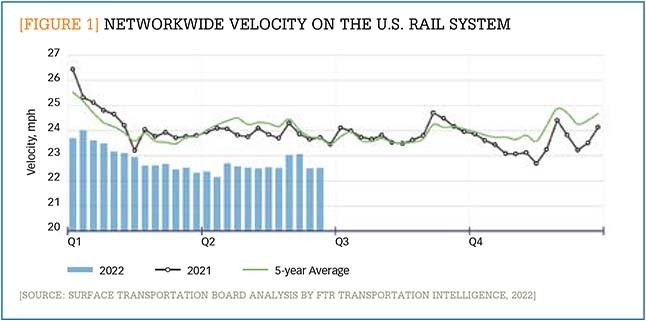

Coming out of the pandemic, the rail industry has experienced persistent service problems that are frustrating shippers and attracting unwanted attention and pressure from regulators. These problems include reduced velocity (see Figure 1) and elevated dwell times at rail terminals, both of which are significantly worse than historical norms. As a result, rail carriers have been losing share to truck and other modes.

[Figure 1] Networkwide velocity on the U.S. rail system

Enlarge this image

Part of the reason for the service issues is that the railroads are having trouble attracting and retaining operating employees. The number of overall operating employees for U.S. Class I carriers has been essentially flat since the fourth quarter of 2020. In addition to the fact that operating employees have not had a raise in the last two years during contract negotiations, the industry has an ongoing lifestyle headwind when it comes to recruiting new employees. New hires are routinely subject to years of being on call and not knowing when they are going to report for work. This leads them to choose alternative industries—such as manufacturing or construction—that have more predictable work schedules and a guarantee of being home every night.

Another factor influencing the current environment is the widespread adoption of Precision Scheduled Railroading (PSR). PSR is an operating philosophy that seeks to lower costs and operate the railroad more efficiently by removing excess assets from the network and working the remaining assets at a higher utilization. But it also leaves little slack in the system if volumes recover quickly, as they did after the COVID-19 pandemic eased and the economy reopened. That volume rebound also came after two rounds of significant furloughs—the first related to PSR implementation and the second related to the pandemic—that led former operating employees to move into other industries.

PSR has also failed to live up to some promises made to shippers. Shippers had been told that once carriers implemented PSR, they would be able to trim their fleets and maintain fewer operating leases. But this “equipment dividend” has not yet manifested. Instead, many shippers are now adding cars to their fleets to compensate for the poor service they have been receiving for well over a year. The added cost of having to purchase more rail cars does not encourage shippers to bring more freight to the railroads.

Historically, rail carriers with mature PSR have been able to pivot to growth once the initial cost-cutting phase was completed. But current service issues have reached a point where they are holding back rail’s ability to grow volume. FTR’s expectations for the carload market now call for less than 1% volume growth in 2022 on a year-over-year basis. This level of volume growth, even with a lean asset base and balance sheet, will make it difficult for the carriers to sustain the type of financial metrics their investors have grown accustomed to.

There are several factors—including an increasing focus on environmental, social, and governance (ESG) goals—that should provide a tailwind to rail carriers looking to grow their volume. However, the industry must first be able to provide consistent service to its customers. As it is, carriers do not have a good track record of attracting additional freight to their lines in spite of various initiatives to grow the carload business over the last 20 years.

Investor concerns

Investors, for their part, are not united on what the best path is for railroads going forward. Comments on earnings calls over the last few quarters highlight that investors are split into two camps.

The first camp determines a railroad’s health and investment quality by looking predominantly at operating ratio (which compares the total operating expense of a company to net sales) to the exclusion of almost all other metrics. This group of investors believes that carriers should not attract or retain any business that has an operating ratio higher than a 60.

The other group of investors is increasingly aware that, without volume growth present, financial metrics cannot and will not be maintained over the decades to come. They believe there is plenty of carload freight that can be moved efficiently and profitably that does not have a sub-60 operating ratio attached to it. The second group of investors is increasingly focused on attracting this freight back to the railroads and learning about what the carriers are doing to protect their franchises for the long term.

This pressure to grow volumes from a significant segment of investors should encourage carriers to rectify their service issues. In addition to helping carriers better satisfy one of their major investor groups and help bring shippers’ freight back to the North American rail system, it could also limit the advance of pro-regulatory forces in Washington, D.C.

Regulatory pressures

The Surface Transportation Board (STB) is currently as active as it has ever been in its 26-year history of regulating rail freight in the U.S., and resolving service issues is its number-one priority.

One of the easiest remedies for regulators to implement in order to alleviate the service issues is to require carriers to report additional data and participate in additional calls with Board staff to discuss what measures they are taking to fix the situation. The Board already took this step, however, in response to the hearing it held in April on freight rail delays and appears less than pleased with the results. STB chairman Martin Oberman said the industry’s first round of service improvement plans were substantially not up to par. This response presents a cautionary tale for carriers and shippers that they should take agency requests seriously.

The other big hammer in the STB toolkit is a directed service order, in which the board tells the carrier how to handle, route, or move freight. Sometimes the order even requires the freight to be moved on another railroad. This requirement has helped to make directed service orders the board’s nuclear weapon when it comes to addressing service issues.

The board is clearly interested in using directed service orders as a remedy. It took steps in May to make it easier for shippers to apply for one. The notice issued by the board, which remains out for comment, stated that the board intends to remove the requirement that a shipper secure a commitment from a competing carrier to move the traffic that would be subject to the potential directed service order. Then in June, the Board issued an emergency service order to Union Pacific related to shipments to an agricultural shipper in California. Other service orders could be coming if shippers continue to see velocity and other service metrics hold well below historical averages.

It does not appear, however, that a directed service order would be appropriate for solving the present service issues. The current service problems are broad-based enough that if any carrier had to move the traffic from another carrier’s lines, it would likely end up putting its own service at risk. In fact, the board does not have a good tool for dealing with situations like the networkwide service disruptions that are plaguing the industry. Instead, the business imperative for the carriers to improve service will have to be the foundation for volume and earnings growth going forward.

However, service issues could give the agency more cover to make larger changes to the regulatory framework between railroads and shippers. The board is looking at several potential economic reforms at the same time as it works to resolve the current service issues. The railroads and their shippers need to hope that the board does not reshape the balance of power between shippers and carriers for decades to come solely in response to present service issues.

If the carriers can quickly restore service over the next few months, it could lead to a lessening of regulatory pressures. Unfortunately, an improvement in service on a networkwide basis appears unlikely. Industry employment figures for train and engine employees have been fairly stable, and some carriers actually reduced train and engine headcount during June, the latest month for which data is available at press time. But it is in everyone’s interest for the service issues that have dominated headlines to resolve soon.

For more information about where the rail industry is headed, go to www.ftrintel.com/supply-chain-quarterly2022 to download more information about FTR’s forecasts for the rail and intermodal markets.