The rail industry is currently seeing two separate story lines develop as the intermodal and carload segments follow different paths. One is growing in line with the underlying economy, while the other is declining significantly on strong modal competition.

Intermodal was once thought of as the growth driver of rail volumes, and while it could return to those heights in the future, it has a steep hill to climb. The last 18 months have been ones of disappointment and uncertainty for intermodal. Both international and domestic freight volumes struggled to find their footing after a post-pandemic surge of traffic created congestion all along the supply chain. In recent quarters, intermodal has been buffeted by the tremendous uncertainty created by the lack of a labor contract for dockworkers at West Coast ports and the economic reality of lower-than-average active truck utilization.

While the International Longshore and Warehouse Union and Pacific Maritime Association tentatively agreed in June to terms for a new six-year agreement, it is less clear whether traffic will immediately start to flow back to the West Coast ports. Overall intermodal volume is expected to decline by 8% from 2022’s weak levels, before returning to modest growth in 2024.

Over the last few years, West Coast ports have lost market share to their East and Gulf Coast peers because of a combination of congestion and uncertainty over the now-resolved labor situation. The labor situation dragged on for nearly a year beyond when the West Coast port labor contract expired in July 2022, meaning many shippers diverted cargo for well over a year. In that time, they developed new relationships with drayage providers, ports, and warehousers that they may be unwilling to sever only to return to the West Coast and lose some alternative routes.

The move to East and Gulf Coast ports has eroded one of intermodal’s key advantages over trucking: length of haul. A 250-mile to 550-mile length of haul makes trucking much more competitive compared to rail intermodal than the 2,000-plus mile lengths of haul that are routine for imports from the U.S. West Coast into the interior.

