Editor’s Note: Every year the Council of Supply Chain Management Professionals (CSCMP) publishes a State of Logistics Report that seeks to understand the logistics industry by assessing the macroeconomic situation and looking in some detail at its major subsectors. The following is excerpted and adapted from the “Executive Summary” of this year’s report, which was written and compiled by the consulting firm Kearney.

The overarching theme of last year’s State of Logistics Report was that supply chains were fundamentally “out of sync” as a result of disruptions related to COVID-19. While the pandemic is still not fully behind us—and may be with us in some form or another for several years to come—it is no longer closing shops or congesting seaports.

To a large degree, then, the period studied by this year’s report—the calendar year of 2022 and the early months of 2023—has been about getting back “in sync.” … It has fundamentally been about the resetting of relationships, assumptions, and practices for a world transforming. A central feature of this transformation is a shift among logistics executives from strictly transactional perspectives to a more strategic and holistic sense of their function’s role.

The transformations rippling through the logistics sector are the result of rapid evolutions in delivery requirements and consumer expectations just as old assumptions about supply chain stability are being disrupted. As e-commerce and direct-to-consumer sales have grown, order fulfillment has become increasingly complex, fragmented, and vulnerable. The deceleration in e-commerce growth should give shippers and carriers some room to build strategic plans until other causes of complexity arise.

Nor is this the full extent of the transformations confronting the industry. Geopolitical disruptions, increasingly potent cyberattacks, and an intensifying cycle of climate-related natural disasters are all placing trade and distribution networks under increasing stress—at precisely the moment when those networks are becoming more essential to companies’ bottom lines.

That’s why thoughtful executives are seizing this moment for a great reset—a revisiting of former arrangements, some of them overtaken by recent events, some of them cobbled together rather hastily amid the confusions of the pandemic. It is time to get clear about what is working now and what is needed to ensure resilience for an uncertain future.

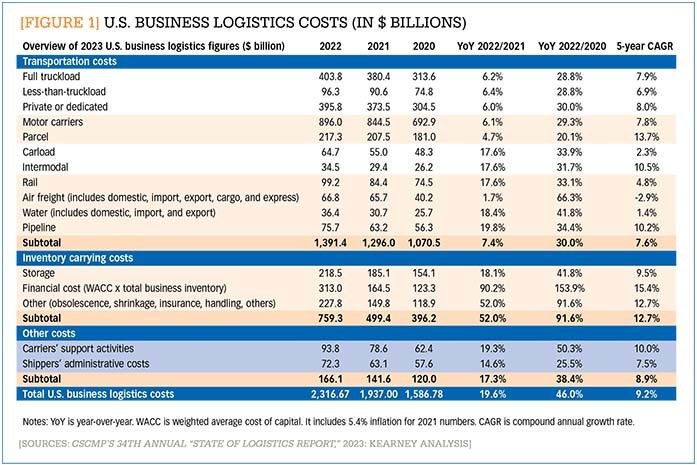

The period covered by this edition of the State of Logistics Report highlights the next strongest cost growth in the past decade and the highest percent of gross domestic product (GDP) ever, as U.S. business logistics costs (USBLC) hit $2.3 trillion in 2022, growing 19.6% year-over-year (YoY) and representing 9.1% of national GDP. (See Figure 1.)

[FIGURE 1] U.S. business logistics costs (in $ billions)

Enlarge this image

Coming off this performance, supply chain demand is likely to remain stagnant or even diminish over the remainder of 2023. The reasons for this are varied and are rooted in lingering uncertainties for the global and U.S. economies.

The International Monetary Fund reports that GDP growth in 2022 was a modest 3.1% worldwide, and predicts 2.9% growth for 2023. For the United States specifically, the picture was a bit brighter in 2022 than many had expected, with growth remaining stable at 2.1% as consumer and business activity showed surprising vitality. While there remains a chance for a domestic recession in 2023, any such downturn is likely to be mild and short-lived.

