What’s the biggest obstacle to any major initiative such as digitally transforming your supply chain operations? In many cases, it’s the fear of change. Consider: In late 2019, ToolsGroup conducted a global survey looking at the state of companies’ digital transformation efforts in supply chain planning. How far along were they in implementing technologies such as artificial intelligence, machine learning, the internet of things (IoT), and digital assistants to the planning process? At that time, we found that 30% of respondents believed that the fear of change was holding back their efforts.1

Since then, the most ruthless unplanned change imaginable swept the globe, decimating some industries while creating unprecedented opportunities in others. Supply chain disruptions happened from difficulty procuring raw material on one end to radically changing customer behaviors on the other. Most organizations had to adapt, and fast. While some were threatened by declining business, others stood to lose out by failing to capitalize on demand spikes and other big changes in consumer behavior.

So, what happens when the planned change of a digital supply chain transformation effort meets the unplanned change of a global pandemic? To find out, we decided to revisit our study. In collaboration with the Council of Supply Chain Management Professionals (CSCMP), we launched a new version of the global survey called “Digital Transformation in Supply Chain Planning: 2021.”

We sent it out in January 2021 to 289 supply chain executives, managers, and planners/practitioners from manufacturing, retail, consumer packaged goods, aftermarket parts, wholesale-distribution, and third-party logistics services (3PL) firms, as well as consulting organizations. We received back 211 usable responses. Of those we surveyed, 74% said that changes wrought by the COVID crisis had influenced their digital supply chain planning transformations.

Our research led us to conclude that many organizations this past year were driven to quickly implement digital supply chain solutions by necessity, rather than invention. The unplanned change of the pandemic helped push many companies past their fear of leading a planned digital change effort.

Jump start the revolution

Most survey respondents said that the pandemic affected their business to some extent. This was primarily by exposing process vulnerabilities (49%), causing supplier instability (45%), and increasing demand for their products and services (45%). Declining demand (31%) and staffing shortages (30%) also affected many firms. Only 3% of respondents said the pandemic has had no effect on their business.

In many cases, the pressures that COVID put on their supply chains prompted companies to reprioritize their investments in digitization. Forty-two percent of respondents said that the pandemic accelerated their supply chains’ digital transformation, while 17% said the pandemic shifted their organizations’ digitization priorities in some way. (See Figure 1.)

[Figure 1] How has the COVID-19 pandemic influenced your supply chain digitization strategy

Enlarge this image

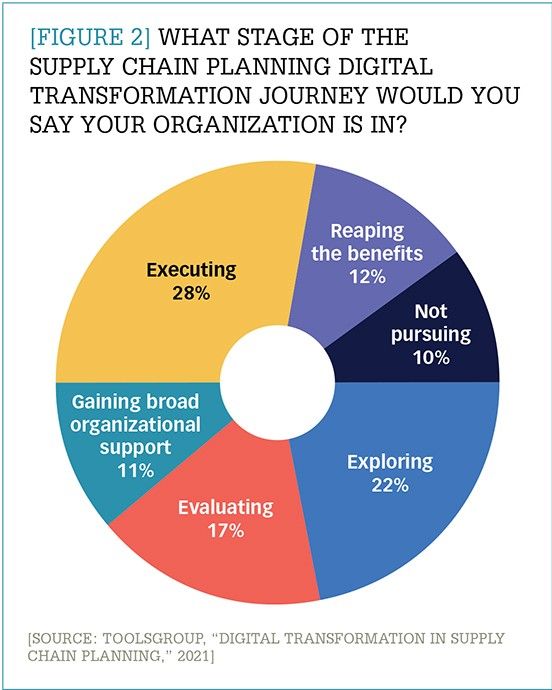

In our original survey in 2019, we found that a full two-thirds of the respondents had not yet executed a digital transformation of their supply chain planning process. They were either not yet pursuing a digital strategy or were only in the early stages of the transformation effort—exploring and evaluating technologies and trying to gain organizational support. (See the sidebar for more information on the different stages of a digital transformation.) Only 7% of respondents said they were reaping the benefits of a digital transformation. This time around, however, a higher percentage of organizations (12%) reported that they were already reaping the benefits of digital transformation. (See Figure 2.)

[Figure 2] What stage of the supply chain planning digital transformation journey would you say your organization is in?

Enlarge this image

One key factor that seems to correlate to how far along companies are in their transformation efforts is executive involvement. Half of the firms in the “reaping the benefits” stage say their transformation is being led by their CEO. In contrast, the majority of those not pursuing a strategy say their digitization efforts are being led by line-of-business managers.

