The first two articles in this series discussed the state of Incoterms rules and how they are structurally challenging to understand and use correctly. The articles made the case that every trade is impacted by Incoterms rules1 and that the pain of using current Incoterms, multiplied millions of times per year across the world’s economies, suggests that fixing these pain points should be a priority.

There are two possible approaches for improving the Incoterms situation: 1) educate and train everyone thoroughly on using today’s Incoterms to their best advantage, or 2) simplify Incoterms. In fact, these are not mutually exclusive. However, the first solution entails a sustained campaign to directly and permanently change the values and behaviors of millions of industry professionals, which is no small task, and one that never ends. The second only entails some diligent and thoughtful work by a few smart people working in the International Code Council (ICC). This may also be no small task, but it is orders of magnitude more realistic. For practical reasons, we believe this second approach is the right place to start.

Simplifying Incoterms should result in a better experience for every level of Incoterms use—from new learner to seasoned expert; from supplier, to carrier, to customer. Let’s consider a wish list for a better ruleset.

1. Simplicity: A better ruleset should begin with the goal of simplicity, which means a common and consistent structure that results in easily transferrable learning. Deeply understanding one rule should make it very easy to quickly understand any of the rules because the way they work is similar and predictable. If one element of a rule uses a letter to indicate the scope of the rule, for example, then every rule should as well.

2. Clarity: A ruleset that is clear will be one that communicates quickly and openly what each rule’s scope, purpose, and application is, leaving no room for second guessing or judgment calls. More importantly, a clear ruleset will avoid ambiguity, not only between rule descriptions but also about which rule is appropriate for a given circumstance.

3. Parsimony: A parsimonious ruleset will cover all the necessary bases with a minimum of overlap between rules, and zero unnecessary rules.

4. Completeness: A complete ruleset will provide all the power the industry needs to easily explain the obligations, risks, and costs of any trade that can be done, without resorting to using the contract language to distort the rule.

Note that the current Incoterms ruleset fails on each of these dimensions of quality,2 so succeeding on even one dimension should be worth a change. We shall try to succeed on all four dimensions. Embedded within these dimensions is larger notion of “usability” that really matters. When the logistics arm of the organization looks at their responsibilities, the Incoterms rule needs to firmly fix in their minds a correct impression of what those are.

A new proposal

We begin by blowing up the ruleset and starting from first principles. We have a few important constraints in how the new ruleset would look, derived by the approximate way of thinking through the choice of term:

1. The rules need to immediately communicate scope, meaning the approximate point of destination. Is this going to occur in the seller’s country, or in a foreign country after export?

2. One should not have to worry about mode of transportation in picking a rule. Each rule should work equally well across any of the modes.

3. Each rule should clearly reveal whose responsibility it is to move materials at the point of delivery without digging into the rulebook.

4. Each rule should be crystal clear about when risk transfers. The answer should not be driven by context or interpretation.

5. Every combination of delivery point, ultimate destination, loading terms, risk transfer behavior, and insurance should be possible, enabling every possible logistics movement.

To create such a flexible ruleset, with a minimum of rules to master, each rule will need to be extensible in a modular way. As it turns out, the current Incoterms ruleset already sports a feature that enables a limited amount of modular extensibility. Each rule is written not just with the three identifying letters but also with a parenthetical modifier naming the point and place of delivery, followed by the version of Incoterms in effect. So, the obvious path forward is to create a limited amount a very clear rules that are made limitlessly flexible by a structured set of modifiers for all the combinations of logistics outcomes needed.

The simplest version possible would be just two Incoterms rules. Let’s call them “free carrier” (FCA) for any movement where the delivery occurs domestic to the seller, and “delivered after export” (DAX) for any movement where the delivery occurs after export. Every movement falls into one of these two categories, and this distinction is arguably the main filter between what buyer and seller must do. However, using these two rules as traditionally understood would be woefully inadequate. So how might we modify them to be maximally flexible?

