In our annual outlook, we identified 2023 as being a year of two halves. The first half of the year is expected to see a return to “normal” supply chain conditions, particularly in terms of physical network operations. The second half, however, may bring confirmation of changing corporate sourcing strategies in the wake of the pandemic and political tensions.

Disruptions coming to an end

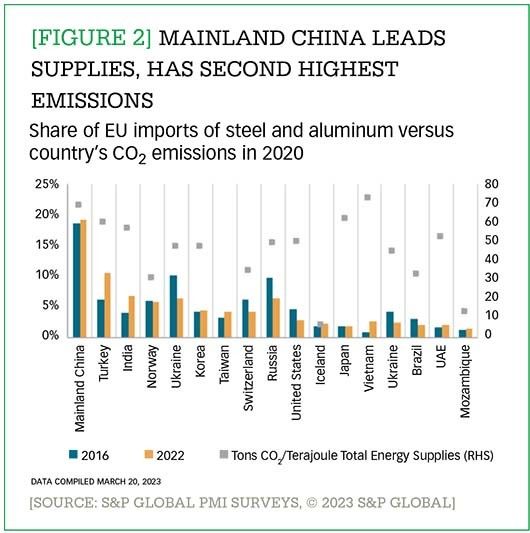

Evidence from the first quarter of the year suggests the normalization in logistics networks has rapidly arrived. For example, as part of our Purchasing Managers’ Index (PMI), S&P Global Market Intelligence asks survey respondents, “Are your suppliers' delivery times slower, faster, or unchanged on average than one month ago?” Based on their responses we calculate a supplier delivery times index, which is used to indicate the extent of supply delays and capacity constraints in the general economy. For the index, which is shown in Figure 1, readings of 50 mean that there has been no change in delivery times over the prior month, readings above 50 indicate that delivery times were shorter or faster than the previous month, and readings below 50 indicate that delivery times were longer or slower. As Figure 1 shows, the most recent PMI indicates that after several years of slow supplier delivery times, times in the U.S. and European Union have reached their fastest on record. This suggests that after years of supply constraints and delivery delays, supply is loosening up and the transportation network is less constrained.

[FIGURE 1] Supplier delivery times their fastest on record in U.S., Eurozone

Enlarge this image

Part of the normalization process is due to there being less pressure on logistics networks. Our forecasts indicate global trade, on a real (that is, inflation-adjusted) basis, has dipped by 0.1% in first quarter 2023, compared with a year earlier. We estimate that it will expand by 0.4% in the second quarter of 2023 and accelerate to 2.5% in the fourth quarter of 2023. With the easing in demand, we are seeing less congestion and capacity constraints across supply chain networks.

There is also evidence that we may see a return to traditional seasonal shipping patterns in 2023. The elevated level of U.S.-inbound container shipments during the consumer boom that occurred from late 2020 to mid-2022 meant there was little seasonality in shipping as ports struggled to “dig out.” In 2022, peak season occurred much earlier than normal as firms sought to avoid shortages. For 2023, there is an apparent return to normal shipping levels and off-peak patterns. But whether or not we are seeing a full return to historic buying and shipping patterns for U.S. and European importers wouldn’t be clear until late summer.

Shipping conditions may be returning to normal levels, but that does not mean all sectors are back to regular operations. The electronics sector faces a glut of supply in memory chips and processors for smartphones and PCs, while the automotive and industrial sectors are still working through back orders as supplies normalize.

Rethinking corporate sourcing strategies

The shortages of the pandemic era may be quickly becoming a distant memory, with some sectors already back to pre-pandemic levels. But corporate inventories are by no means back to normal across the board. U.S. retail sales, for example, are still below their historic averages, but that's due mostly to the automotive sector. Consumer durables (furniture and appliances) and general stores have actually declined from recent peaks, as firms seek to make up for earlier overpurchasing.

The road ahead for inventories will depend on whether firms switch to “just in case” rather than “just in time” sourcing strategies. A more prudent just-in-case approach to inventories reduces future risk. However, a recession with tighter financial conditions may mean banks and shareholders will not allow firms to lock up more cash in inventories.

Aside from the question of “how much” to source, companies have also had to address the question of “where from.” Disruptions from the pandemic have led companies to rethink their over-reliance on sourcing from China. Reshoring, however, is an expensive process. So, like changes to inventory strategies, we're unlikely to see firms making major adjustments in where they source from during the high-interest/falling-profit environment of 2023.

Our analysis of the telecommunications and computing sectors, for example, shows that reshoring is a multiyear process with a panoply of drivers ranging from labor costs and transit times to tariffs and local industrial policy. The exceptions may be the automotive and semiconductor sectors, where significant government funding is encouraging firms to accelerate their investments in new countries including the U.S., the EU, South Korea, Japan, and mainland China.