Digital defense

Unsurprisingly, it’s the more mature, digitally transformed supply chains that have weathered the storm of the pandemic most successfully. Fifty-four percent of the companies in the “reaping the benefits” group said that they were managing COVID-related demand and supplier uncertainty “very well.” In comparison only 13% of those in the “evaluating” and “not pursuing” stages reported handling this area “very well.” This finding suggests that digital technologies and processes can help companies better manage disruptions.

Through our customers and partners, we’ve been able to see firsthand how much more resilient digitally mature companies were during the pandemic. For example, during the first COVID spike, an alcoholic beverage distributor was concerned that sales would plummet because consumers would no longer be able to drink in bars and restaurants. Fortunately, this company had been using advanced planning software to sense demand day-by-day at the stock-keeping unit (SKU) and point-of-sale level. By the start of March 2020, the system sensed a major shift in demand from “out-of-home” channels (restaurants and bars) to retail channels (supermarkets and corner shops). This was essentially a shift from business-to-business (B2B) to business-to-consumer (B2C) channels. Having sensed this change, the system started revising its March–June projections accordingly.

At first the planners were skeptical as the forecast looked almost too good to believe. However, the forecasts produced by the system for July–November were nearly perfect, increasing the team’s trust not only in the system but also the data model.

Obstacles to transformation

While the COVID-19 pandemic provided a strong impetus for companies to embrace new technologies, obstacles to digital transformation still remain. The biggest one this year has been that companies lack the skills needed to implement a digital transformation. This is understandable as digital transformations require advanced skills such as change management, negotiation, and decision-making, along with the traditional technical planning skills.

This awareness of a skills deficit has grown greatly since 2019. This year, 41% of respondents said that a skills deficit stood in the way of their company implementing its digital transformation plans; in 2019, that number was 23%. Part of that jump may be due to where companies are in the transformation journey. Skills deficits often rank as the highest obstacle for those in the early phases of transformation as companies are just beginning to assess the skills they will need to execute and reap the benefits of improvement. Given that 60% of organizations are still at pre-execution (not pursuing, exploring, evaluating, or gaining organizational support) stages of maturity, it seems likely that the skills deficit is a problem that is only going to get worse before it gets better.

Additionally, more respondents this year said that data quality/lack of data was a big obstacle to their transformation efforts than in the last survey: 34% in 2021 versus 25% in 2019. This figure’s growth is likely because more organizations have accelerated their transformation programs and have been forced to confront their data issues.

Different stages, different challenges

Our research also revealed that organizations face different types of challenges depending on where they are on their digital transformation journey:

- Companies not pursuing a transformation strategy are most likely to cite fear of change, lack of data, or a lack of investment as issues that are holding them back.

- Companies in the “exploring” phase are most likely to cite skills deficits as they struggle to develop a transformation strategy.

- Companies in the “evaluating” phase list three key challenges: risk aversion, lack of data, and skills deficits.

- Companies in the “gaining support” phase say fear of change is a top issue, as is the fear that they can’t prove a business case for transformation.

- Companies in the “executing” phase cite a lack of data as a key obstacle to moving forward. This makes sense because it is at this stage when data hygiene issues become most apparent and troublesome.

For sure, digital transformation isn’t easy and there are many roadblocks along the way. However, as we mentioned, our survey showed a clear correlation between digital transformation maturity and the ability to manage COVID-related demand and supply uncertainty and disruptions. Unfortunately for 16% of respondents, the pandemic caused them to either delay their transformation plans or put them on hold.

We would urge every organization whose digital transformation efforts are stalled to redouble their efforts to get them back on track. The COVID effect may be waning, but more disruptions are inevitable. The results of our two surveys so far, along with countless anecdotes from our customers and partners around the world, leads us to one stark conclusion: You can either be the architect of change in your organization or a victim of it.

Notes:

1. Caroline Proctor and Gregory Fowler, “Digital Transformation in Supply Chain—On Pace or At Risk?” Supply and Demand Chain Executive (December 2019) pp. 10–15.

The six stages of a digital transformation

As part of the survey, we asked respondents to characterize where their company was in its digital transformation efforts. We divided the transformation effort into six stages:

- Not pursuing: In this stage, the company is currently not investigating the use of digital technologies for supply chain planning.

- Exploring: This stage involves establishing the catalyst for change and ranking ideas by how well they fit existing business and supply chain strategies, organizational capabilities, and the needs of the customer.

- Evaluating: These companies are actively evaluating digital solutions, sometimes in a hands-on way.

- Gaining broad organizational support: This stage involves getting funding for a transformation effort and securing broad support from the supply chain organization. Organizational work is also being done such as setting up steering committees.

- Executing: At this stage, the company is implementing and deploying technology and trying to get people to adopt the required processes and tools.

- Reaping the benefits: Here the company has shifted to continuous improvement projects to scale and capture the full benefits of the digital transformation.