When the COVID-19 pandemic struck, producers of consumer products were scrambling to keep up with demand. One supply chain executive told us that according to internal projections, his company could have sold 400% more personal hygiene products over the first six months of the pandemic. But years of cost cutting had eliminated any slack capacity and alienated suppliers. Those sales—and the customers behind them—went instead to more agile competitors that had invested in flexible equipment and built long-term relationships with key supply chain partners. His experience is not unique. Many companies have struggled to keep up with recent market shifts. But despite the missed opportunities and frequent disruptions, very few have taken a structured approach to investing in supply chain agility.

Supply chain agility reflects how quickly a company can adjust operations to avoid disruptions while capitalizing on opportunities. In other words, agility enables companies to thrive in uncertain environments. To enhance agility, companies need a structured approach for identifying and funding projects that build internal capabilities and external relationships. Concretely, this means making targeted investments that improve areas such as decision-making, process cycle times, and capacity optimization. Ultimately, the goal is to provide managers the flexibility to respond to a wide range of possible outcomes.

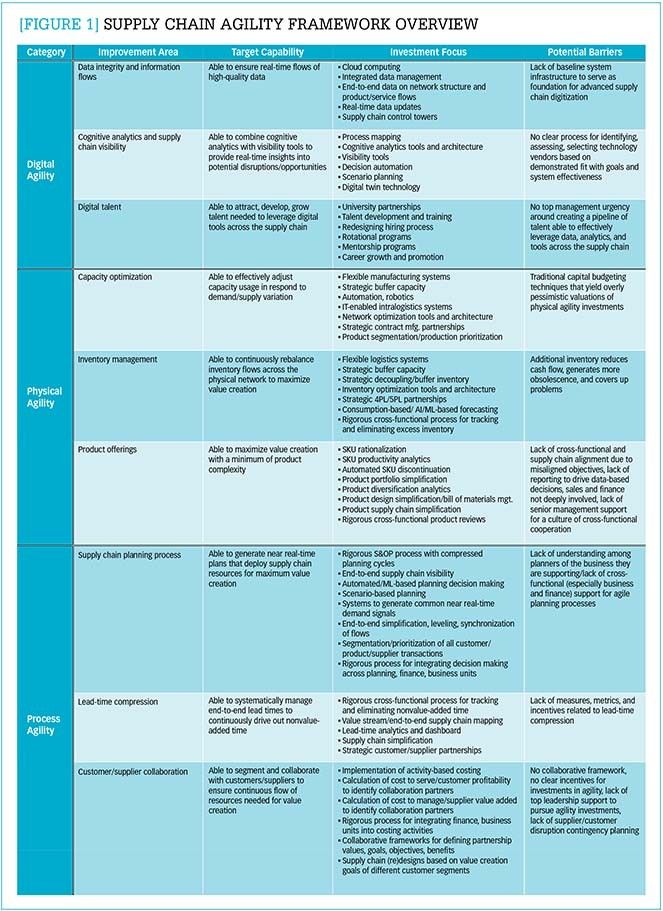

But where to begin? Few companies have a process in place, and available agility frameworks provide limited guidance. The lack of practical advice on how companies should be thinking about agility investments is what prompted our research (see “About this research” sidebar). Based on discussions with dozens of supply chain leaders, we have developed a framework that breaks agility in to three broad categories: digital, physical, and process.

Broadly speaking, digital agility refers to a company’s ability to leverage information flows to improve and speed decisions. Digital agility is reflected in, for example, a company’s ability to ensure real-time flows of high-quality data, generate insights into potential disruptions and opportunities, and develop the talent needed to leverage digital tools across the supply chain.

Physical agility refers to a company’s ability to continuously (re)align physical assets to maximize value creation. Physical agility is reflected in, for example, a company’s ability to adjust capacity usage (for example, production capacity, logistics capacity, and warehouse capacity) in response to demand/supply variation, rebalance inventory flows across the physical network, and generate high levels of customer value with a minimum of product complexity.

Finally, process agility refers to a company’s implementation of processes that support operational adjustments. Process agility is reflected in, for example, a company’s ability to do near real-time supply chain planning, manage end-to-end lead times, and collaborate with customers/suppliers to ensure a continuous flow of resources.

Figure 1 provides an overview of the framework. For each category, companies can identify improvement areas, target capabilities, investment focus, and potential barriers. Using this framework, companies can assess current agility gaps and then hone in on specific projects to improve performance. It’s important to note that while Figure 1 highlights some of the most critical improvement areas we found based on our conversations, specifics will vary across companies. Supply chain agility is not an off-the-shelf application. Rather it’s a complex set of interconnected capabilities. The point here is to provide a framework for structuring ongoing agility improvements.