One lingering shadow across the U.S. economy is inflation. While prices are down from the highs of 2022, they remain elevated across many categories, and much will ride on whether monetary policy can bring inflation to heel without compromising overall economic health.

A primary source of this inflation is also one of the engines of the United States’ persistent growth—a hot labor market, in which unemployment is at or near the lowest levels seen in a half century. This relative scarcity of willing and able workers has had a particularly forceful impact on the logistics sector.

Beyond such immediate sources of uncertainty there are other factors motivating companies to act now to reset their logistical networks. In recent years, the world has seen a resurgence of forces that threaten long-standing assumptions of ever-expanding global trade—forces such as nationalism, protectionism, and even major-power conflict.

For many businesses, reshoring now appears to have shifted from a strategic possibility to a market reality. U.S. companies have been increasingly moving supply chains closer to home. U.S. imports of Mexican manufactured goods grew a staggering 26% according to Kearney’s Reshoring Index.

The war between Russia and Ukraine continues to threaten the stability and prosperity of Europe, while deepening concerns about Chinese intentions have accelerated efforts to redirect manufacturing and sourcing to other nations throughout the Indo-Pacific region and the Americas.

Then there is climate change, which is increasingly influencing the availability of resources and vital infrastructure, as well as the perceptions and expectations of consumers. Companies are increasingly folding sustainability considerations into their business models, and regulators around the world are increasingly requiring that they do so—through a multiplying array of mandates, incentives, and standards.

By now, there are numerous well-proven sustainability strategies that are not only relatively easy to implement but also fit neatly within the logic of the great reset, which emphasizes the virtues of flexibility, efficiency, and resilience—qualities that are only becoming more vital for companies throughout the logistics sector.

A tally of main sectors

Here is a quick survey of how the forces outlined above affected the primary logistics sectors. …

Air: Worldwide air cargo revenue is projected to reach approximately $150 billion in 2023. This is 25% below 2022, when the sector was still profiting from historically high rates, but still 50% higher than the pre-COVID revenue figures from 2019. Several factors have pushed rates back to earth, including a falloff in demand, the return of many shippers to waterborne freight, and a surge in capacity as passenger flights resume and new planes come online. East-West air freight rates dropped 23% from January to December 2022. One bright spot for the sector: The global average jet fuel price index has declined by about 20% since April 2022.

Parcel and last mile: The explosive growth in e-commerce at the height of the pandemic has begun to moderate as shoppers have returned to stores—a development with sizeable implications for parcel companies. Even as the U.S. parcel market has grown to its largest size in history, its percentage of retail sales has begun to flatten. Volumes declined by 2% in 2022 but are expected to grow at a 5% compound annual growth rate (CAGR) over the next five years. Revenues have increased as major deliverers shifted toward a focus on profitability as seen in recent rate hikes. One especially vibrant slice of the parcel and last-mile sector is same-day delivery, which is expected to grow from $6.4 billion worldwide in 2022 to $7.9 billion in 2027, rising at a CAGR of 18.8%.

Third-party logistics (3PLs): Third-party logistics firms took on increasingly significant roles as shippers looked for added expertise to navigate the unusual circumstances arising with the COVID pandemic. Increasingly, shippers are calling upon 3PLs for more specific needs, especially data management, visibility, and analytics. But beyond even this, shippers are increasingly open to trusting 3PLs with the stewardship of entire supply chains—as fourth-party logistics (4PL) capability resurges. Freight under management by 4PLs is growing, though there still are not many 3PLs capable of playing at this more demanding level. As a result, the 4PL market is increasingly concentrated among a handful of larger providers.

Freight forwarding: The freight forwarding market is expected to grow from $48 billion in 2021 to $90.7 billion by 2031, a CAGR of 6.3%. This growth derives from the continued expansion of e-commerce, as well as the ongoing pressure on shippers to trim costs and increase the efficiency of their supply chains. Digital freight forwarding is an especially dynamic market; valued at $2.92 billion as of 2020, it is expected to be worth $22.9 billion by 2030, a CAGR of 23.1%. The trend within the overall forwarding sector is toward more comprehensive offerings, and therefore toward increased market consolidation. However, there are signs the largest shippers may be moving toward more direct relationships with carriers, a move that could deprive forwarders of lucrative potential clients.

