The nation’s trucking woes are as challenging as ever. As companies work tirelessly to ship critical goods, they’re wrestling to secure capacity, control costs, and get their products to their destination on time.

Since 2017, we’ve published the quarterly U.S. Bank Freight Payment Index, which is based on data from tens of thousands of paid truck freight invoice transactions between shippers and carriers. For context, in 2021 we processed more than $37 billion in shipper and carrier payments. The Index provides a window into changes in shipping cost and volume on a quarterly basis. Importantly, we break the data down by region, as each region has unique challenges. What follows are key points from our most recent Index and other sources along with ideas for enhanced support to help navigate the industry’s ongoing volatility.

Spending growth

One trend to watch is that the Index shows continued growth in spend by shippers. Spending on truck freight in Q2 increased 3.3% from Q1 2022 and was up 19.7% year-over-year. This increase is due not only to record diesel prices but also to a movement of shipments from the spot market back to the contract market.

Most of the transaction volume that we track is from the contract market, therefore the U.S. Bank indexes are more reflective of contract freight as opposed to the more expensive spot market. Our data indicates that even though contract carriers seemed to have held their prices relatively steady, there’s increased utilization of the contract market.

In the second half of 2020 and through most of 2021, shippers relied heavily on the spot market to manage capacity challenges stemming from driver and equipment shortages. The spot market also helped address the tremendous spike in household goods spending as consumers stayed home and stocked up.

But as spending on travel and services began to increase in 2022 and the economy contracted in Q1, trucking capacity opened up and the freight market shifted back to contract carriers. The slight decrease in demand was offset, however, by the dramatic rise in fuel prices, as well as some strength in manufacturing and housing in various parts of the country. These factors helped push the spend index higher in Q2, in spite of the modest slowdown in the economy during the quarter. From a volume standpoint, the U.S. Bank National Shipments Index increased 2.3% in Q2.

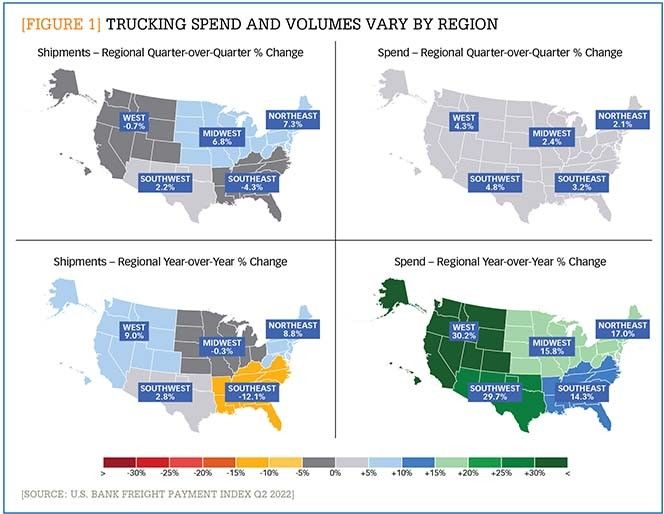

Regional trends and revelations

Interestingly, changes in shipment volumes varied by region. Shipment volumes decreased for two regions—the Southeast and West—in Q2, by 4.3% and 0.7% respectively. Contrast that with the volume gains in the Northeast (7.3%) and the Midwest (6.8%). Compared to the same quarter in 2021, the Southwest recorded a 2.8% volume gain—the fifth straight quarter with a year-over-year increase. (See Figure 1.)

[Figure 1] Trucking spend and volumes vary by region

Enlarge this image

Looking more closely at the Southeast’s considerable decline, this region’s shipments index contracted a little over 12% year-over-year—far outpacing the other five. Reasons leading to this drop could include softer housing starts (a big factor for this region) and slower retail sales in the region. Although tourism-related services may be strong in the Southeast, trucking to support these services generates less volume than the transportation of goods.

Alternatively, the Midwest demonstrated the power of strong manufacturing output, which fueled higher Q2 truck freight levels in this region. Even more pronounced, the Northeast region posted its largest quarterly gain in three years. Housing starts in the region were stronger than the others, and a higher factory output helped boost freight volumes to the nation’s highest level.

Driver and equipment shortages

As noted earlier, over the past two years, the spot market surged as shippers’ contract carriers couldn’t haul the added freight during the pandemic because of capacity and driver constraints. Now, contract freight is outperforming the spot market. However, driver and equipment shortages continue to cause problems.

According to American Trucking Associations (ATA), the driver shortage is at a historic high with no end in sight.1 Over the next decade, more than one million new drivers will be needed to replace those leaving the market and enable growth, the ATA reports.

A range of incentives are being offered to recruit new drivers and retain current ones. In fact, the ATA notes that average annual earnings have increased by five times the previous standard. But some drivers are choosing to work less. Others are reluctant to make trucking their career due to lifestyle challenges—including time away from home—and other barriers to entry, such as failed drug tests, driving record infractions, and criminal histories.

Adding to the turmoil, truck parts (for new and used trucks) are in very short supply due in part to pandemic-forced factory shutdowns and other supply chain issues, such as port congestion, the Ever Given Suez Canal blockage, and weather events. To compensate, fleets are being even more vigilant about maintenance schedules, recognizing that their equipment must do more than ever before, all while maintaining excellent safety standards.

Smart support for tough times

Diesel prices, labor costs and availability, equipment costs and availability, and economic uncertainty—these are tough times for the industry. Smart use of shipping data, analytics, and industry benchmarking, however, can help companies better navigate these volatile times. Insights regarding trends affecting the entire industry—particularly spending and volume levels—can be very useful for logistics planning.

Tools such as our Freight Payment Index can help shippers analyze current freight shipping data at both national and regional levels to make informed decisions based on factors most relevant to their organization. Robust analytics can help supply chain and logistics professionals gain a further edge over their competition by providing reporting and data analysis capabilities that dive deeper into causes and effects and model options to further improve their supply chains.

Finally, benchmarking can help companies analyze utilization and spend to see where they stand compared to their peers. This analysis further enables them to gauge their performance and determine opportunities to adjust and achieve improvements.

Nationwide capacity and supply data are very dynamic. But the more an organization can anticipate issues and discuss them with its stakeholders, the more it can maintain an effective, responsive supply chain—even in the most challenging times.

Note:

1. “Driver Shortage Update 2021,” American Trucking Associations (Oct. 25, 2021): https://www.trucking.org/sites/default/files/2021-10/ATA%20Driver%20Shortage%20Report%202021%20Executive%20Summary.FINAL_.pdf