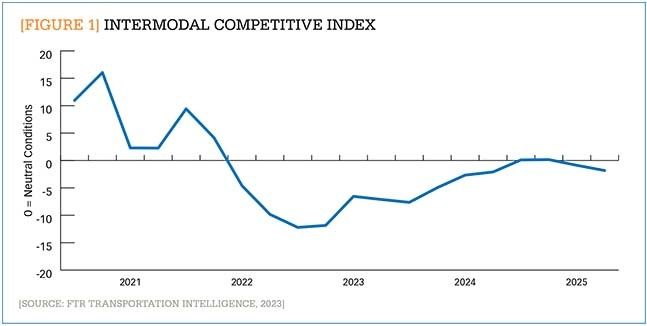

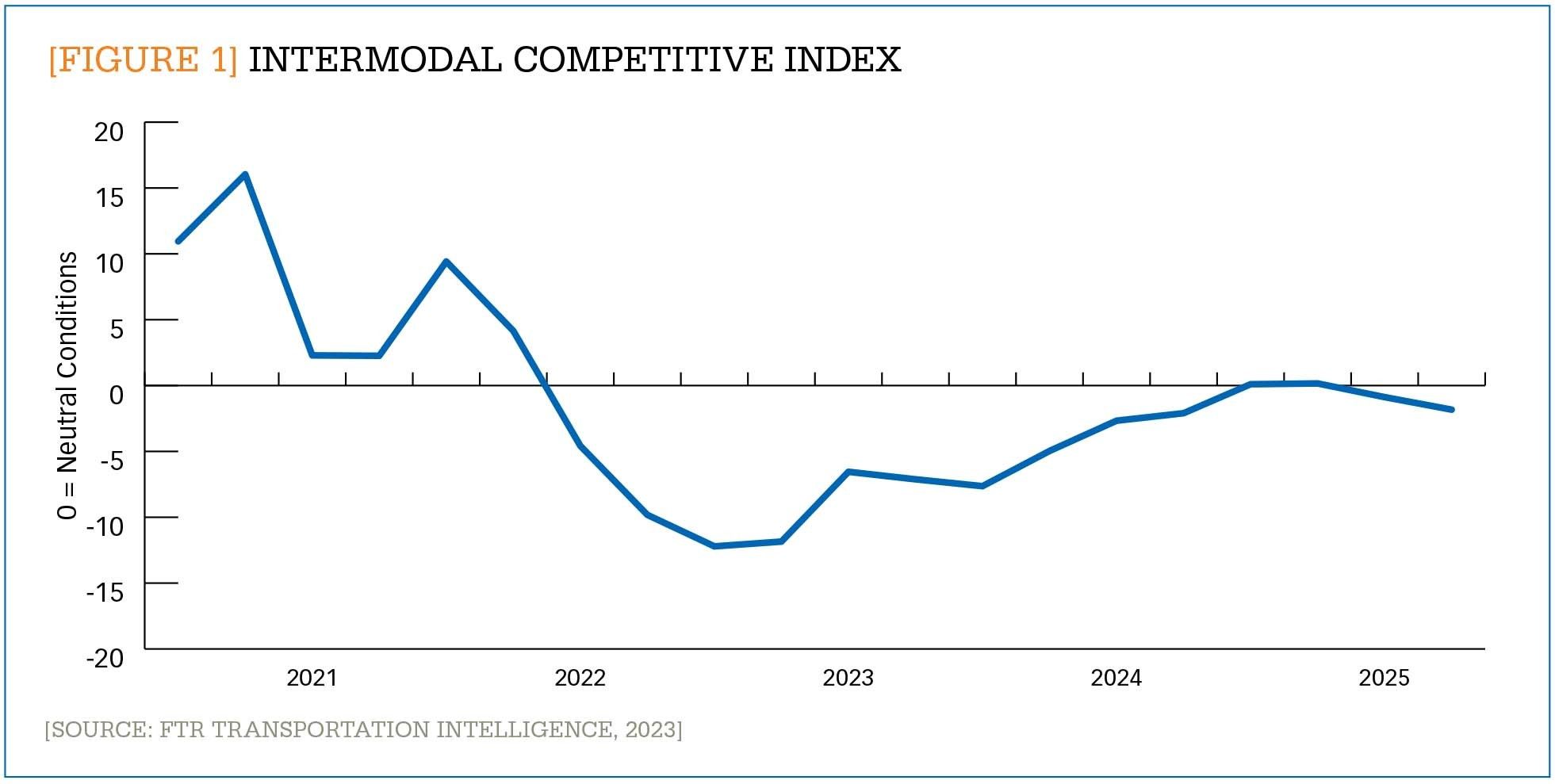

At the same time, active truck utilization declined dramatically over the last few quarters and is below its long-run historical average, making truckers hungry for any and all available freight. As a result, intermodal has had to work to sell its value proposition at a time when rail service was also experiencing struggles. Lower truck rates, combined with the perceived better service reliability of trucking, has made for challenging competitive dynamics for rail intermodal as can be seen in FTR’s Intermodal Competitive Index shown in Figure 1.

[FIGURE 1] Intermodal competitive index

Enlarge this image

That tough competitive environment is expected to remain in place until the second half of 2024, when it will ease back toward a more neutral footing over the course of the year. Until that happens, expect intermodal volumes to remain at or below five-year average levels.

Intermodal wildcard

Carriers have tried to adapt to the changing port dynamics and competitive truck market by introducing new and expanded services for intermodal containers leaving the Port of Houston, Texas. Gulf Coast ports have experienced tremendous growth in the post-pandemic period as shippers work to serve the growing Texas market. The new intermodal services, most of which started on June 1, are railroads’ attempt to capture some of this additional volume.

The wildcard when it comes to intermodal volumes is if and how flows change in response to the railway merger of Canadian Pacific and Kansas City Southern (CPKC) that took effect earlier this year. Mexico is expected to post its second consecutive year of double-digit percentage intermodal volume growth in 2023 before downshifting to low single-digit results. That expected downshift could be altered by the new service offerings and partnerships announced in the wake of the CPKC transaction. Not only has CPKC added several new partners and beefed up its cross-border offerings, but other railroads responded by creating their own expedited intermodal services from Mexico into the upper Midwest.

These services could cause Mexican intermodal to outperform the 2% year-over-year growth expected and help it break its traditional status as an intra-Mexico (rather than cross-border) move. It is too early to adjust the base expectation higher or to know what the magnitude of the impact will be from the new services coming out of Mexico.

Better than expected

In a marked contrast with intermodal, carload volumes are performing better than expected through the first half of 2023 and are expected to grow for the full year. Carload volumes are expected to increase by 2% this year, in line with or slightly faster than overall gross domestic product (GDP) growth.

Coal, the largest carload sector by volume, has held up better than expected through the first half of the year, despite low natural gas pricing that should be denting domestic demand. It is expected that coal volumes will weaken as the year moves along, but its first half steadiness is already enough to likely ensure it avoids a negative outcome for the full year.

Chemicals volume started 2023 essentially in line with the prior year and five-year average levels, but it has shown some weakness as the end of the second quarter nears. This is worrisome not just for carload volume levels but also for what it could mean for the overall economy, as the base chemicals produced in this sector feed a number of manufacturing and industrial processes across the economy. New chemical facilities set to come online in 2024 and 2025 should boost volumes over the longer term, but the next few quarters could be a challenge.

Crushed stone, sand, and gravel traffic remains a bright spot for loadings as it has for the last six quarters. Federal and state infrastructure dollars should keep that sector moving forward for quarters to come as additional money is disbursed.

Metals and automotive are two more sectors that appear to have a solid foundation for carload growth over the next few quarters, as automotive production remains strong to rebuild inventory and meet demand.

Forest products traffic, however, is likely to be challenged in the next few quarters as lumber copes with the machinations of the housing market and pulp and paper appears to be settling into a pattern of lower volumes for a longer period of time.

Key factor: service

In general, slow-and-steady growth is expected to rule the day moving into 2024 for carload traffic, while intermodal faces headwinds for the next year. While those competitive pressures for intermodal will abate slowly over the next year, it will be 2024 before volumes truly turn around. Indeed, the competitive situation is not expected to place intermodal on level footing with its truckload competition until late next year.

In the long run, the primary factor determining rail companies’ success—whether intermodal or carload—will ultimately be whether carriers can deliver on the service expectations of their customers.

Service levels remain an area of dispute between carriers and shippers. While progress was made early in the year for both overall velocity for intermodal shipments and dwell time, these two metrics slipped back toward historical averages at the beginning of the second quarter and held there for most of the period.

Meanwhile railcars online, which measures the total number of railcars actively hauling freight in the North American rail system, remained stubbornly high until the end of the second quarter. Typically having a high level of railcars online is good, but only if they are supporting freight growth. Over the last few years, however, shippers have been adding and keeping railcars in the fleet to compensate for poor rail service (and not growth). So in this case, as service improves and freight growth is slow, railcars should be coming out of the fleet. We did begin to see this trend in the waning weeks of the second quarter, as railcars online came to a level that is in line with its historical average and closer to the levels other metrics had been holding.

The ultimate test of the health of the rail sector going forward will be whether carriers can improve service levels, as they will have a large impact on rail’s ability to reclaim and maintain market share from trucking in the intermodal and carload realms.

{kind=link}