Supply chain agility framework overview

Enlarge this image

The following sections dive more deeply into each of the agility categories. We provide examples of successful supply chain agility initiatives with practical advice on implementation. In addition, we highlight some of the barriers that companies face in developing agility in each category and make some suggestions for moving forward.

Digital agility

When the pandemic hit, companies that championed digital technologies were in a much better position to see and anticipate demand changes at a granular level. IBM is a good example. Through investments in geo-mapping, IBM has generated visibility into supply, production, fulfillment, and deliveries across its global network. The technology enables managers to see when a multitier supplier can’t ship materials and quickly assess the impact. During the pandemic, IBM reaped the benefits of these agility investments. Armed with advanced visibility, managers could quickly find workarounds as competitors scrambled to simply understand where their supply chains were breaking down. Ultimately IBM was able to meet most of its customer demand despite disruptions at various points in their network.

More broadly, companies seeking to enhance digital agility can begin by focusing on several related capabilities. First, companies need to be able to collect, validate, store, and distribute high-quality data that reflects the current state of the supply chain from their suppliers’ suppliers to end users. This might entail investments in integrated data management through cloud computing and the establishment of supply chain control towers. Companies then need to be able to leverage this data to provide real-time insights into potential disruptions and opportunities. Leading organizations we spoke with particularly stressed the need for cognitive analytics and visibility tools to gain actionable insights. Given the volume and variety of data flows, cognitive analytics can be used to quickly structure data and present relevant information to decision makers.

To develop these capabilities, however, companies must overcome barriers related to hiring, training, and growing supply chain talent. The skills necessary to manage a digitally agile supply chain are diverse, as personnel must be able to effectively leverage digital technologies to manage their area of responsibility (for example, new product development, supplier evaluation, supply and demand forecasting, production and operations, network analysis, logistics, and customer service). This means companies need to think differently about skills and abilities when hiring for these areas, as well as put into place programs for ongoing development and growth. Ultimately, digital agility doesn’t fix a problem, but it does warn companies that a problem exists and provides insights for adjusting supply chains. Talent is needed to understand and act on these insights.

Physical agility

Capital investments in physical capacity are probably where most people start when thinking about supply chain agility. But our conversations with supply chain executives suggest that physical agility is as much about what companies do—and don’t do—with their existing physical assets. Consider stock-keeping unit (SKU) rationalization. The pandemic forced many companies to cut SKUs, and the benefits were felt throughout the supply chain. Several companies we talked to were able to reduce SKUs while improving revenues and increasing margins. But as pressures eased, SKUs have begun to grow again. One executive summed up the sentiments of many supply chain leaders when he said, “You would think it would be hard to walk away from these savings.”

But the impact of SKUs goes well beyond just savings. As product and service offerings proliferate, each individual SKU’s total percent of sales shrinks, while the ability to predict its demand lessens considerably. At the same time, additional SKUs require planning across the supply chain, including for raw materials, manufacturing/conversion, transportation, warehousing, safety stock, and packaging. Planning around nonproductive SKUs locks in capacity, preventing the flexible redeployment of that capacity toward more value-added purposes. Ultimately, maintaining too many SKUs adds complexity while reducing available resources, preventing an agile response to changes in supply and demand.

Benchmark companies we spoke with focus on maintaining the SKUs needed to grow the business—and no more. Costco Wholesale, for instance, averages 3,700 SKUs, where competitors can hold up to 80,000. Costco’s limited focus has allowed it to weather recent demand shifts better than peers. By dedicating resources to its most productive SKUs, Costco was able to grow earnings over the pandemic while competitors struggled. Some companies we spoke with have created a disciplined process for tracking SKU productivity and highlighting key metrics through regular reviews with top leadership. A few firms even have automated SKU discontinuation processes. SKU rationalization (and related product simplification) can then be supported by targeted investments in decoupling/buffer inventory, flexible manufacturing, and automation across the end-to-end supply chain. Such investments enable companies to quickly adjust production while maintaining customer service levels. Agile firms invest selectively to address the greatest risks as part of an ongoing review process, with an eye toward maximizing options as markets evolve. The key takeaway is that companies can achieve significant agility gains by simply rationalizing and then supporting existing physical assets.

