Last year taxed every inch of the U.S. supply chain. Fueled in part by trillions of dollars of COVD-relief money, demand for goods surged in 2021. Global supply chains, however, struggled to keep up as they faced material shortages, a tight labor market, capacity constraints, and a congested transportation network.

This volatility and tumult caused U.S. business logistics costs (USBLC) to skyrocket to $1.85 trillion, a 22.4% increase over 2020, according to the Council of Supply Chain Management Professionals’ (CSCMP’s) 33rd Annual “State of Logistics Report.”

Originally created in 1989 by the late logistic consultant Robert V. Delaney to measure logistics efficiency following the deregulation of transportation in the United States, the “State of Logistics Report” has expanded over the years. It now not only details all the costs associated with moving freight through the U.S. supply chain but also analyzes the overall state of the economy and key logistics trends to watch.

TO LEARN MORE…

This article contains just a small sampling of the insights and analysis found in the “CSCMP’S 33rd Annual State of Logistics Report.” The report can be downloaded for free for CSCMP members at the CSCMP website (cscmp.org) under the “Research” tab. Nonmembers can purchase the report for $249. An executive summary of the report is free to all.

CSCMP members can also access a video of the release presentation that occurred at the National Press Club in Washington D.C. in June here.

Interested in an update to this year’s report? A panel of report contributors and industry leaders will discuss the finding and provide new insights at an educational session at CSCMP’s EDGE conference in Nashville, Tennessee, on September 19. Panelists will include Paul Bingham, from S&P Global Market Intelligence; Jennifer Kobus of Ulta Beauty; Andy Moses of Penske Logistics; Kevin Smith of Sustainable Supply Chain Consulting; John Verdon of Waymo; Rob Walpole of Delta Airlines; and Michael Zimmerman of Kearney.

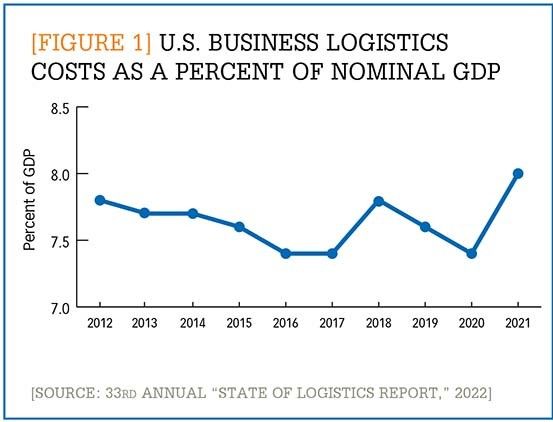

This year’s report—written by the global management consulting firm Kearney for CSCMP and presented by logistics service provider Penske Logistics—bears the descriptive title “Out of Sync.” It relates how 2021 was characterized by severe mismatches between demand and supply of everything—from labor to transportation and warehousing capacity to raw materials and parts. As a result, USBLC ended up representing 8% of the country’s gross domestic product (GDP) of $23 trillion, a level not seen since 2008. (See Figure 1.) Meanwhile supply chain leaders felt intense pressure from internal stakeholders as rates shot up but service deteriorated.

[Figure 1] U.S. business logistics costs as a percent of nominal GDP

Enlarge this image

Everything goes up

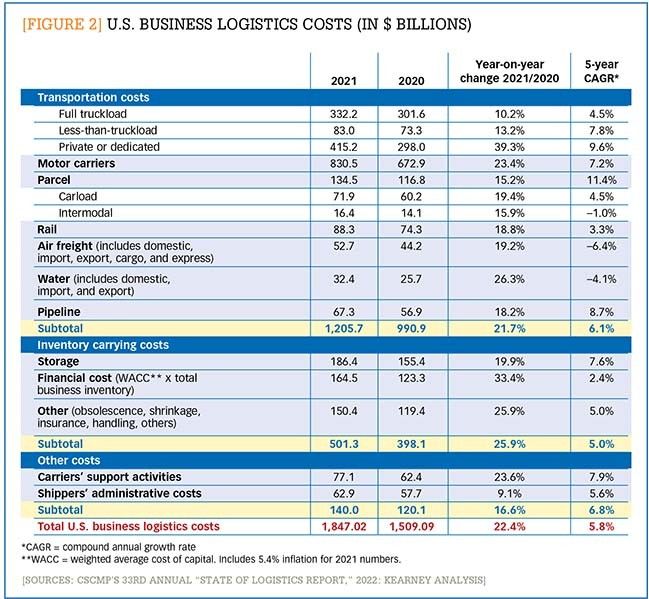

The report carefully breaks down all the factors that make up total business logistics costs, which include transportation costs (all modes plus parcel and pipeline), inventory carrying costs, and “other” costs (including carriers’ support activities and shippers’ administrative costs). (See Figure 2.)

