Considering the attention being directed globally toward the pursuit of sustainability, it is not surprising that supply chains of all types have made highly visible commitments to achieving sustainability goals and objectives.1 For many companies, a key aspect of achieving those goals will be how well they collaborate with their third-party logistics providers (3PLs), fourth-party logistics providers (4PLs), and other logistics service providers. Recognizing the important role of 3PLs, the “2022 26th Annual Third-Party Logistics Study,” to be released at the CSCMP EDGE conference, will focus on investigating this topic.2

A closer look at ESG

Sustainability can be defined in a number of different ways from focusing solely on the environment to encompassing diversity, equity, and inclusion (DEI); corporate social responsibility (CSR); and the notion of the “circular” economy.

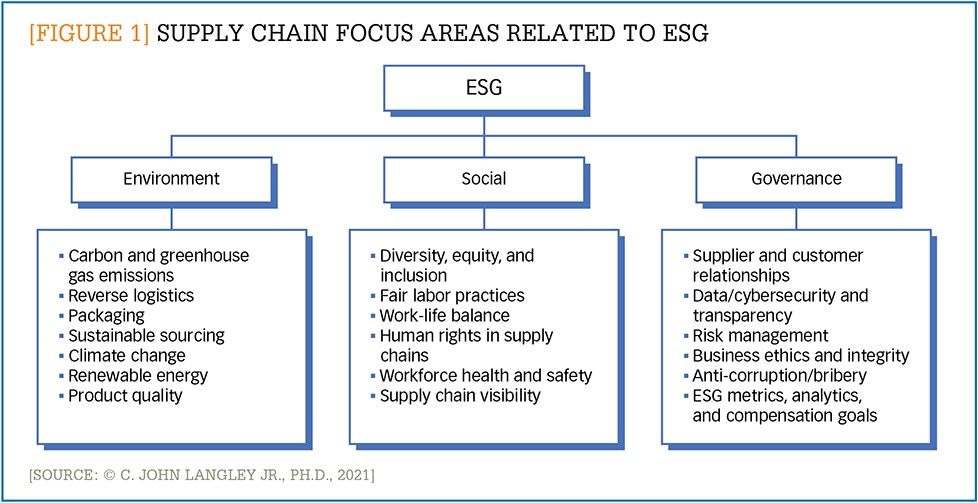

For the purposes of this article (and the “Annual 3PL Study”), the concept of ESG (environmental, social, and governance) will be used to anchor our reporting on how 3PL-customer relationships can impact sustainability in the context of supply chains. The ESG framework provides a well-structured approach for better understanding the progress being made towards environmentally friendly, socially acceptable, and ethically responsible business practices. The three elements of ESG and their connection to supply chain management are outlined in Figure 1 and below.

[Figure 1] Supply chain focus areas related to ESG

Enlarge this image

Environmental. Generally, environmental goals relate to reducing the overuse and destruction of natural resources and threats to all forms of life. Initiatives that are designed to address tactical environment concerns include the development of “carbon-neutral” activities and processes; biodegradability; alternative and renewable energy sources; reverse logistics; and circular supply chain strategies, to name just a few. One opportunity area that is relevant to many 3PL-customer relationships and provides numerous opportunities to enhance environmental sustainability is transportation management. Specific examples in this category would include fuel efficiency, capacity utilization, advances in electric vehicle technology, and improved vehicle scheduling and management.

Social. The social element of ESG focuses on identifying and managing the impacts of organizations and their supply chains, both positive and negative, on people.3 Recent experiences have highlighted the importance of issues such as: diversity, equity, and inclusion; work-life balance; fair labor practices; and human rights in our supply chains. The inclusion of supply chain visibility reflects the importance of preserving these principles throughout supply chains.

Governance. This component of ESG reflects the commitment of an organization to responsible decision-making and execution. Most frequently, this involves actions taken by senior and executive management and boards of directors. Just as “good processes lead to good results,” good governance should promote and foster sustainability both internally within the organization and externally with other supply chain participants and stakeholders. Some examples that relate to how 3PLs and their customers can collaborate on sustainability include improving relationships; increasing data and cybersecurity; and using visibility to help address anticorruption/bribery.

Among respondents in this year’s “Annual 3PL Study,” 85% of 3PL users and 83% of 3PL providers said that ESG is included in their organization’s supply chain and growth strategies. Currently, many supply chains are further along the maturity cycle in the area of environmental progress than social or governance. This is understandable when you consider the attention most organizations have focused on improving the efficiency and sustainability of their internal manufacturing operations and logistics activities. Social and governance areas, however, are receiving significant additional attention as ESG initiatives move forward.