Unfortunately, when it comes to investing in physical agility, traditional capital budgeting techniques—such as those based on payback period, internal rate of return, or net present value—can create significant barriers. Such techniques tend to yield overly pessimistic valuations of physical agility investments insofar as they translate high levels of uncertainty into more aggressive discount rates, while downplaying the range of possible outcomes. The whole point of agility investments, however, is to enable companies to respond in a highly uncertain environment. Thus, the uncertainty that makes these investments look unattractive from the perspective of traditional budgeting techniques is precisely what makes them valuable for enhancing agility. By contrast, alternative budgeting methods incorporate the idea that payoffs fall along a distribution and are influenced by managerial actions and environmental conditions. Real options analysis, for example, considers the value of investments that give managers the ability, but not the obligation, to undertake actions in the future. Such alternative methods can augment traditional techniques to generate a more balanced view of agility investments.

Process agility

Core business processes need to support agile operations. Supply chain planning is perhaps the most obvious process that can be used to support agility. A supply chain planning process that provides a common demand signal—in near real time—to all elements of the end-to-end supply chain would obviously facilitate a more responsive network. Likewise, a planning process that was synched to actual customer requirements rather than internal metrics would be better able to adjust when those requirements changed. While many companies talked about the planning process as a critical support for agility, we want to spend our time here on the less frequently highlighted, but no less important, process of managing lead times.

In some ways, lead time is almost synonymous with agility: the faster a network can respond, the more agile that network. A company we spoke with illustrated the point. Prior to the pandemic, the company had undergone an intensive lead-time reduction initiative. Starting with a comprehensive value stream map, the company documented every step in the process from order receipt to delivery for one of its major customers. The company then broke the map down into three target areas for lead-time reduction: planning time, production time, and order fulfillment time. Starting with planning time, the company overhauled its sales and operations planning (S&OP) process to generate more consistent decisions through greater cross-functional alignment. Next the company worked with over 100 suppliers to reengineer their ordering process while enhancing visibility across their network. Finally, the company added automation to reduce pick, pack, and deliver times. The result was to shrink overall lead time from 71 days to 19 days. Along the way, the company created a rigorous process for continuously reviewing lead times and driving out nonvalue-added time. When the pandemic struck, the company was able to leverage its more agile supply chain to win new business by quickly responding to customer needs.

In our experience, though, lead-time reduction remains perhaps the most underutilized process for improving agility. Managers we’ve spoken to point to a lack of incentives around lead-time management. To overcome this barrier, companies can quantify the gains of lead-time reduction in customer service, market share, and cost structure. Benchmark companies not only measure lead times but also set goals for continuous improvement. A major retailer we spoke with manages lead time at every link in the supply chain, including new product introduction, supplier response, production, order fulfillment, and shipping. Another manager told us their manufacturing operations were incentivized to reduce time for schedule changes using a “units produced but not planned” metric. Yet another company uses a “lost sales due to response time” metric across its organization. Whatever the approach, lead-time management is a critical process for supporting agile operations.

Turn disruption into opportunity

Given the increased attention on supply chain, managers today are uniquely positioned to make the case for enhancing agility throughout their network. As managers have these conversations, they should keep in mind a few critical points.

First, supply chain agility is fundamentally about responding to a dynamic environment. Discussions on agility therefore should be less about accurately predicting a particular risk event and more about building agile capabilities.

Second, investments in agility should be seen as investments—not just expenses—and investing is about risk. Most companies view risk as a negative, focusing on mitigating events that could disrupt current operating models. But from an agility perspective, risk simply means change in the environment. And change is inevitable. When talking about agility, the central questions are how open should your company’s supply chain be to change? And what is the appropriate cost for creating such a “change-welcoming” system? These are strategic questions, related to the overarching goals of a company.

Finally, to become truly agile, companies need to bake questions around risk and agility into their regular strategic planning process. Supply chain leaders can support strategy discussions by analyzing emergent trends and proposing digital, physical, and process investments that would position their company to take advantage of change. With a structured approach to improving supply chain agility, companies can turn potential disruption into the next big opportunity.

ABOUT THIS RESEARCH

As part of this research, we interviewed dozens of senior supply chain executives across numerous industries, from consumer packaged goods (CPG), food, apparel, and consumer durables to original equipment manufacturing, automotive supplies, chemicals, and supply chain consulting. Interviews lasted 60 minutes and focused on core capabilities and significant barriers related to supply chain agility. The framework presented in this article was developed out of these interviews and vetted with a core group of participating executives. The research was conducted through the University of Tennessee's Advanced Supply Chain Collaborative (ASCC). ASCC works as a collaborative think tank, bringing together industry leaders and faculty experts to explore advanced concepts in supply chain management. The project was conducted over two years (2020–2022). Additional information about ASCC and the full white paper this article is based on can be found here: https://supplychainmanagement.utk.edu/research/advanced-supply-chain-collaborative/.