[Figure 2] U.S. business logistics costs (in $ billions)

Enlarge this image

The chart shows total transportation costs increasing by 21.7% in 2021 compared to 2020, with costs rising across all modes, as can be seen in the breakdown below:

- Motor carriers: Trucking, which is the largest segment of U.S. logistics spend, saw its costs rise by 23.4% in 2021 to $831 billion. The increase was driven in part by rising consumer demand and shippers’ attempts to replenish inventory levels. Tight capacity drove many shippers to pay increasingly high spot market rates, which helped push profits for carriers upward. According to the report, top carriers reported seeing profits rise by 50%–100%, (and sometimes even more), even as their own operational costs surged.

- Parcel and last-mile logistics: Parcel volumes rose last year as e-commerce sales continued to grow at a rate of 10% year-over-year. However, existing last-mile delivery systems struggled to match that growth due to tight labor supply and an overburdened infrastructure. As a result, parcel delivery companies, such as UPS and FedEx, raised rates, and costs associated with parcel shipping jumped to $134.5 billion, an increase of 15.2%.

- Rail: While network speeds and service levels dropped due to port congestion, chassis shortages, and a tight labor market, costs rose 18.8% to $88.3 billion. In spite of service problems, rail companies were able to improve revenues, operating ratios, and total operating income last year.

- Air freight: With other modes facing tight capacity and increased congestion, air freight took on an expanded role in the global supply chain last year, according to the report. Volumes increased by 18.7% over 2020. Capacity, however, remained tight. Since demand continued to surpass supply, air freight costs for shippers soared to $52.7 billion, an increase of 19.2%. These increases allowed revenues to hit $175 billion, a record for the industry.

- Water shipping and ports: Of all the transportation costs, U.S. water shipment costs (which do not include international ocean expenditures) saw the biggest increase, shooting up by 26.3% to $32.4 billion. Last year saw trans-Atlantic costs rise by 100% and trans-Pacific costs rise by 200%. It is perhaps not surprising then that, according to the report, ocean carriers earned more in 2021 than in the previous 20 years combined. Yet the industry struggled immensely with service issues as tight capacity and congested ports frustrated shippers to no end.

- Pipeline: Costs for the pipeline sector for 2021 came in at $67.3 billion, an increase of 18.2%. The sector faces headwinds from several directions including increasing environmental regulations, strong public resistance to new projects, more severe weather events, and geopolitical turmoil.

Another significant factor driving the increase in business logistics costs was the rise in inventory carrying costs. Costs jumped 25.9% in 2021 to just over $501 billion. While inventory levels dipped to near historic lows last year, the costs to store, handle, and finance that inventory went up sharply. Warehouse rents, for example, rose by 9.5%, nearly twice as fast as in 2020, and warehouse construction costs rose by 29% between March 2021 and March 2022. At the same time, labor shortages have forced wages for hourly warehouse employees up, with some markets, such as Southern California and Seattle, Washington, seeing pay reach $19 an hour. Meanwhile financial costs were up 33.4%, due primarily to higher interest rates.

Finally, as Figure 2 shows, the calculation for U.S. business logistic costs also includes two other factors: costs associated with carrier support activities and shippers’ administrative costs. According to Kearney, carrier support activities, which rose nearly 24%, include a range of services that support shipping, such as freight forwarders and brokers, customs services, port handling, and packing and crating to name just a few. The report acknowledges the growing role of both freight forwarders and third-party logistics providers as more shippers turn to outside experts to help them navigate the complex and volatile global supply chain. Shippers’ administrative costs, which include labor and logistics information technology, were also up a little over 9% due mostly to rising wages and other labor costs.

Facing hard truths

There’s no doubt that 2021 was a challenging year for supply chain professionals. One that had them longing for relief and a return to some semblance of stability. But while there is certainly the sense that last year’s challenges were unique, the hard truth is that the logistics industry has been seeing significant volatility for a while. In 2018, logisticians were reeling from an 11.4% increase in logistics cost due to tight transportation capacity and rising rates. While costs stabilized in 2019—growing just 0.6%—they dropped by 4% in 2020, the year of the pandemic shutdowns. Indeed, that volatility has continued during the first half of 2022 as logisticians have wrestled with continuing congestion, rising inflation, a slowing economy, periodic COVID shutdowns in China, high fuel costs, and the effects of the war in the Ukraine.

Looking forward, the report’s lead author Balika Sonthalia, a partner at Kearney, anticipates that 2022 will see a softening in demand for logistics services, particularly as many companies have seen their inventory-to-sales ratios increase this year.