Let’s determine all the necessary degrees of articulation we’ll need. First, we need to know the point and place of delivery (P&P), which is, of course, already a feature of Incoterms. Next, we need to know who will do the materials handling at transfer point. This factor is the major distinction between all the “F” terms,3 apart from modality, so let’s add a modifier for that. With just these two rules and these two modifiers, we can successfully re-create the bones of the current EXW (ExWorks), FCA, FOB (free on board), FAS (free alongside ship), DAP (delivered at place), and DPU (delivered at place unloaded), minus a few details.

To replicate the current “C” rules4 we’ll need two more modifiers: one to describe the risk transfer point and one to indicate the need for insurance. With these in place, our new DAX can specify a delivery point late in the movement, but a risk transfer point early in the movement. CPT (carriage paid to) and CFR (cost and freight) are taken care of, plus CIF (cost, insurance, and freight) and CIP (carriage and insurance paid to) are handled by adding the insurance modifier. This allows us to handle scenarios where the buyer needs the expertise of the seller to get the cargo booked, sent, and delivered on their behalf, but where the seller isn’t willing to bear the risk (or wait to recognize revenue). Using DAX with a delivery point near the buyer but specifying that the risk transfers once the seller hands the cargo off to the main carrier, successfully satisfies both parties.

Notice, though, that if we’re now specifying the point of risk transfer, we now have maximal control to create precisely the risk profile both parties are most comfortable with. The risk transfer point can be specified to be anywhere along the way, not just the few places the current “C” Incoterms rules demand. Notice also that insurance can now be part of any trade, not just ones whose risk and responsibility is split, as with the current “C” rules.

Finally, we need to know that the newest Incoterms rules are in effect, so we’ll continue to use that modifier. Let’s call the new ruleset proposal “Incoterms 2030.” With all these modifiers in place, we can now replicate EXW, FCA, FAS, FOB, CFR, CIF, CPT, CIP, DAP, and DPU. Not only that, but these two rules can handle situations that those 10 rules cannot, such as a situation where risk passes early, but the seller arranges shipping to the door of the customer and unloads the cargo. It can even handle situations where risk passes after the delivery point, such as a scenario where the seller unloads and risk only passes once the cargo is installed and calibrated at the customer’s site. This situation cannot be handled by Incoterms 2020 but is trivial using Incoterms 2030 just by being explicit about the points of delivery versus risk passage.

Here is what the resulting two rules might look like, as templates waiting to be filled in with the relevant details:

1. FCA (P&P, loading, risk transfer point, insurance, Incoterms 2030)

2. DAX (P&P, loading, risk transfer point, insurance, Incoterms 2030)

If “risk transfer point” or “insurance” are left blank, we can have standard assumptions. For risk, a blank space would mean that risk transfers in lockstep with delivery. For insurance, we would assume that no insurance is required, for example. Or, we could simplify further and just require responses for all modifiers, no exceptions. Either way, these resulting rules are so radically simple that it would be almost impossible to select the wrong rule, and the details of the resulting logistics performance are so up-front that it would be almost impossible to be confused about them. Any ambiguity in the specification (such as with a missing or conflicting modifier) is front and center to both parties and forces communication to take place early to settle underspecified or inappropriately specified details.

One further distinction we might want to introduce is between purely domestic sales, where the end customer is domestic and no export will happen, versus export sales, where additional due diligence and documentation is necessary. The responsibility as a seller is to ensure export compliance, and so might split our new FCA into two rules: free carrier domestic (FCD) for domestic sales and free carrier international (FCI) for international sales. This change will signal to all parties the additional responsibilities associated with the international trade and prepare the seller for the appropriate degree of packaging. This change also has the benefit of ensuring that none of the new rules are superficially similar to the existing rules, helping to establish a clean break from past usage (and the defunct Universal Commercial Code).

Given this, our new and improved ruleset now has three rules, instead of 11:

1. FCD (P&P, loading, risk transfer point, insurance, Incoterms 2030)

2. FCI (P&P, loading, risk transfer point, insurance, Incoterms 2030)

3. DAX (P&P, loading, risk transfer point, insurance, Incoterms 2030)

Any improvement to the Incoterms would have huge positive implications for global trade.5 This improvement, we submit, would be truly enormous due to the reductions in confusion and increases in power and flexibility. As an example, consider a scenario where a company is importing an item and unloading the item from the ship. Right now, without further information, the correct rule to use might be CPT, CIP, CFR, or DAP, depending on multiple small variations on the buyer’s intent. Worse, DPU (previously DAT or delivered at terminal) will seem like a reasonable option because of its historical usage at terminals, even though it calls for the seller to unload. Contrast this to the Incoterms 2030 reality, where the only conceivable choice is DAX, and the buyer just needs to name the appropriate terminal, say they are unloading, and (maybe) specify the point of risk transfer and whether they need insurance. Simple and powerful, and more like ordering from a menu than wielding arcane knowledge.