Conflict, chips, and carbon

With supply and logistics constraints looking to mostly ease in 2023, government policy changes remain one of the largest risks facing companies for the remainder of 2023 (although certainly not the only risk). Policy shifts addressing the war in Ukraine, restrictions on semiconductor exports, and sustainability measures could all have an impact on how companies structure their supply chains.

The war in Ukraine is still ongoing, with fighting likely to continue over the next six months and an eventual stalemate likely by end 2023. From a supply chain perspective, the main outstanding risk comes from an extension of sanctions, including secondary sanctions for countries that sell to Russia.

The passage of the CHIPS for America Act in 2022 and U.S. restrictions on exports of semiconductors and manufacturing equipment to mainland China are tangible signs of the possible development of dual supply chains for some products (for example, graphics chips for artificial intelligence), or what some are calling a “bifurcation of global technology markets.” During the remainder of 2023, it will become clearer whether other countries will follow the United States and issue export restrictions of their own. So far, the government of the Netherlands has indicated restrictions on semiconductor machinery exports will be applied, but their final form has yet to be determined. Similarly, the Japanese government has announced plans to limit the export of chipmaking equipment to China but has yet to apply formal restrictions.

Export restrictions should not be taken to mean there will be a full split in all technology supply chains. In many assembled goods, for example smartphone and computer manufacturing, there are significant economies of scope, and we expect to see companies operating in both countries.

Meanwhile the European Union’s Carbon Border Adjustment Mechanism (CBAM) has the potential to reform global supply chains over the coming decade. CBAM will tax “carbon-intensive products” imported into the European Union in an effort to keep European companies from moving production to or importing from countries with lower environmental standards. Cross-border trade in raw materials and their derivatives will become subject to tariffs set in line with the origin countries’ own environmental policies.