This year’s survey, for example, asked respondents to indicate areas of importance related to ESG criteria. Top focus areas include workforce health and safety, government anticorruption/bribery, diversity and inclusion, sourcing, and visibility throughout the supply chain. Survey responses from 3PL users indicate that the areas of greatest potential include sourcing/procurement, supplier management, manufacturing, transportation, and warehousing.

Collaboration is key

Achieving ESG objectives across participating organizations in the supply chain ecosystem requires meaningful and effective collaboration. As 3PLs and their customers begin to take a serious look at what needs to be done in the areas of sustainability and ESG, the development of an objective and accurate base case is essential. Like all transformational efforts, ESG initiatives need to be enhanced from an “as-is” or current state to a “to-be” or future state. In the case of sustainability, the priority should be to develop a comprehensive and measurable understanding of the current state of sustainability and to assess key areas to be targeted for improvement.

This process can be initiated by either party and may be facilitated by other stakeholders, such as consumers, investors, and corporate partners. We have seen cases where big box retailers and consumer packaged goods companies, for example, will work only with transportation providers that meet specific goals relating to efficiency and sustainability. At the same time, some large providers, such as FedEx and UPS, have announced internal sustainability goals. Among the available resources that encourage businesses to manage logistics in an environmentally responsible way is the Environmental Protection Agency’s SmartWay program that reduces transportation-related emissions by creating incentives to improve supply chain fuel efficiency.4

Successful sustainability efforts along the end-to-end supply chain require that participating members are aligned along ESG practices while not unnecessarily compromising the progress already made at any individual firm. Customer organizations that have developed effective supplier relationship management strategies with their 3PLs should benefit accordingly.

Collaboration will also be essential for responding to the some of the challenges that supply chains face in implementing effective ESG measures. According to survey findings from the “2022 26th Annual Third-Party Logistics Study,” top challenges include the cost of implementation, changing regulatory requirements, and a lack of tools and technologies to support ESG programs. To address some of these concerns, 3PLs and customers will need to share costs and investments. Addressing these issues ahead of time and assessing each party’s willingness to make investments is crucial to the success of the relationship between a 3PL and its customer.

It is also important to recognize that as supply chain organizations promote and pursue objectives relating to ESG, they need to do so in a way that is economically and financially sustainable. A reasonable expectation is that organizations and their supply chains have the financial well-being to accommodate investments that will yield positive results. While altruism may be a virtue, businesses must be financially viable in order to contribute to the pursuit of sustainability.

A serious business

The focus on ESG in supply chains is serious business. Supply chains are broad, encompassing everything from sourcing and packaging to warehousing and final-mile delivery, and ESG is applicable at every point. Network optimization, reduced-emission equipment, and efficient buildings can reduce carbon and greenhouse gas emissions, while increased supply chain visibility and traceability can provide insight into sustainable sourcing and the importance of respecting and preserving human rights.

As organizations look to make progress in the areas of environment, social, and governance issues, today’s supply chains leaders will need to step up to the task. Making progress in these areas will shape supply chains of the future. A focus by 3PLs and customers on collaboration to achieve these priorities has the potential to create meaningful advances in meeting the goals of sustainability and ESG. At the same time, attention to the ESG process can be a very useful element for building and strengthening the relationship between 3PLs and customers.

Authors’ Note:The authors would like to thank Mindy Long of Mindy Long Freelance LLC for her contributions to this article.

Notes:

1.. For an interesting article on the topic of supply chain sustainability, see Pierre-Francois Thaler, “Will this be the decade of supply chain sustainability?” Supply Chain Quarterly (October 23, 2020): https://www.supplychainquarterly.com/articles/4065-will-this-be-the-decade-of-supply-chain-sustainability

2. C. John Langley Jr., Ph.D. and NTT DATA Inc., 2022 26th Annual Third-Party Logistics Study, forthcoming September 2021. This study is sponsored by NTT DATA, Penske, and Penn State University. Copies will be available for download at https://www.3PLStudy.com.

3. United Nations Global Compact: https://www.unglobalcompact.org. The United Nations Global Compact is a nonbinding U.N. pact to encourage businesses and firms worldwide to adopt sustainable and socially sustainable policies and to report on their implementation.

4. For additional information please see https://www.epa.gov/smartway.