Projected economic growth has been significantly disrupted by recent major global events, such as Russia’s invasion of Ukraine and COVID containment lockdowns in mainland China. As a result, economic growth looks to be much lower than anticipated for 2022, with some large impacts for the freight market.

In the first quarter of 2022, strong U.S. imports and weak exports, fading government fiscal stimulus, and lingering supply constraints led to a -1.6% U.S. gross domestic product (GDP) growth rate. This quarterly decline was the first since the second quarter of 2020, when the world went into a short recession early in the pandemic.

As a result, S&P Global has updated its baseline economic forecast to reflect slower global and U.S. growth. However, we believe there will not be a recession in 2022. The forecast for 2022 U.S. GDP growth is now 2.4%, with global GDP growth of 3.0%. Neither of these are recessionary levels, yet growth is lower than forecasted prior to the Ukraine invasion.

Economic headwinds

Inflation remains an important headwind for the economy, as it dampens demand and increases operating costs. The U.S. Federal Reserve Board is raising interest rates to keep inflation closer to their targets. But a tighter monetary policy can’t immediately solve supply chain disruptions, just as it doesn’t shift spending from goods towards services.

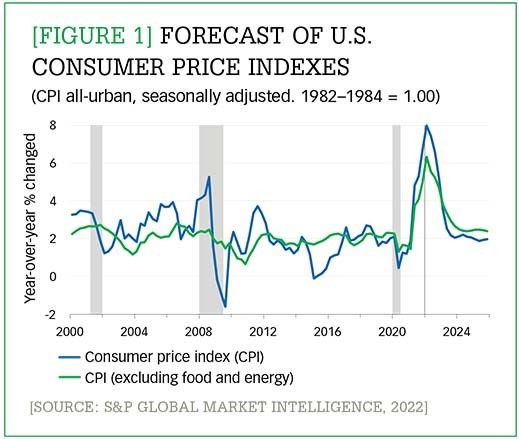

However, the 40-year high in U.S. inflation will eventually see the impacts of the end to monetary stimulus. Figure 1 shows how the Consumer Price Index (CPI) and the CPI excluding the volatile food and energy prices have hit a 40-year high. However, Figure 1 also shows our forecast for declines in the CPI to come.

[Figure 1] Forecast of U.S. consumer price indexes

Enlarge this image

Growth this year, success in slowing inflation, and avoiding a recession will depend in part on supply resilience. There are positive factors at work to improve supply conditions and combat inflation which include rising labor force participation, investments to increase capacity and labor productivity, an easing of transportation bottlenecks, and diversification of supply sources.

In addition to inflationary pressures, the U.S. economy must also deal with the fact that the impacts of the Federal government pandemic stimulus payments have faded while the new stimulus from the 2021 Federal Infrastructure Investment and Jobs Act won’t likely begin to affect the economy until late in 2022. Our baseline forecast of 2.4% growth assumes the Build Back Better spending program will not further advance in Congress. It also considers seven increases in interest rates by the Federal Reserve Board, as it moves quickly to reverse monetary stimulus and focus on constraining inflation.

We also expect to see business fixed investment growth weaken to 5.8%, down from 7.4% growth in 2021. Import growth is also forecasted to slow substantially, averaging 7.2% in 2022 after a 14% growth rate in 2021. Exports are forecasted to increase slightly to 4.8% growth after experiencing a 4.5% growth rate in 2021. This leaves net exports as a negative contribution to 2022 GDP with export growth trailing import growth by 2.2%. Meanwhile the freight-intensive construction sector is forecasted to fall 1.3% in 2022, as declines in residential and commercial construction won’t be offset by the 4.4% increase in spending on highway and street construction from the new infrastructure bill.

The outlook for freight

The deterioration in the outlook for 2022 economic growth weakens the outlook for most segments of the U.S. freight market. And embedded in the weaker overall economic growth is a decline in volume demand for durable goods, a key element in truck and rail freight demand. Freight demand will weaken increasingly through 2022 with the progressive shift in consumer spending away from durable goods and back toward services.

There are a few freight segments that have an improved outlook for 2022 due to recent market disruptions, such as for those serving energy and agricultural export-related customers. Those are sectors of the U.S. economy that now see stronger demand for the U.S.-produced goods as direct or indirect substitutes for now-embargoed Russian exports or disrupted exports from Ukraine.

Overall, this new situation is a significant shift from the strong U.S. goods consumption growth that overwhelmed supply chains in 2021. This is not a return to the pre-pandemic 2019 composition of freight. Instead, it reflects a more risk-averse model for much freight in the economy with higher costs from increased operating and inventory carrying costs.

S&P Global Market Intelligence forecasts for the remainder of 2022 show the economy moving past the 2021 peak of trucking and air cargo demand growth, with inflation and shifts to services spending across the economy leading to “demand destruction” for some categories of freight demand. For example, we expect to see e-commerce growth slow and actually reverse in some categories (such as home exercise equipment and food for home delivery). Similarly, carriers serving the construction market will see softening demand as construction companies grapple with higher interest rates and lingering supply chain problems. Export-related freight transportation also faces multiple headwinds. Exporters are struggling to deal with capacity constraints for handling exports via rail and through seaports and a strengthening U.S. dollar, which makes some U.S. exports less price competitive in overseas markets.

As a result of efforts by carriers, intermediaries, and shippers, there is progress in shrinking the structural gap between freight capacity and goods demand. However, with higher fuel costs and higher wages, freight logistics costs for shippers won’t fall back to pre-pandemic levels. The higher transportation costs being passed through to consumers as part of goods price inflation will lead to lower sales volume growth.

The freight outlook varies by modal segment and customer base. For supply chain managers, the forecast outlook implies more opportunities to benefit from spot-rate declines, which may help offset fuel surcharge increases from carriers. Yet potential rate relief will remain limited with carriers facing the higher costs for labor and equipment in addition to fuel price increases. Capacity and operational limits remain in many areas, with congestion lingering at container ports and intermodal rail yards through the first half of 2022.

With slower or declining 2022 sales volume growth, shippers may be able to better manage their volumes. For carriers, the prospect of improved operations, reduced inefficiencies, and reduced service disruptions for the rest of 2022 brings the opportunity to better utilize assets and improve customer satisfaction.

Author’s note: This analysis is from S&P Global Market Intelligence and not S&P Global Ratings, which is a separately managed division of S&P Global. IHS Markit it now part of S&P Global.