Our site selection firm's first office was on Princeton, New Jersey’s Nassau St., overlooking the university and a few blocks from the former home of the father of the theory of relativity, Albert Einstein—who lived in Princeton from 1933 until his death in 1955. So, it seems fitting that in characterizing the current state of the warehousing sector, I lean heavily on the term “relative.”

First, the specter of an impending commercial real estate market crash is very much a reality. About $1.5 trillion in commercial mortgage debt is due by the end of 2025. With rising financing costs, along with stricter credit conditions and a fall in property values brought on by remote work, the risk of default has greatly increased. More than half of the $2.9 trillion in commercial mortgages will need to be renegotiated in the next 24 months when new lending rates are likely to be up by as many as 450 basis points.

Yet relative to other sectors of the commercial real estate industry, especially compared to the office sector, the warehousing market is doing quite well. The warehousing sector is doing an admirable job dodging the bullets of a slowed economy, rising interest rates, and the easing of pandemic restrictions that helped brick-and-mortar retail win back some of the business that it lost to e-commerce during the lockdowns.

In fact, fundamentals within the warehousing sector have remained fairly stable over the past year, and in many markets, they’re growing even stronger. That’s primarily due to sustained demand from online shopping, reshoring trends in manufacturing, and a shortage of prime, shovel-ready warehousing sites.

We are actually seeing double-digit rental rate hikes over the past year in the majority of U.S. distribution warehousing hubs, with all-time high rental rates being reached in many markets. Simply put, warehousing has not been turned upside down by the pandemic and rising interest rates like the office and retail markets have. Furthermore, these rising warehouse rents have not yet been reflected in many long-term leases. As a result, the next cycle of lease renewals will very likely increase the valuations of most warehousing assets.

Bellwether layoffs

Despite warehousing fighting the good fight amid 2023 upheavals in the overall commercial real estate market, the sector is not completely immune to the cooling economy. Real-estate analysis firm CoStar Group Inc. reported new warehouse construction fell by almost 25% in the most recent 2023 quarter, reaching the lowest level since the start of the pandemic.

Another sign is that warehousing employment has dropped significantly over the past year as companies slashed payrolls amid a downturn in the U.S. economy and talks of a recession. Warehousing companies have reduced employment by some 75,000 jobs over the past year, led by bellwether logistics giants Amazon, Walmart, UPS, and FedEx.

Recent companywide layoffs by Amazon total almost 30,000. Walmart, the world’s largest retailer, is also cutting back as it responds to falling consumer demand and concerns about a potential recession. The company plans to lay off more than 2,000 workers at distribution centers in Texas, Florida, and Pennsylvania as well as making additional cuts at other locations.

UPS plans to lay off some of its weekend drivers, and FedEx Freight announced it has gone through three rounds of layoffs since late 2022. FedEx is also consolidating its FedEx Express, FedEx Ground, FedEx Services, and other FedEx operating companies into what will be called the Federal Express Corporation. Combining these segments is part of an overall plan to trim its staff and expenses. All of these logistics giants are also automating operations greatly to speed up order processing and further trim headcounts.

Three trends to watch

Looking ahead we see three general trends that will affect the location of future warehouses: growing interest in logistics corridors, nearshoring, and continuing resistance to new warehouse construction from some local communities.

