This article marks the first installment of a three-part series by McKinsey & Company on managing supply chains in emerging markets. In addition to Latin America, the series will also look at Asia and Africa. Each article will include an overview of business and logistical conditions, followed by recommendations for successfully navigating the supply chain challenges that are specific to that region.

Many companies today consider Latin America to be an intrinsic part of their emerging-market strategy. And no wonder: With a total gross domestic product (GDP) of US $5.5 trillion, the region offers the potential to reach more than half a billion consumers. Moreover, Latin America's GDP is projected to grow 4 percent annually until at least 2017, twice as fast as GDP in the major developed economies.

![[Figure 2] Local transportation costs can be significant](/media-library/20140613latin-ex2.jpg?id=53612049)

![[Figure 3] Typical Latin American supply chain clusters](/media-library/20140613latin-ex3.jpg?id=53612050)

![[Figure 4] Latin America's supply chain maturity gaps](/media-library/20140613latin-ex4.jpg?id=53612051)

In the aggregate, people in Latin America are relatively well-off compared to other developing markets. GDP per capita in Brazil, for example, is 45 percent higher than that of China and three times that of India. But despite its degree of personal wealth, the region is still very much an emerging economy. Its total GDP is only one-third the size of that for the United States, and 40 percent of Europe's. Per-capita GDP is lower still: one-fifth that of the U.S. and a quarter that of the main European Union (EU) countries.

All of this means that companies operating in Latin America transport smaller volumes and less value there than they do in more mature markets. Volumes can vary significantly from country to country and region to region, too, making it hard for companies to take advantage of scale effects by consolidating regions, or to design efficient transport networks. Despite such challenges, and as the statistics above suggest, Latin America is a promising market that merits time, attention, and investment.

Historically, many multinational companies have focused on one or two key markets in the region, such as Brazil and Mexico. These markets are indeed important to the success of any company doing business in Latin America. But in order to access this region's full potential, companies must strengthen their coverage across the entire area. From a supply chain perspective, this necessity forces them for the first time to think about Latin America as a whole as they seek to drive up service levels while keeping costs under control. To do that well, supply chain managers must first understand the region-specific challenges they will face, and then adopt strategies for mitigating or overcoming them.

Challenges on a grand scale

Look at a map, and the challenge presented by the region's sheer geographic size becomes clear. The flying distance between two important commercial centers in South America, São Paulo (Brazil) and Santiago (Chile), for example, is 2,500 kilometers, around the same as the distance between London and Moscow. The flying distance between São Paulo and Mexico City is 7,500 kilometers, the same distance as from London to Kathmandu.

This huge spread might not be much of a problem if the spaces between major population centers were occupied. But that is not the case. The direct, 2,500-kilometer route from São Paulo to Santiago passes within 100 kilometers of only two secondary cities (Mendoza and Córdoba in Argentina). In fact, the top 10 cities in Latin America are 3,900 kilometers apart on average. That's 2,500 kilometers more than the same figure for Europe. If you exclude Brazil's relatively concentrated population, the average rises to 4,200 kilometers.

