Writing about trends in the railroad business is always an interesting exercise. That's because the railroad business is a mature industry, and as such, it doesn't change radically year-to-year. But the world in which mature industries operate and the circumstances surrounding the customers they serve can shift considerably. Any trends that affect customers, of course, will have a significant impact on service providers. As we'll see later in this article, some trends on the customer side that are presently under way or are looming on the horizon could change how shippers work with railroads.

The seismic shift in railroading traces back to the Staggers Act, which deregulated railroads in 1980 and set in motion changes that rejuvenated an industry many had thought was headed for the scrap heap. Virtually all of the railroads in the Northeast were bankrupt, with little prospect for recovery. The strongest carriers, meanwhile, simply did not earn enough to reinvest at a rate sufficient to renew and sustain their infrastructure and asset base. Even the freight rates—much higher in real dollars than today—could not overcome the giant millstone of regulatory constraints and institutionalized inefficiency. The Staggers Act took the shackles off the railroad industry, and the results have been truly transformational.

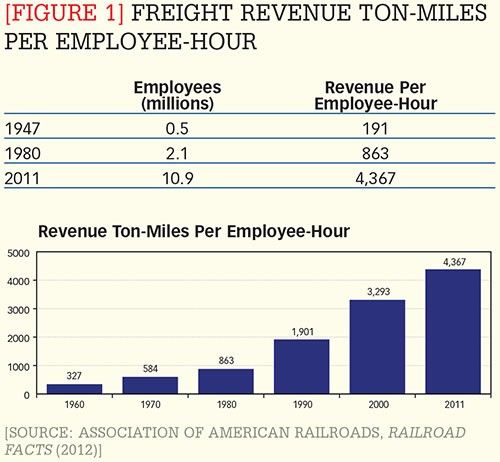

In their current incarnation, the North American railroads haul more freight, at lower cost and with fewer employees, by a factor of about twenty, when compared to 1947, their highest-volume year prior to deregulation. (See Figure 1.)

This was a transformational change, the likes of which have rarely, if ever, been seen before, and it's still going on. The point is that prosperity often brings a following sea of complacency ("We must be smart; look how well we're doing!"), but that hasn't happened in this instance. Railroads have so far largely avoided being in the position of recognizing their mistakes as they're repeating them.

The good news is that, since the onset of the recession, the national rail network has been fluid, with ample capacity and reliable service. The longer-term challenge will be managing the impact a sustained and meaningful increase in volume will have. Rail carriers' continued investment in network upgrades and capacity expansion will certainly help, but current forecasts say it won't be enough.

Managing for the future

What does all this mean for rail shippers? In the context of moving tomorrow's freight, probably not a lot. The strategic implications are more critical. And indeed, there are a number of strategic elements of managing for the future that deserve consideration, exploration, and in many cases, action. Here are two I believe are particularly important.

1. Transportation network optimization. Despite rapid advances in both Internet capabilities for instant communications and sophisticated optimization technology, most companies around the world fail to take advantage of those tools, continuing to buy and sell transportation in what might be characterized as a "suboptimal" fashion. In the vast majority of cases, then, acquiring transportation capacity is essentially a tactical exercise in rate shopping. It is frequently balkanized by geography (continent, region, country, or even smaller areas). It is also often cut up into discrete modes (air, ocean, rail, truck, parcel).

This approach is at odds with the nature of supply chains, which operate as interconnected networks linking suppliers, manufacturers (or other buyers), distributors, and end users. Transportation is a key part of these networks and, in fact, is its own network of freight flows.

Most consumers of transportation services (shippers, consignees, third parties, intermediaries) have a good operational understanding of how their supply chains function. What is so often lacking is a comprehensive view of their network of freight flows (inbound, outbound, and inter-facility). This precludes a strategic view of the entire network based on empirical data, which would enable a different strategy for holistic optimization across what can be a complex global supply chain. Mastering this fundamental capability is critical to truly optimizing a supply chain network.

Operating such networks in an agile and dynamic fashion is vital to optimizing supply chain performance. Many shippers still rely on static routings (that is, if it's an air shipment, it's always air; if it's truck, it's always truck, and so forth). Dynamic operations allow for concepts such as "blended service," whereby tiered capabilities are provided on a lane. The base volume may move by rail (carload or intermodal), replenishment volume may move by truck, and "hot" shipments may move by truck with around-the-clock driver teams, or even by air. This amplifies flexibility and produces a "best cost/best service" model.

2. Supply chain visibility and event management. The other key element is having true visibility across the network. In the past, this has been nobly advanced, yet largely doomed to failure and frustration. The main obstacle has been getting trading partner connectivity to a level that produces meaningful and reliable results. Historically this has hinged on a "one-to-many" set of relationships, where one buyer of services has endeavored to connect with hundreds or even thousands of trading partners across the supply chain. Few can claim success. Generally, these efforts have failed because of the time and expense involved in the gritty work of building connections to each party and then maintaining them. Failure to capture each one leads to holes in the supply chain. That makes the data suspect and unreliable, which ultimately leads to the inability to rely on the results. That has now changed.

Two developments became the game-changers. First, device-independent, cloud-based technologies have blossomed as the Internet, growing at breakneck speed, has driven and enabled innovation. And second, the cloud-based, multitenant platform we now have speeds up and simplifies those things that caused earlier attempts to stumble and fail. Think of it as a kind of "Facebook for logistics." It is a community of logistics service providers and users. Instead of connecting individually with each of my trading partners—be they an ocean carrier, airline, railroad, motor carrier, or third-party logistics service provider—I "friend" them on the platform. The advantages to the service provider are significant: Instead of maintaining connections to every one of their customers individually, they need only connect once. When it comes to updating information (for example, schedules, contact information, news and notices, public tariffs, procedures, and so forth), providers can post and maintain it for all of their customers in a single instance.

Coupling a truly optimized network with comprehensive visibility—right down to the stock-keeping unit (SKU) level—will take us to the next generation of supply chain performance. Viewing this in the context of the rail industry, it means that as a shipper, I can now conduct true multimodal analysis and comparison of service and price trade-offs. In the past, I might have gone out to the market periodically to solicit competitive rates. But without the ability to accurately compare cost, service, and capacity trade-offs simultaneously across all modes, I could well be missing opportunities to improve performance and take out cost.

At the beginning of the 1970s television show "The Six-Million Dollar Man," about a test pilot who gained superhuman abilities through bionics, a voiceover announcer said, "We have the technology..." Well, folks, we have the technology to transform supply chains, taking them from a tool for tactical execution to a means of strategic enablement. The railroads will play a key part in achieving this important goal. It's time for shippers to integrate them more seamlessly into the overall network strategy of their organizations.