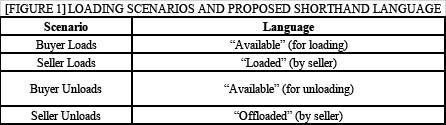

Standard language around writing these modifiers is possible. Points and places (P&P) are (or should be) straightforward. Loading language could be quite straightforward as well, as there are only four scenarios: buyer loads, seller loads, buyer unloads, and seller unloads. (See Figure 1.)

[FIGURE 1] Loading scenarios and proposed shorthand language

Both buyer actions, whether it’s loading or unloading, require the same action from the seller: make the cargo available for the buyer to handle the material. As such, both can be handled by the same short-hand instruction to the seller, which is that the cargo is delivered once it is “available” to the buyer at the point and place of delivery. For the two seller actions, different instructions are needed for the seller. “Loaded” tells the seller they need to handle the cargo onto the next vehicle, be it ship, truck, rail, or aircraft. “Offloaded” tells the seller they need to remove the cargo from the arrival vehicle onto the ground at the point and place of delivery, necessitating handling equipment perhaps. In any case, these modifiers allow the three Incoterms 2030 rules to handle the various capabilities of the existing FCA, plus the variety of “F” rules, and some scenarios that cannot be currently handled by Incoterms. If the point and place is specified as the quay alongside ship X, and the loading modifier says “available,” then the rule is recreating the current “FAS.” If instead the modifier says “loaded”, then the rule is recreating the current “FOB.” As a reminder, though, the Incoterms 2030 can apply to any mode, so it works equally well to specify a rail terminal and “loaded” to effectively synthesize “FAS” or “FOB” with rail in a way that Incoterms 2020 does not endorse.

Standard language on insurance would simply be “Class A,” “Class B,” “Class C,” or “none,” and the assumed terms would be 110% of the value of the cargo, consistent with current use. These terms differentiate the level of insurance coverage required (with the industry standard of “Class C” signifying the least coverage and “Class A” signifying the most coverage).

The only remaining variable that is not yet handled by this proposal is that of customs clearance. Incoterms 2020 contains a rule that requires the seller to clear customs in the destination country on behalf of the buyer. As noted in our second article, there are many potential problems with having a rule that involves such an arrangement, not least of which is that sometimes the contract cannot be executed because the seller lacks import privileges. Therefore, we humbly suggest that matters of customs clearance, like those of payment terms and title, are best left to the contract to specify. In this proposal, DAX could be augmented—not changed—by custom contract language specifying that the seller clear customs, thereby re-creating the current DDP (delivery duty paid). Moreover, Incoterms 2030 is flexible enough to do that and have the seller perform the unloading, which Incoterms 2020 cannot.