Speaking at the June press conference that announced the release of the report, Sonthalia made sure to place this cool-off within a broader context. “It will cool off from the highest increase we saw last year,” she pointed out. “So, the baseline has shifted. There is a cool-off coming, but it is not going to be significant across all modes and nodes.”

Sonthalia believes capacity will remain tight, as the semiconductor shortage, high steel prices, and continuing labor market tightness will continue to make it difficult to deploy more transportation equipment or increase warehouse space. The report states: “In short, the logistics sector must simultaneously contend with the hangover of red-hot demand and worries of a revenue-diminishing and inventory-swelling downturn.”

These disruptions indicate a greater need to focus on supply chain resiliency and agility and have encouraged companies to reassess their supply chain strategies and experiment with different approaches, both large and small. Many companies, for example, are increasingly turning to private and dedicated fleets for over-the-road shipping, while others have increased their use of air freight or are holding more inventory on hand. Other trends include an increase in merger and acquisition activity among transportation providers; greater interest in “multi-shoring” (or sourcing from more than one geographical location); and more investment in technologies that improve supply chain visibility, such as control towers, artificial intelligence, the industrial internet of things, and blockchain. Meanwhile, both shippers and carriers are having to make significant investments to make their supply chains more environmentally sustainable.

One trend that the report repeatedly points to is a move toward greater reshoring or near-shoring. Supply chain disruptions and soaring overseas shipping costs are driving an overall shift toward producing and storing goods closer to the consumer. Nearshoring and reshoring will also protect shippers somewhat from growing geopolitical divides, such as the war in the Ukraine and growing tensions between the U.S. and China. To support this forecasted shift away from the current East-West flow of goods and toward more North-South flows among countries in North America, the United States will need to invest in new transportation infrastructure and assets.

“What is notable for 2021 is that the logistics sector has begun to enable changes that should benefit manufacturers, retailers, and consumers alike,” said Sonthalia. “To meet the increasingly diverse needs of a changing world, while safeguarding the environment and navigating repeated shocks, logisticians must engage in fresh thinking and exhibit unprecedented agility.”

RESPONSE TO THE REPORT

When this year’s “State of Logistics Report” was released in late June, CSCMP gathered a panel of experts to respond to the findings. Below are some reflections from those panelists about the report and their experiences of the past year. (CSCMP members can view the entire presentation here.)

Ron Marotta, Yusen Logistics, vice president

“I think the surprising and grateful aspect of this [year] is we have greater awareness as a society of the importance of the supply chain, and with that we can go forward and enhance, improve, and add to the quality of life.”

Robert Walpole, Delta Airlines, vice president of Delta Cargo

“There’s been a structural change in how people buy things that will drive changes in how we set up supply chains going forward. … In a pre-COVID environment, the air-to-ocean price ratios for Asia to U.S. trade were eight to ten times higher. During COVID, that closed to two to three. That drives a fundamentally different decision for [original equipment manufacturers] about how they choose to freight product.”

Jennifer Kobus, Ulta Beauty, vice president of transportation and logistics

“What I have been surprised about is the accelerated need for agility throughout the last few years. I think that’s going to continue to be critical for organizations. … The other aspect that has been ‘doubled clicked’ for me over the last few years is the importance of technology. Even from a business continuity perspective, it’s become important to understand where your freight is at any moment in time.”

John Verdon, Waymo, trucking lead for business development and partnerships

“What we are beginning to see now is this focus on consistent innovation and how do you apply technology over a number of years to actually make [supply chain operations] far more fluid and end-to-end. [In terms of autonomous trucks,] there is a call out in the report that it’s not a case of if, it’s a case of when. I think that’s very true.”

Andy Moses, Penske, senior vice president of sales and solutions

“When I looked at the report, I was somewhat stunned that when you look at the numbers… private and dedicated [trucking] fleets were up 39%. So, the majority of the additional freight [that we saw last year] ended up moving into this mode. Why is that? I think supply chain design is a big deal. … There are ways to design your network so that your freight moves in ways that are more friendly to your people than a network that may require drivers to be out overnight. I think these are some of the reasons that we saw the surge in private and dedicated fleets.”

Paul Bingham, S&P Global Market Intelligence, director of supply chain transportation economics consulting

“There was clearly a contrast between the report’s summary of the financial performance of the rail industry [and its service performance]. [The Class I railroads have] increased their revenues, improved their operating income, and lowered their operating ratio. By those metrics, you would say that the rail system did very well in 2021. However, the business logistic costs for the rail industry went up 18.8% and performance actually fell—average train spends and dwell time in terminals all deteriorated.”