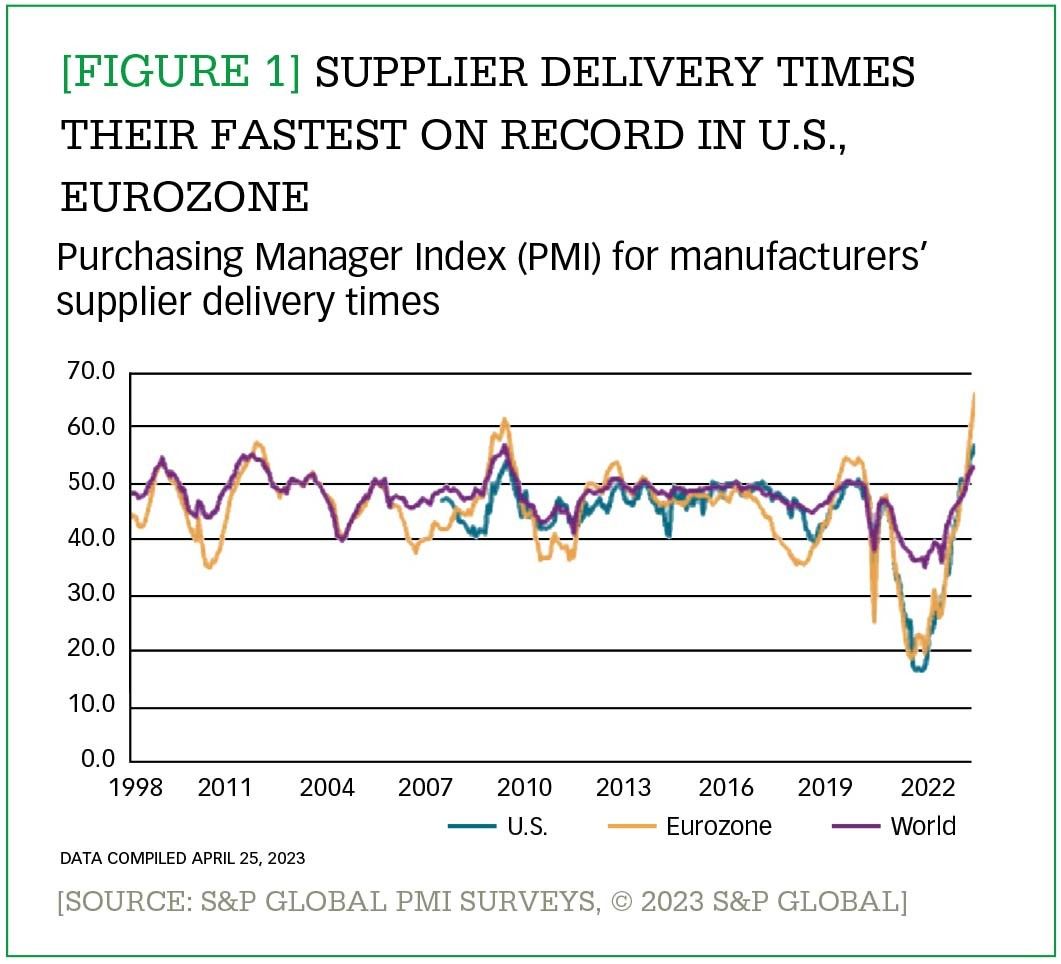

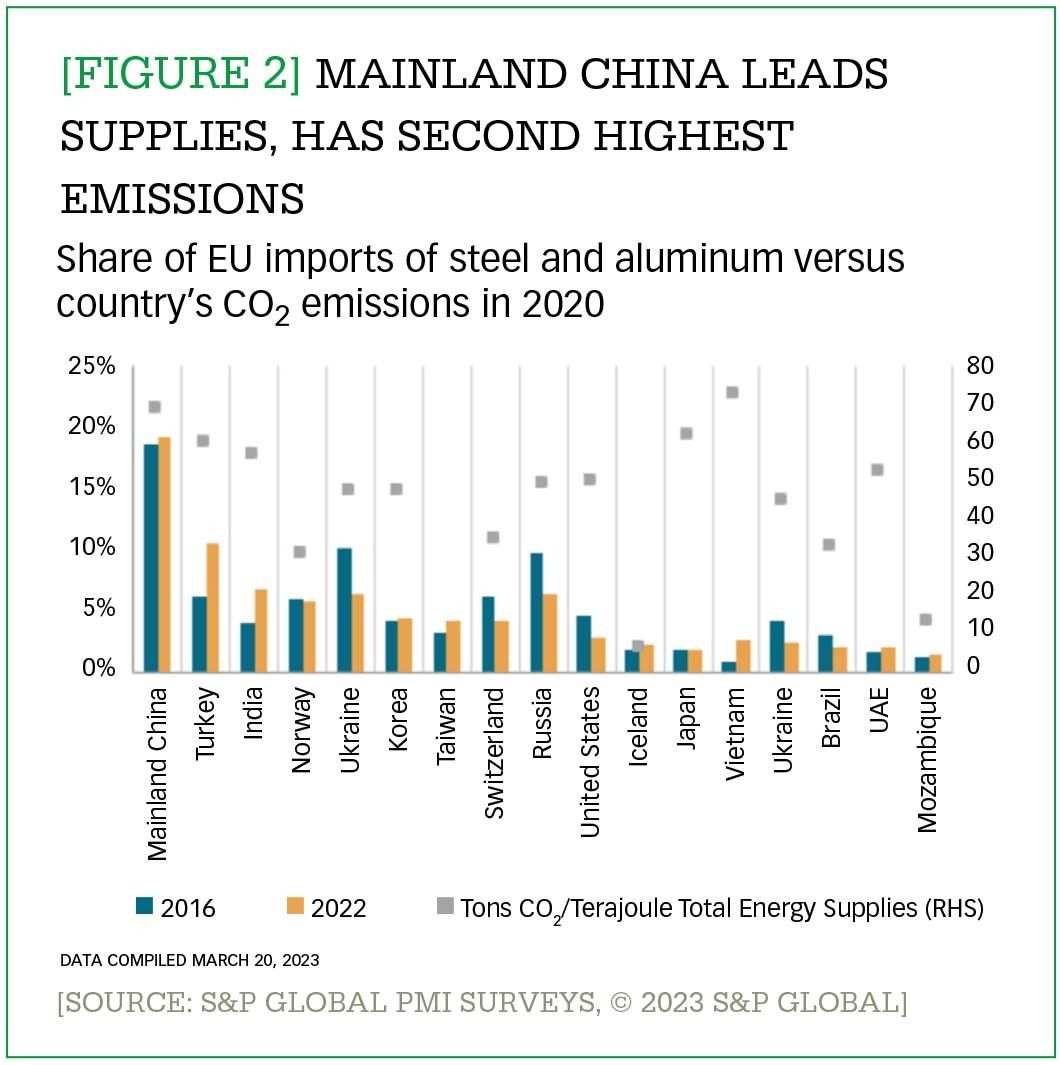

In 2023, the main impact will come from a requirement for importers to start reporting the greenhouse-gas emissions embedded into the covered imported products. That is a quarterly requirement with a deadline of 30 days after the end of the quarter. In the long term, the effect on aluminum and steel products may have the widest implications for global supply chains. Mainland China and Vietnam have the highest carbon dioxide (CO**subscript{2}) intensity among major suppliers of steel and aluminum to the European Union. Mainland China is also the largest supplier of those products. (See Figure 2.)

[FIGURE 2] Mainland China leads supplies, has second highest emissions

Enlarge this image

In summary, logistics networks look to finally work their way through the repercussions from the COVID-19 pandemic. However, that does not mean that supply chains will completely return to how they operated pre-2020. Some companies continue to explore significant changes to their sourcing strategies in efforts to increase supply chain resiliency or respond to government regulations.

{kind=link}

{kind=link}