Our annual inventory check-in shows that inventory levels and costs have been continuing their wild roller coaster ride over the past year as many supply chains seem to be in the throes of “the bullwhip effect.” The bullwhip effect occurs when variations in downstream demand lead to large overcorrections upstream due to delays in information, production, and distribution—all of which make forecasting difficult.

After having too much inventory in 2020, then not nearly enough in 2021, the pendulum has swung back towards abundance in 2022. Large retailers like Target and Walmart are marking down prices and cancelling orders, while smaller retailers are simply trying to stay afloat under the weight of too many goods. This is a far cry from this time last year, when the New York Times was writing articles titled “How the World Ran Out of Everything.” Case in point, total business inventories reached $2.38 trillion in May 2022—up 24% from the nadir in July 2021.1

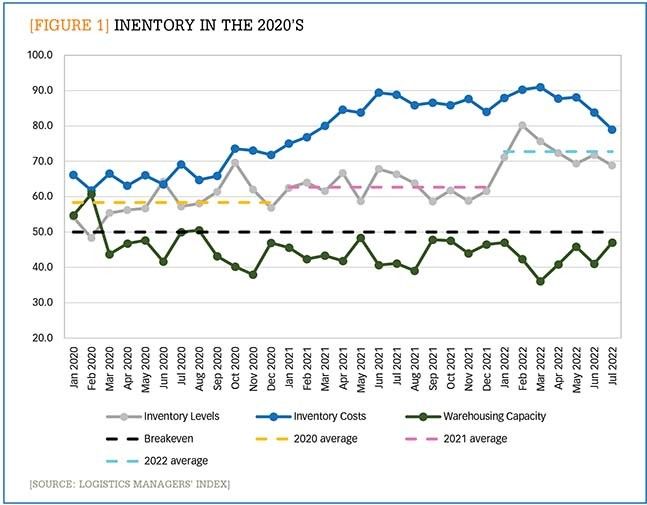

This volatility is reflected in the inventory indices that we calculate each month as part of the Logistics Managers’ Index (LMI). Figure 1 charts the inventory levels (gray line), inventory costs (blue line), and warehousing capacity (green line) metrics from the Logistics Managers’ Index (LMI) from January 2020 to July 2022. A reading above 50.0 (the black dashed line) indicates expansion, whereas anything below 50.0 indicates contraction.

[Figure 1] Inventory in the 2020s

Enlarge this image

Other than a slight contraction in February 2020, inventory levels have been increasing constantly over the past two and a half years. However, the rate of expansion has looked quite different year-to-year. In 2020, the average rate of expansion for inventory levels (orange dashed line) was 58.4; in 2021, the rate of expansion jumped to 62.7 (pink dashed line); and in the first seven months of 2022, it increased significantly to 72.8 (dashed teal line).

In 2020, inventory levels and inventory costs only expanded at a moderate rate, as low consumer demand led to a decline in imports and manufacturing. As lockdowns lifted in 2021, consumer demand increased. While real inventory levels rose, they struggled to keep up with this booming demand. At the same time, the increased demand combined with global supply chain congestion to drive the costs of holding and storing goods to record highs. This is reflected in the steady increase in inventory costs seen in 2021 that were incurred as firms paid dearly while competing against each other to move products towards consumers.

Through the first seven months of 2022, we have seen a statistically significant increase in inventory levels from what we saw in 2020 and 2021. This change came through a series of events. Due to shortages and congestion slowing shipments both between and within countries, firms over-ordered goods throughout much of 2021. While consumer spending was robust for much of Q4, it dropped off unexpectedly in December due in part to the Omicron surge in the Northeast. Additionally, port and inland transportation congestion meant that goods that had been due at Thanksgiving did not show up until President’s Day. Unfortunately for this late-arriving inventory, Q1 of 2022 looked much different than Q4 of 2021, as robust consumer spending was tempered by record inflation, which crippled demand for the nonessential consumer goods that many firms were suddenly flush with.

While inventory metrics fluctuated throughout the pandemic and recovery, the lack of available warehousing capacity (green line) has remained constant. LMI respondents have reported a contraction in capacity for 27 of the last 29 months. Even the approximately 738.6 million square feet of warehouse space added to the U.S. in 2020 and 2021 was not nearly enough to keep up with demand.2 This shortage of warehousing space has slowed the intake of new goods and made holding overstocked goods incredibly expensive.

Where is this headed?

Firms are attempting to deal with this high level of inventory in various ways. Some large retailers like Walmart and Costco—which reported inventory increases in the most recent quarter of 33% and 26% respectively—are discounting unsold goods to make way for the wave of imports that usually arrives during the second half of the year. Sportswear company Under Armour is pursuing another prominent strategy of cancelling orders, rescinding approximately $200 million of shipments. Meanwhile Target is employing both strategies, marking down prices and canceling orders. This aggressive approach did lead to lower inventories, but also to a 90% drop in quarterly earnings year-over-year.

Another strategy involves offloading overstocked goods into secondary inventory channels, such as off-price retailers, dollar stores, and salvage dealers. The size of these secondary markets reached a record high of over $681 billion in 2021—3% of U.S. gross domestic product (GDP).3 However, this strategy will not work for all overstocked goods. Secondary retailers operate on a high-turn strategy in which inventory moves through their systems quickly, and they are not likely to take on a high volume of off-season or soon-to-be-obsolete goods.

When asked to predict logistics activity over the next 12 months, LMI survey respondents predict that inventory levels will continue to increase, but at a significantly slowed rate of 64.8, with inventory costs growth slowing to a rate of 78.5. This slowing growth is at least partially due to the prediction that available warehousing capacity will finally begin to expand again (at a moderate rate of 51.5) over the next year.

Firms have worked diligently to burn off inventories through the first seven months of 2022, but the back-to-school and holiday seasons—and the wave of imports that come with them—will be here soon. The goal for inventory managers through the rest of 2022 will be to carefully wind down inventories, while not overcorrecting once again and ending up in another shortage situation (which is a common occurrence when the bullwhip swings back too quickly).

Threading this needle while production and delivery lead times continue to vary will make this quite the challenge. The aftermath of a global pandemic was always going to be long tailed. Hopefully, we are now closer to the end of that tail than to its beginning.

Author’s note: For more insights like those presented above, see the LMI reports posted the first Tuesday of every month at: www.the-lmi.com.

Notes:

1. U.S. Census Bureau, “Total Business Inventories,” FRED Economic Data, Federal Reserve Bank of St. Louis (June 27, 2022), https://fred.stlouisfed.org/series/BUSINV

2. A. Ortiz, “The U.S. Industrial Sector Sets New Records in 2021,” Knowledge Leader—Colliers Commercial Real Estate Blog (February 3, 2022), https://knowledge-leader.colliers.com/amanda_ortiz/the-u-s-industrial-sector-sets-new-records-in-2021

3. Z.S. Rogers, D.S. Rogers, and H. Chen, “The Importance of Secondary Markets in the Changing Retail Landscape: A Longitudinal Study in the United States and China,” Transportation Journal (2022), 61(1).