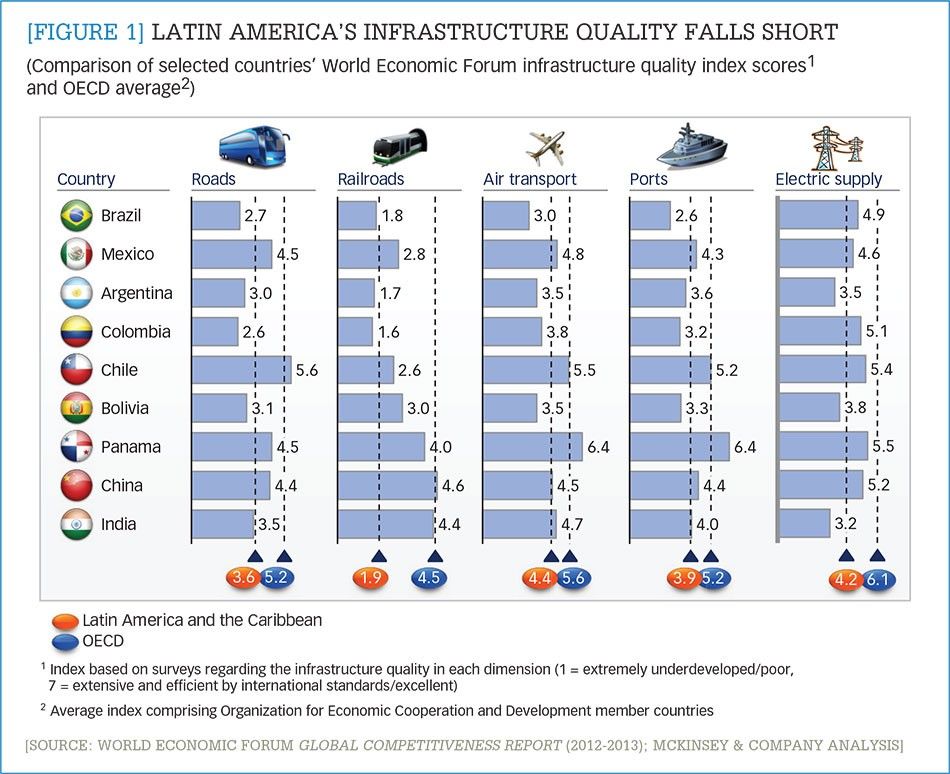

Covering these huge distances is difficult. According to the World Economic Forum, most Latin American countries fall behind world averages for infrastructure availability and quality. These disparities are shown in Figure 1. Moreover, rail coverage is poor compared to EU or U.S. standards, and ports are running at many times their designed capacity.

Countries in the region rely heavily on road transportation. In Brazil, 60 percent of the total domestic ton-kms (metric tons times kilometers traveled) transported per year moves over the road; in Colombia, it's 77 percent, and in Mexico, 90 percent. That is much higher than in many other economies. In China, for instance, that figure is 21 percent, and in the United States, 36 percent. This is significant because road transport is considerably more expensive than transportation by rail or ship. Road transport can also be slow: Average road speeds across Latin America can vary from 10 to 80 kilometers per hour, creating important implications for supply chain planning and product shelf life. The region's natural barriers, like the Andes Mountains and the Amazon River Basin, add further cost and complexity to the transport picture.

The challenge of high costs

Latin America's great distances and poor transportation infrastructure are a factor in the region's high costs. Shipping a 20-foot ocean container from Mexico or Colombia to Brazil costs about the same as shipping a container to Brazil from China or Hong Kong, although the transit time, at 20 to 23 days, is some 10 days shorter. Transporting the same container from Europe to Brazil would be cheaper. And, as Figure 2 shows, local transportation can be very expensive—in fact, it costs more to move a container between major cities in Argentina than it would to ship that same container from Hong Kong to Buenos Aires.

Although Latin America as a whole has the characteristics of an emerging economy, for many companies operating there it is not a true low-cost region. Labor costs, for example, are significantly higher than those of China—up to 3.5 times higher in the case of Brazil. And while labor rates are not rising as fast as China's, the gap is likely to remain significant until at least the end of the decade.

This is true not just for warehouse, distribution center, and factory workers but also for managers and executives. Professional salaries in Latin America have risen dramatically in recent years as demand for key skills has outstripped supply. The cost to employ an experienced supply chain manager in Brazil, for example, is now on a par with that for the equivalent role in the United States.

Challenges across borders

Latin America—for the purposes of this article, the Spanish- and Portuguese-speaking countries in Central and South America, plus Mexico—includes 17 countries, each with its own customs and tax laws, bilateral agreements, and tariffs. In Brazil, tax regulations even vary significantly from state to state. Many countries in the region are trying to protect their local industries through import duties, quotas, and tax regulations. The sheer complexity of these rules makes it difficult for companies to simply keep up to date with current charges and regulations, let alone account for all the many variables affecting their supply chain optimization efforts.

Political developments can exacerbate supply chain challenges. Tensions between countries in the region frequently lead to the closure of border crossings, or to limitations on the movement of goods. In the past, such situations have arisen between Colombia and Venezuela, Venezuela and the United States, and Bolivia and Chile, to name three examples. Internal instability can also lead to unsafe road conditions or closures, with activity by guerrillas in Colombia and by coca producers in Bolivia being two notable recent examples.

To complicate matters even further, the region has a tradition of government-controlled exchange rates, with a tendency to engage in local "currency wars." As a consequence, sudden devaluations can make one country more or less competitive in relative terms without any significant changes in productivity. For example, after Argentina recently devaluated its currency, Brazil's currency also fell in dollar terms—but not enough to compensate for Argentina's devaluation, which made Argentine goods relatively more competitive in Brazil. Combined with the often painful bureaucratic processes at ports and border crossings, these effects can make managing manufacturing and distribution footprints, lead times, and inventories in Latin America more an art than a science.

Supply chain strategies for success

Taken together, these challenges make it difficult for companies to optimize the performance of their Latin American supply chains. They also have driven some supply chain decisions that seem illogical at face value.