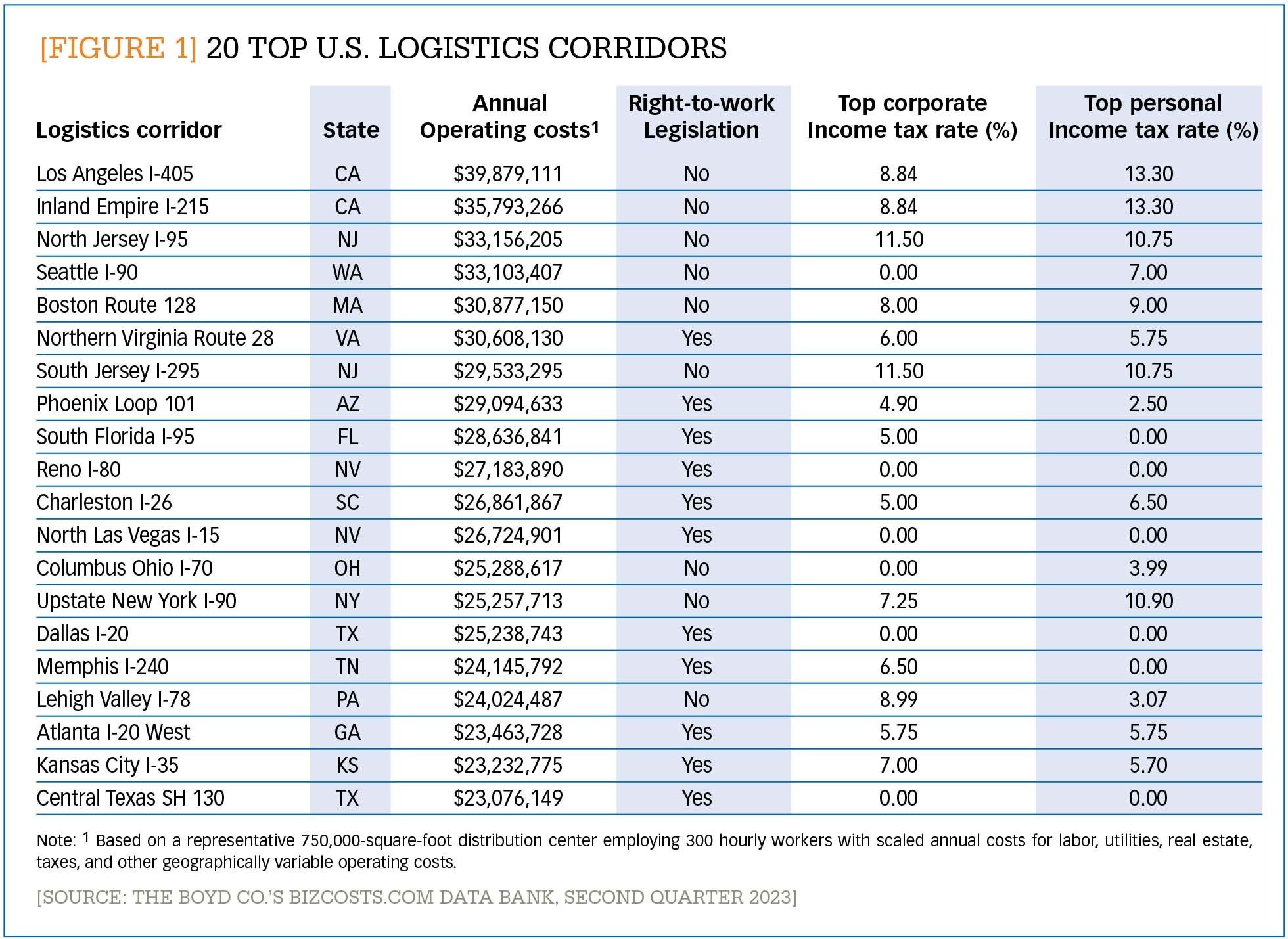

Logistics corridors. In spite of the big layoffs noted above, many of today’s site-seeking warehousing companies still want to access expanded labor markets as well as greater real estate options. As a result, site searches are increasingly focusing on prominent controlled-access highway corridors, especially in states offering attractive operating cost structures and low taxes. These corridors expand the geographic area that companies can draw upon for warehousing labor as well as shovel-ready sites for construction.

Some companies are shortlisting areas with smart highways that can monitor road conditions and communicate with vehicle navigation systems via smart infrastructure. Such technology can improve the speed of delivery and accommodate the future needs of electric trucks and emerging technologies like autonomous vehicles and hydrogen fuel cell-powered trucks. A good example is the SH 130 Corridor in Central Texas that utilizes futuristic technology, such as satellites, and links the high-growth areas of Austin and San Antonio. Figure 1 provides the location of these types of logistics corridors along with comparative warehouse operating cost data and state business climate information.

[FIGURE 1] 20 top U.S. logistics corridors

Enlarge this image

Nearshoring. Many industrial clients of Boyd continue to seek alternatives to manufacturing in and sourcing from China since the Trump tariffs in 2018 and the pandemic-induced global supply chain bottlenecks and geopolitical tensions. Today, the new federal incentives to manufacture and source in North America that were written into Biden’s Inflation Reduction Act (IRA) are fast-tracking the nearshoring movement even more.

At the same time, imports from Mexico are soaring, creating great demand for new cross-border logistics services. Foxconn, for example, which makes parts for Apple’s iPhones, now has major new production facilities in Ciudad Juarez, Mexico, and the automotive company Tesla just announced plans to open a new “gigafactory” in Monterrey, Mexico. Data from Uber Freight points to over 400 companies opening plants in Mexico in 2023, generating some $35 billion in new exports to the U.S. The magnitude of these exports is creating a new draw for supply chain investments in and near border states like Texas, Arizona, California, and New Mexico.

“Nimby-ism.” Our clients in the manufacturing sector have long faced anti-growth pressures from NIMBY (“not-in-my-backyard”) groups. Their objections are most often about noise, pollutants, and emissions. What is driving the NIMBY movement’s response to warehousing is different and has more to do with the sheer size and speed of the sector’s proliferation, especially in logistics hubs like New Jersey, Chicago, and California’s Inland Empire. This fast pace of change and the overpowering size of many of these new warehouses—one million square feet is becoming common—is unnerving to many.

In our firm’s home state of New Jersey, NIMBY-ites have long stressed traffic and stormwater runoff from warehouse roof tops and parking lots as major objections in places like the Millstone River Basin in Central New Jersey—home to millions of square feet of warehousing space in and around the popular Exit 8-A environs of the New Jersey Turnpike. The NIMBY movement here has recently upped the ante and is about to acquire a new arrow in its quiver. It is one that is likely to be adopted in other warehousing hubs around the country.

Local groups are now arguing that it would be appropriate to use American Rescue Plan Act (ARPA) funds to buy land where warehouses would otherwise be built on the premise that it was the pandemic that ignited the explosion in e-commerce and the subsequent sprawl of warehouses in New Jersey. They also say that protecting available land from warehouse use would underscore the value of open space, which was stressed during the pandemic.

Other warehouse NIMBY groups and like-minded lawmakers in other states are watching closely to how this all plays out in New Jersey. It would be quite the irony if federal monies that were designed to help businesses hurt by the pandemic were actually used to create new hurdles for their expansion and job creation. Irony, yes, but all things considered, a turn of events that would only be a minor speed bump in the ongoing growth and resiliency of the U.S. warehousing sector.

{kind=link}