the changes may be more profound,” concludes the report.

The “State of Logistics Report” is authored by the consulting company Kearney for the industry association, the Council for Supply Chain Management Professionals. It is sponsored by Penske Logistics.