Despite another winter wave of COVID infections in early 2022, the underlying conditions affecting U.S. freight demand and the outlook for the rest of the year are quite different from what supply chain managers were facing a year ago. While IHS Markit is forecasting year-over-year growth for the freight market, we believe that it will be at a slower pace than in 2021.

To be sure, the U.S. is still in a pandemic, and consumers are again pulling back from spending on “socially dense” services. But despite the fact that the omicron variant set new infections records in the United States, the 2022 COVID-related disruptions are only an echo of those from 2020 and 2021. Instead, most of the economy (and schools) are still largely open, and goods demand has not softened as much, or as quickly, as many analysts assumed it would a year ago. As a result, the freight system currently is handling near-record volumes of cargo.

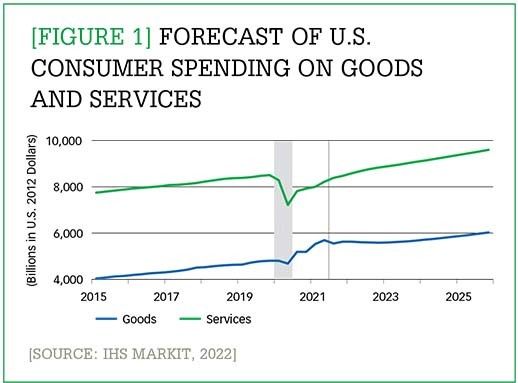

However, we expect the surge in goods spending will soon fade, as government stimulus program payments have dwindled and no new pandemic fiscal stimulus packages are on the horizon. Furthermore, as the infection rate eases post-omicron, we expect to see a gradual shift of consumption away from durable goods and back toward services. Figure 1 shows that the above-trend goods consumption of the last two years is about over, while services consumption has yet to recover to pre-pandemic levels. We expect this shift toward more services consumption will decrease demand for freight as we progress through 2022.

[Figure 1] Forecast of U.S. consumer spending on goods and services

Enlarge this image

Freight demand will also be affected by a deceleration in inventory restocking by businesses. Businesses were able to substantially rebuild their inventory before year-end 2021. While this helped boost Q4 2021 gross domestic product (GDP) growth, it reduces business’ need to restock inventory in 2022 (with a few exceptions, such as the auto industry). This, in turn, weakens the outlook for business investment and associated freight demand in 2022.

As a result, IHS Markit has revised its forecast for 2022 U.S. real gross domestic product (GDP) growth down to 4.1%. From a long-term perspective, this percentage still represents strong growth, but it is 1.6% slower than the economy grew in 2021. Therefore, our analysis of the underlying 2022 macroeconomic and industry forecasts prepared in January sees the overall baseline for freight demand still increasing, but at significantly slower pace as we move through 2022.

Modal outlook

The forecasted pace of growth for the various transportation modes will depend on conditions affecting each mode’s customers as well as continued competition between modes. For example, the booms for segments such as the at-home food and exercise equipment are over. Meanwhile the auto industry is still playing catch up in 2022, trying to recover from the severe chip shortage, which constrained production and shipping in 2021.

Among the key elements affecting modal freight demand in 2022 are the strength of the e-commerce portions of the retail economy and the outlook for commodity sectors such as energy and agriculture exports.

IHS Markit’s analysis shows continued strength in trucking and air cargo demand in 2022, driven by e-commerce shipping. Trucking demand will also benefit in 2022 from rail intermodal’s lingering difficulties handling higher demand volume. There will be weaknesses in bulk energy and construction commodity markets not offset by the increased pace of exports, which will affect carriers serving these markets and benefit shippers of related commodities.

The structural mismatch between freight network capacity and demand that has led to so much congestion and disruption in the last two years will linger well into 2022. Freight velocity will continue to be reduced, and the workforce level will continue to be inadequate to handle e-commerce business and evolving just-in-case supply chain inventory management practices.

It is essential to note that these forecasts include some important assumptions, including that the combination of vaccinations and natural immunity will prove effective against any new variants of COVID. As a result, the forecasts assume that we will see further opening of the economy during 2022. Also assumed is there will be no substantial additional federal fiscal stimulus programs following the Infrastructure Investment and Jobs Act of 2021, nor any significant trade policy shifts.

The risks around these forecasts are high given that there are many remaining unknowns, including the potential for major geopolitical disruptions in Europe, the Middle East, and Asia. New virus variants could also potentially arise, which could extend the pandemic. There are also many unknowns around consumer sentiment, workforce participation, and additional government fiscal and monetary policy shifts in 2022.

Implications for U.S. freight markets

The economic conditions driving 2022 freight demand are not a repeat of the booming goods consumption that overwhelmed supply chains in 2021, nor will there be a reversion to the pre-pandemic 2019 composition of freight demand.

Instead, the outlook for 2022 freight volumes is for weaker growth, driven by decelerating economic growth, mostly-already-rebuilt inventories, and slowing consumer goods spending. For supply chain managers, this forecast implies a slow step down from the record-high 2021 rates in intermodal, air, and some trucking segments. However, the potential rate relief is limited, as carriers are facing persistently higher costs for fuel, labor, and equipment, as well as many inefficiencies in their operations. Capacity and operational limits will still impact most modes in 2022, especially in the first half of the year, as container port congestion has lingered through January.

For shippers, the pace of sales volume growth will be more moderate than in 2021, allowing for better management of volumes, with a few exceptions—such as for those export commodities that were impeded by operational and equipment availability in 2021.

For carriers, 2022 brings the prospect of making progress on improving operations and better satisfying customers. Yet, they could also face potentially lower margins, as the extreme supply/demand imbalance that favored many carriers with high spot rates in 2021 will dissipate.