AFTER YEARS OF DISRUPTION AND UNCERTAINTY, warehousing and third-party logistics providers (3PLs) ended 2022 on several positive notes as the market stabilized. 3PLs reported continued confidence due to new customer acquisition, e-commerce growth, and significant upticks in profitability, according to Extensiv’s annual “2023 State of the Third-Party Logistics (3PL) Industry Report” and its recent “3PL Warehouse Benchmark Report.”

These reports explore the state of the 3PL and warehousing industries, identifying the innovative approaches businesses are undertaking to adapt to the new normal. The reports found that even amid concerns over inflation, a recession, labor shortages, and global uncertainty, 3PLs outperformed in terms of order volumes versus the preceding years. More than 90% of 3PLs reported increased order volumes in 2022, up from 2021 when 85% reported increased volumes and 2020 when 79% reported increased volumes. New customer acquisition is the most significant driver of order volume growth, with 81% of respondents citing it as a primary reason, followed by diversifying fulfillment types (42%) and increases in e-commerce ordering (31%).

3PLs also saw higher revenues as many leveraged increased market demand to boost profitability. When surveyed about their financial performance over the past year, 81% reported improvement, with 38% reporting a significant growth of more than 25% in profitability. Meanwhile, 31% indicated moderate growth in profitability ranging from 10% to 24%.

Amidst these positive developments, the 3PL industry also faces challenges. Top among them (perhaps unsurprisingly due to upward pressure on warehousing rents and a tight labor market): managing costs, finding and retaining workers, and operational efficiency.

Three key trends reveal how 3PLs must embrace the opportunities presented by these market changes to help their customers optimize their supply chains: omnichannel fulfillment, space constraints, and digital automation.

1. Omnichannel fulfillment

Customers today expect to have a unified shopping experience across all of a company’s retail channels, whether it's online, in a physical store, or any combination of the two, such as “buy online pickup in store” (BOPIS) or curbside and locker pickup. To support their clients’ sales channels, 3PLs need to embrace an omnichannel fulfillment strategy. Extensiv’s survey showed that 3PLs supporting omnichannel fulfillment saw 13% more growth than those offering more limited fulfillment. Furthermore, 18% of 3PLs performing omnichannel fulfillment saw a 50% increase in profitability over the prior year, which is 33% higher than the 17% average increase for 3PLs that do not offer omnichannel fulfillment.

A successful omnichannel fulfillment strategy requires:

● Real-time channel performance monitoring that provides visibility and evaluation of key performance indicators (KPIs).

● A single platform to manage cross-channel fulfillment, which increases efficiency and consistency across all channels.

● Streamlined returns management or reverse logistics capabilities. Prioritizing reverse logistics in an omnichannel strategy is a realistic goal that aligns with a greater mission to remove friction from whatever parts of the fulfillment process matter most to consumers.

There are many benefits to having a robust omnichannel fulfillment strategy. First, having cross-channel fulfillment can help streamline and improve order management across all channels, simplifying the process from warehousing to packing to delivery. It also improves customer and consumer satisfaction. Omnichannel fulfillment meets the disparate needs of consumers through their preferred channels, while making brands look good and creating a loyal consumer base.