For example, it is not uncommon for companies to maintain idle manufacturing capacity in both Brazil and Argentina. This strategy allows companies to quickly change the percentage of goods they are manufacturing in one country or the other in response to changes in exchange rates or tax policies, or when there are border issues. Another example: In Argentina, tax policies have encouraged many consumer electronics companies to set up assembly plants in Rio Grande, a city in the extremely cold Tierra del Fuego region that lies around 3,500 kilometers south of Buenos Aires, Argentina's main market. Similarly, tax policies explain why many consumer goods and electronics manufacturers have large plants in Manaus, Brazil, located in the Amazonian forest region some 4,000 kilometers from São Paulo, Brazil's main market.

Despite the challenges outlined above, some multinational and local companies have built extremely successful Latin American businesses. An intrinsic part of this success has, in many cases, been the adoption of a Latin America-specific approach to the design and execution of their supply chains, together with a targeted investment in supply chain capabilities in the region. Let's review some of the key elements of these strategies.

A significant local footprint

A significant local footprint forms a core part of the most successful Latin American supply chain strategies. The top four mobile handset makers in Brazil and Argentina each manufacture or assemble locally more than 90 percent of the products they sell in those countries. Argentina's top automotive brands all produce significant numbers of vehicles in the country, both for local consumption and for export to other regional markets, especially Brazil, thanks in part to special treaties for bilateral automotive trade between the two countries. Maintaining this local footprint, especially in expensive places such as Argentina and Brazil, can be significantly more expensive than concentrating production in one low-labor-cost country. However, doing so allows companies to be faster and more agile in a volatile market.

From operational expedience ... In many cases, these localized supply chains have been specifically designed to meet the requirements of local tax and duty regimes or to overcome import quotas. In the case of mobile handsets, for example, this may entail sourcing 80 percent of the component value in the handset from within the country. The benefits of this type of tax-efficient approach can be highly significant, often far outweighing the potentially higher costs of local manufacture. One consumer products company, for example, was able to increase its contribution margin for a key product category in Brazil by 30 percent by shifting to local production, despite the fact that doing this also increased its cost of production by 30 percent. The difference came entirely from savings on import duties, internal tax benefits, and other regulatory effects.

... to competitive advantage. While regulatory conditions may have driven the development of local footprints, the most successful companies take deliberate steps to turn both of these factors into a source of competitive advantage, typically by tailoring products to suit the needs and tastes of Latin American consumers. For example, in the 1980s, the German carmaker Volkswagen designed the subcompact Gol specifically for manufacture and sale in Brazil. The vehicle was built to replace the popular but aging Beetle, catering to local tastes and taking advantage of tax breaks for local production. It was later introduced in neighboring Argentina under a similar strategy. The Gol has been the best-selling car in both Brazil and Argentina; counting all its variants, it has sold over 10 million units, and VW has used its Brazilian factories to make compact, low-cost city cars for other international markets.

In the apparel industry, "fast fashion" player Zara makes design adjustments especially for Brazil, something that it does not do for most other countries. It has also cultivated a flexible local supply base, which allows it to quickly change its production plans in response to demand. Other apparel manufacturers have turned their Latin American supply chains into sources of product for export, increasing scale and allowing them to accumulate export tax credits, which help to increase the profitability of the local operation.

An appropriate organizational split

Few Latin American countries offer a large-enough market to justify an entirely local supply chain. A strong supply chain design requires companies to define the right regional split, one that maximizes the benefits of scale while also reflecting the individual needs of particular regions.

The right supply chain clusters. An efficient supply chain organizational split must take into account the physical (long distances, jungles, mountain ranges), cultural (different languages, incomes, and tastes), and political barriers in Latin America. Language differences may require multiple labeling variants for adjacent regions, for example, while the existence of various free trade agreements can have significant implications for the movement of goods between and within countries, sometimes even requiring companies to change package sizes or the number of products per case to meet local regulations.

As a result of these complexities, most large companies operating in Latin America choose to segment their supply chain organizations into regional "clusters." These clusters are designed to balance market size, cultural similarity, and the cost and ease of moving goods across internal borders within the cluster. A typical approach uses four segments: North and Central America (including the Caribbean countries and Mexico), Brazil (which is often large enough to justify a dedicated supply chain organization), the Northern Andean Region, and the Southern Cone. Figure 3 outlines these typical segments and the main considerations that affect where companies will decide to draw those lines.

The right organization within each cluster. Within and across these supply chain clusters, companies must then make the right decisions to ensure that research and development, purchasing, manufacturing, sales, warehousing, and distribution assets are located in a way that balances cost, service, and local taxation. Often this entails concentrating assets in the largest market in a cluster, but the best design depends very much on the details of each organization's products and markets. Ideally, the organizational structure should foster quick reaction at the appropriate level within and across the established network cluster.