Water/ports: Major ocean liners made combined global operating profits of $215 billion in 2022, buoyed by a continuation of high rates from the previous year. That trend lost steam as demand weakened and ship availability returned to something like normal—though an increase in U.S. import volumes in April 2023 may suggest a demand recovery. Following their flush months of 2021 and early 2022, sea carriers face a reckoning: Their 2023 profits are projected at $43 billion, an 80% year-over-year decline. The first quarter of 2023 saw a return of blank sailings, particularly on routes from Asia. As capacity began to open up again, shippers took advantage by renegotiating agreements and diversifying their options—showing a preference for shorter deals, spot markets, mini-bids, and other arrangements that can help them better weather uncertainty.

Motor: Road freight—which is the largest chunk of logistics spending—saw little change in overall volume as shippers weighed concerns about inflation, rising interest rates, and overstocked inventories. At the same time, capacity increased, resulting in a sharp decline in spot rates. These changing dynamics have induced shippers—who turned toward dedicated fleets to address the capacity challenges arising during the peak months of the pandemic—to seek a new balance among dedicated, private, and one-way services. Carrier margins were threatened by low rates and high resource costs, with smaller carriers—reliant on the spot market—under particularly acute pressure.

Rail: Class I railroads saw operating income increase by 8% year-over-year and total revenue by 14%—gains largely attributable to price increases. But while rate hikes boosted railroads’ income and revenue, rising costs undermined operating ratios. The sector also suffered from service-related issues, including increased terminal dwell, ongoing congestion, network speeds that still lagged pre-pandemic velocity levels, and some high-profile derailments. Aggregate carload volume for Class I carriers was static, though volume levels shifted markedly for some product categories.

Warehousing: As companies raced to meet demand for consumer goods during the pandemic, inventories skyrocketed and demand for warehouse space heated up considerably. In 2022, however, that demand waned, resulting in overstock. Warehouse vacancy rates fell sharply, to as low as 2.9%—down 41% from the 4.9% high of 2021, and well below pre-pandemic levels, which tended to hover around 6.5%. These historically low vacancy rates resulted in higher rents, though this rise was mitigated by robust construction of additional warehousing space. Even as available space is increasing, companies are hesitating to occupy it as they try to get rid of excess inventory and use existing space more efficiently. Net absorption peaked in the second quarter of 2022 but then decreased nearly 20% by the fourth quarter. The pricing and availability is expected to be more favorable for shippers in 2023.

Reset and resilience: Preparing for whatever’s next

What’s clear from these sector summaries is that the age of building supply chains just around cost-reduction considerations is over. A new value has taken center stage: resilience.

But the best ways to achieve resilience are not always obvious. They often involve trade-offs among core priorities, such as speed, service, optionality, and savings. These calculations are only becoming more complex and nuanced with time.

To cite just one example, increasing fragmentation of demand means that massive distribution center footprints are becoming less profitable. Yet shippers often need a large footprint to maintain high levels of service and ensure supply resilience.

Logistics leaders are responding by taking a more holistic and comprehensive view of their value chains. They are diversifying their sourcing to avoid overreliance and to ensure ample workarounds in the case of sudden disruption. They are investing in technologies and human capabilities to enhance organizational awareness of what’s happening across the entire network. And they are actively resetting their supplier and carrier commitments, their approaches to customer service, and their expectations of what lies ahead.

Because if the past few years have been any guide, it is wise to make discretionary resets when one can—rather than be compelled to improvise them when one must.

The full 34th Annual State of Logistics Report can be found on CSCMP’s website under the “Resources” tab. The report is free to CSCMP members and $299 for nonmembers.

{kind=link}