2. Space constraints

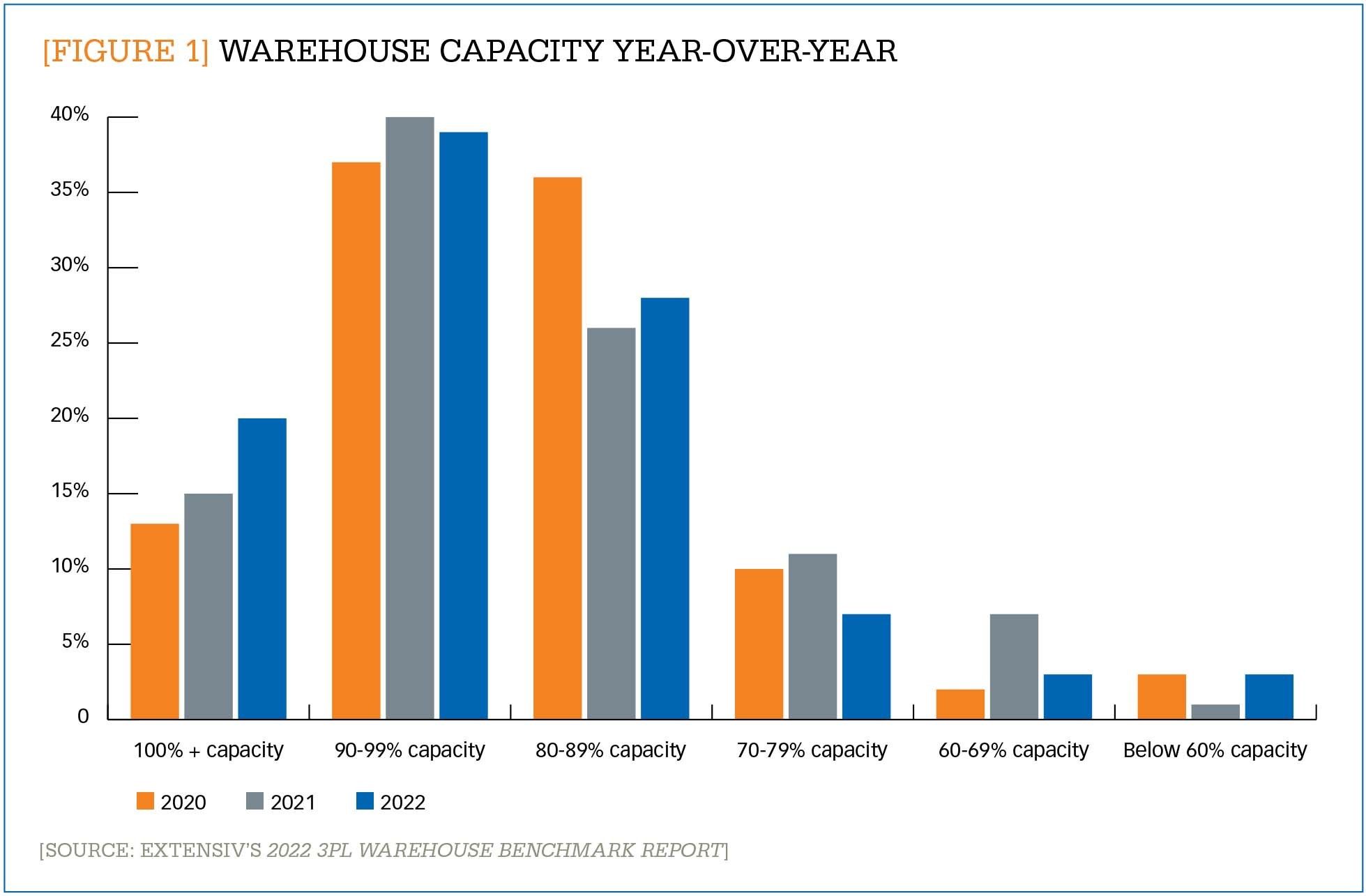

A significant challenge that may limit 3PL growth is the current scarcity of warehouse space due to low vacancies and high rents. Over a third (35%) of 3PLs who responded to our survey think finding available warehouse space will be one of their biggest challenges. Currently, 20% of 3PLs report operating beyond 100% capacity (a 33% increase from 2021), while almost 40% report capacity of 90% to 99%. (See Figure 1.) Nearly 2 out of 5 (39%) 3PLs report that adding warehouses in new locations is one of the most significant opportunities in the coming year. These challenges are exacerbated by the fact that brands are asking 3PLs to warehouse slow-moving inventory surpluses.

[FIGURE 1] Warehouse capacity year-over-year

Enlarge this image

3PLs are undertaking a variety of approaches to tackle space constraints, including:

● Pricing long-term storage at a higher rate to persuade customers to reduce the stock of slow-moving inventory and preserve valuable warehouse space.

● Using “micro-warehouse” space in densely populated urban areas. Micro-warehousing helps 3PLs expand available square footage by adding smaller warehouses to their real estate portfolio. This strategy also allows them to get inventory closer to consumers, significantly decreasing delivery times and costs.

3. Digital automation

Digital automation is the foundation for establishing continued effective and efficient processes within the supply chain. Businesses are leaning into it: 93% of shippers reported that data-driven decision-making, made possible by digital automation, is critical to the success of supply chain management.

Although there’s widespread recognition that automation can streamline operations and boost productivity, technology implementation and integration continue to vex 3PLs. In 2021, 42% said technology implementation was their most pressing business challenge. The 2022 survey showed effectively no improvement in this area, as that number only dropped by 1%, down to 41%. Implementing the right technology stack—one that aligns easily with target industries and creates flexible and scalable workflows—is at the heart of this task. It requires a holistic approach that doesn’t rely on a sole piece of software, like a warehouse management system (WMS), to solve the problem single-handedly. A holistic approach instead builds an entire digital ecosystem that is primed to cut hard and soft costs, increase visibility, and improve the consumer experience.

The technologies with the highest current implementation are WMS, with 87% of 3PLs having implemented it; order management systems (52%); mobile barcode scanning (51%); and electronic data interchange (44%). For 2023 and beyond, 3PLs plan to focus on technologies that support increased profitability and operational efficiency. The top three planned implementations are billing and invoicing (32%), mobile barcode scanning (27%), and reporting and analytics (27%).

To retain happy customers and consumers, 3PLs need to evaluate technologies to build a long-lasting digital foundation. Many tools that have already been implemented haven’t been fully used or optimized. Many 3PLs would benefit from training employees to get the most out of those automation investments. Only when technology and teams complement each other do businesses see increased productivity and revenue growth.

Moving forward

Mid-2023 finds 3PLs looking to optimize their omnichannel fulfillment processes, leverage digital automation, and create innovative warehousing strategies to respond to capacity constraints. Continued proactive management and leaning into automation will mitigate these challenges while positioning 3PLs to weather other market impacts, including labor shortages, inflation, and a potential recession.

{kind=link}