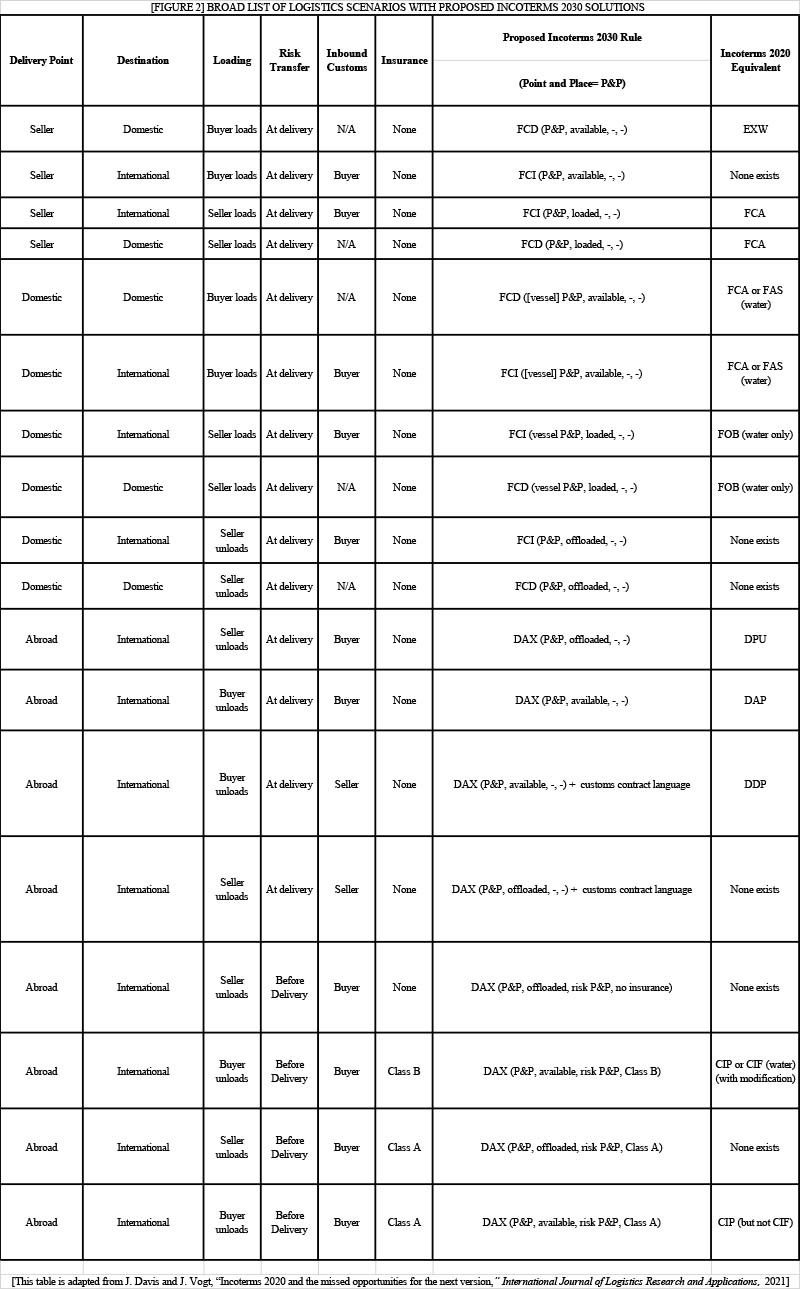

The resulting Incoterms 2030 ruleset consists of three simple—yet enormously flexible—rules that are easy to learn and understand and that clearly communicate all aspects of the trade at a glance. For each conceivable logistics application, there is a clear way to express, with no ambiguity, what should happen and by whom. Figure 2 is a large cross-section of possible logistics scenarios, and how Incoterms 2030 would address each.

[FIGURE 2] Broad list of logistics scenarios with proposed incoterms 2023 solutions

It is time for the ICC to kill Incoterms as they stand today. But, like a phoenix, Incoterms must rise again, made all the better to lubricate trade and logistics across the globe. Let’s make a modern Incoterms by sweeping away the historical structural problems while building on the knowledge the previous versions have generated. Incoterms need to be rewritten into a consistent, clear, concise, and parsimonious ruleset that works for all trade and does not rely on mere goodwill between buyer and seller to overcome logistics hurdles. This proposal for Incoterms 2030 is a path forward. But the need for change is clear, and the rewards for forging this path will make the challenges seem insignificant.

Notes:

1. “Incoterms” or “International Commercial Terms,” is a legally registered trademark of the International Chamber of Commerce.

2. J. Davis and J. Vogt, “Incoterms 2020 and the missed opportunities for the next version,” International Journal of Logistics Research and Applications, 2021: p. 1-24.

3. “F” rules deal with goods that are exchanged from the seller’s facility up (and including) to the port of international departure.

4. “C” rules deal with goods exchanged at either the port of export or the port of import (or in between).

5. J.A. Spanogle, “Incoterms and UCC Article 2—Conflicts and Confusions,” The International Lawyer, 1997. 31(1): p. 111-132.