Pragmatic, agile execution

Leading companies modify their supply chain execution strategies to suit the realities of operation in Latin America. The best of them do this with a "hope for the best, prepare for the worst" approach, in which they accept the higher levels of risk and volatility in the region and run their supply chains accordingly. This requires a high degree of agility and flexibility, both on a day-to-day basis and in the face of changing, longer-term trends. That, in turn, calls for significant investment in supply chain capability and talent, something that many companies struggle with today.

Tactical responsiveness. A common strategy used to meet the day-to-day challenges of operating in Latin America includes the use of higher risk-adjusted safety stocks than would be typical elsewhere in the world, in order to maintain continuity of supply if local logistics activities are subject to delays or disruptions. To keep the costs of higher inventories under control, companies also take steps to improve the overall agility of their Latin American supply chains. They do this by actively monitoring changing supply chain conditions in order to have the best and earliest possible warning of situations that may affect their ability to cost-effectively deliver to customers, and then dynamically adjusting supply chain parameters in response.

One consumer goods company with manufacturing facilities in Argentina, for example, found that consistent supply to customers in Brazil was affected by variations in the time required for goods to clear customs at the border, which could vary from a single day to several weeks. To minimize the effect of these delays, the company monitored border transit times and dynamically adjusted its safety stocks in Brazil, increasing them when border congestion rose and cutting them back to reduce costs as goods began to move more freely.

Strategic agility. Leading companies improve their ability to react to changing situations in two ways: by creating and rehearsing contingency plans to deal with a wide range of possible scenarios, and by improving their ability to collaboratively plan for and react to unpredicted events. These capabilities are critical in Latin America, where political and regulatory changes—both expected and unexpected—can have a swift and significant impact on supply chain costs and efficiency.

In 2012, for example, the Brazilian government announced a law with strict new limits on the time and distance that truck drivers could cover between mandatory rest stops. From one year to the next, these requirements had the potential to increase the cost of road transportation in the country by up to 30 percent, and to lead to a shortage of both vehicles and drivers.

One leading food company quickly recognized the potential impact the new law would have on its supply chain costs, and it embarked on a wide-ranging response while the law was still being drafted. The company established communication with the government at the top level of the organization, with the aim of preventing certain unreasonable clauses from being written into the law. It redesigned its distribution footprint to adjust for longer lead times and shorter feasible daily distances. It also opened early negotiations with suppliers and transport companies to secure additional capacity. As a result of this quick and comprehensive response, the company helped to ensure some critical modifications were made to the draft law before it was passed, and it was well positioned to minimize additional costs and potential disruption by the time the law came into force.

A focus on capabilities. Design and execution of an effective supply chain in the challenging conditions encountered in Latin America requires considerable individual and institutional capabilities. As the examples earlier in this article show, some companies that are operating in the region have developed these abilities to a high level.

However, our research has shown that these leading organizations are the exception, rather than the rule. Since 2010, we have evaluated the supply chain capabilities and performance of more than 600 companies worldwide, using the "maturity assessment" diagnostic tool included in the McKinsey Supply Chain 360 benchmarking suite. The maturity assessment tool covers hundreds of practices, which are grouped into 20 topic categories. For each practice, the evaluated companies received a 1-5 score that reflected the current implementation level at the company. The Latin American consumer goods supply chain organizations in our survey had an average score across all dimensions of 2.73 out of five, compared with 3.1 for Europe and 3.13 for North America. As shown in Figure 4, this research reveals that among Latin American companies (both locally owned and locally based multinationals), critical maturity gaps exist in two aspects of supply chain management that are among the most important for success in the region: risk management and forecasting.

Many companies operating in Latin America need a systematic approach to compensate for these critical gaps in supply chain maturity. Above and beyond gaps in institutional capabilities, the shortage of supply chain talent in the region makes it difficult to fill these skill gaps through recruitment alone. Instead, companies need to build their own individual and institutional capabilities from within. The best organizations do this through a combination of actions, like facilitating the exchange of knowledge and best practices from their global supply chain organizations, investing in capability building, and transforming their local organizations to better adapt to local conditions.

Unlock Latin America's potential

Latin America offers companies a different kind of emerging market, with faster growth than most mature economies and a wealthier starting point than much of Asia. Unlocking this potential will require strategies to overcome the region's political and geographical complexities, however. The only way to do that is by deploying smart, flexible, and pragmatic supply chains that can respond to challenges like the ones outlined in this article.

For companies that want to be successful in this part of the world, it is well worth the effort and investment required to implement those strategies. The financial payoff will be substantial: Our research has found that for companies that successfully master this approach, the typical impact includes simultaneous increases in order fill rates of about 10 percentage points (which would result in higher sales), as well as decreases in inventory on the order of 30 percent and in transportation costs of approximately 15 percent.