The U.S. economy in 2023 will start with weak demand met with mostly adequate inventories. Shippers can expect sufficient freight capacity and lower rates as well as improved distribution center and warehousing availability. While service providers have been adding capacity since late 2020, the situation will be as much a result of changes in demand as it will be due to increases in supply.

A combination of factors will lead to reduced demand in 2023 as the economy falls into a recession. These factors include inflation, consumer and business spending, inventories, and a U.S. Federal Reserve Board monetary policy focused on taming inflation. There are other factors also contributing to the baseline forecast of weakness in the economy and freight demand as we begin 2023.

Mild recession in 2023

The S&P Global Market Intelligence 2023 U.S. macroeconomic baseline forecast is now indicating a recession in the first two quarters with a recovery in growth in real gross domestic product (GDP) in the second half of the year. The resilience of the economy in the fourth quarter of 2022, with sustained employment and moderation in some energy prices, delayed the U.S. economy from falling into recession even as trading partner countries such as those in Europe were already in recession.

For the U.S., on an annual basis, GDP is projected to expand 0.3% from 2022 to 2023 but with the growth coming in the second half of the year after contraction in the first half. The pattern of quarterly U.S. GDP growth in 2022 was also for contraction in the first two quarters followed by growth in the third and fourth quarters. In 2023, the contraction in the first two quarters is forecasted to be greater than during 2022, and the recovery will not be as strong as second half growth was in 2022. The resilient spending of consumers in 2022 relied unsustainably on credit and drawn-down savings instead of stimulus payments as in 2021. Consumer spending is facing more headwinds as variable interest rates and interest rates on new credit continue to increase and inflation remains relatively high.

The recession forecast depends on an assumption that the U.S. Federal Reserve Board is going to maintain interest rate policy to slow demand enough to bring inflation down to its 2% target. The tightening of financial conditions takes time to work through the economy enough to reduce widespread inflation. Consequently, S&P Global Market Intelligence is forecasting that the Federal Reserve will further tighten monetary policy in the first half of 2023, keeping the economy in a period of soft demand.

Interest rate increases are reducing consumer demand by raising the cost of credit. For durable goods purchases, such as autos financed with loans or homes financed with mortgages, lender limits on consumers’ debt service-to-income ratios constrain the number of purchases that consumers can qualify for compared to a year ago. The rapid pace of mortgage rate increases in 2022 already led to a sharp downturn in single-family residential real estate markets, accompanied subsequently by a weakening in the associated furniture and home furnishings markets.

Interest rate increases also affect business, where higher costs of capital reduce firms’ capacities to afford new plant and equipment or even hold substantial safety-stock inventory. For some businesses already facing higher costs from inflation, increased capital costs can result in negative cash flow or even insolvency. Some new-entrant truckers who paid high prices for new equipment in the 2021 boom are particularly vulnerable in this higher-interest rate, lower-growth environment.

International trade to weaken

International trade is forecasted to slow in 2023 with the value of U.S. imported goods declining 1.2% for the year (compared with the 16.4% increase estimated for all of 2022 and the jump of 23.4% seen in 2021). The U.S. will still run a trade deficit, but it will shrink, as exports will not slow as much as imports. The 2023 pace of goods exported is forecasted to grow 1.4%, compared with the 19.1% growth estimated for 2022.

The economies of most U.S. trade partner countries, especially in the more advanced countries, will be in recession in 2023, which typically would weaken demand for U.S. exports overall. However, U.S. energy and agriculture exporters will continue to find good opportunities in global commodity markets disrupted by the Russian invasion of Ukraine. Despite the overall weakness in global trade demand, competitive U.S. exporters will help moderate weaker domestic demand. U.S. trade partner economic growth, measured as trade-weighted foreign GDP, is forecasted to slow from 3.1% in 2022 to 1.2% in 2023. S&P Global Market Intelligence generally characterizes world growth below 2% as a recession, as it is well below potential GDP growth.

The foreign central banks are also following the U.S. Federal Reserve Board in using monetary policy to fight inflation. Also affecting U.S. goods trade in 2023 is the lingering effects of COVID-fighting policies in some countries, especially mainland China, where relaxation of restrictive policies has only recently allowed supply chain disruptions to ease. Downside risks to the global forecasts remain, as new COVID-variant waves and the impacts from the war in Ukraine continue in 2023.

Weak U.S. freight outlook

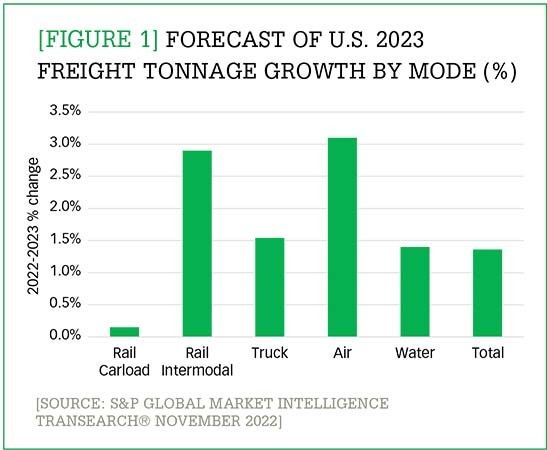

Based on the projected demand for goods and inventory levels in our recession-and-recovery baseline forecast, we expect 2023 U.S. freight volumes to start weak and end the year stronger. The duration of the painful downturn is projected to be limited, where consumption and inventory rebuilding in the second half of 2023 will lead to demand and freight growth for the year as a whole. The S&P Global Transearch baseline forecast overall is for freight tonnage to increase 1.36% for 2023.

Not all freight modes have the same prospects, however. For rail, the range of 2023 tonnage growth is from a small 0.15% increase for rail carload tonnage up to a rebound of 2.9% for intermodal rail tonnage. The intermodal rail recovery is in comparison to 2022 when systemwide congestion and threats of a strike drove customers away. The baseline trucking demand forecast is for recovery by year-end, resulting in 2023 tonnage growth of 1.54%. Air cargo tonnage growth is forecasted slower than in recent years at 3.0% due to slowing e-commerce growth. The maritime baseline forecast includes the assumed recovery of water levels in the Mississippi River System, enabling a rebound of 1.4% in tons compared to suppressed 2022 levels. These Transearch modal freight tonnage forecasts for 2023 are summarized in Figure 1.

Forecast of U.S. 2023 freight tonnage growth by mode (%)

Enlarge this image

For supply chain managers, the baseline freight forecast implies a return towards having market power. Expect softening freight rates, tempered by continuing elevated wage levels and high diesel prices, which will both raise the floor on operating costs. However, after almost three years of running at capacity and operational limits, freight markets will see constraints ease in 2023, especially in the first half of the year.

It is important to note that there does remain significant risks to these baseline forecasts, including potential impacts from policy decisions and/or new shocks, whether related to COVID or other 2023 market disruptions.