The container shipping industry experienced an unparalleled surge during the pandemic; however, in 2023 so far, the market has been anaemic due to an oversupply of capacity and sluggish demand.

Freight demand has declined significantly after reaching its peak in September 2021, as consumers reduced their spending on luxury goods and the global economy grappled with inflation and rapid interest rate hikes. As a result, spot rates on significant trade routes have dropped rapidly.

Although shipping lines reported strong profit margins in Q1 of 2023 due to pre-negotiated contract rates, we anticipate a substantial decrease in these margins. As contract negotiations are currently underway, revised rates will soon come into effect, impacting the profitability of shipping lines in the second half of 2023 and throughout 2024.

While the drop in demand and rates are having an immediate effect on carriers’ profitability, the forthcoming influx of new ships will have a significant impact on the market for years to come.

Freefalling prices, surging costs

The year 2023 started with a significant oversupply of containers and high uncertainty in the market—which led to substantial container-price erosion. The average container prices have been freefalling, and there are no signs of revival as we approach the busiest period in the shipping industry. It is quite evident that this year’s peak season is almost invisible.

Container prices in June 2023 for major supply chain markets like China, Europe, and the U.S. reached their lowest average levels when compared to the same month in both 2022 and 2021. This decrease in container prices may suggest an additional burden on the profitability of shipping companies.

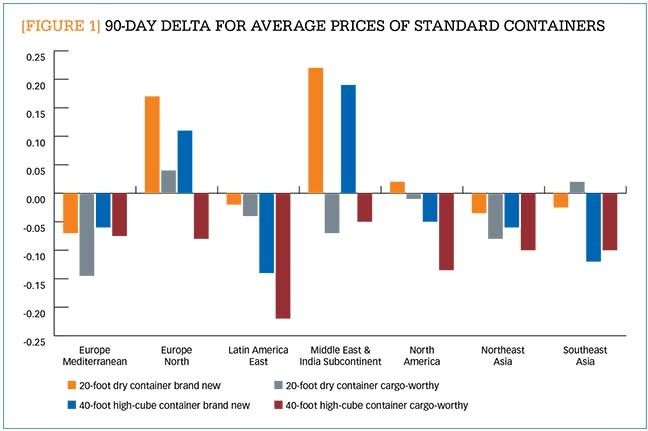

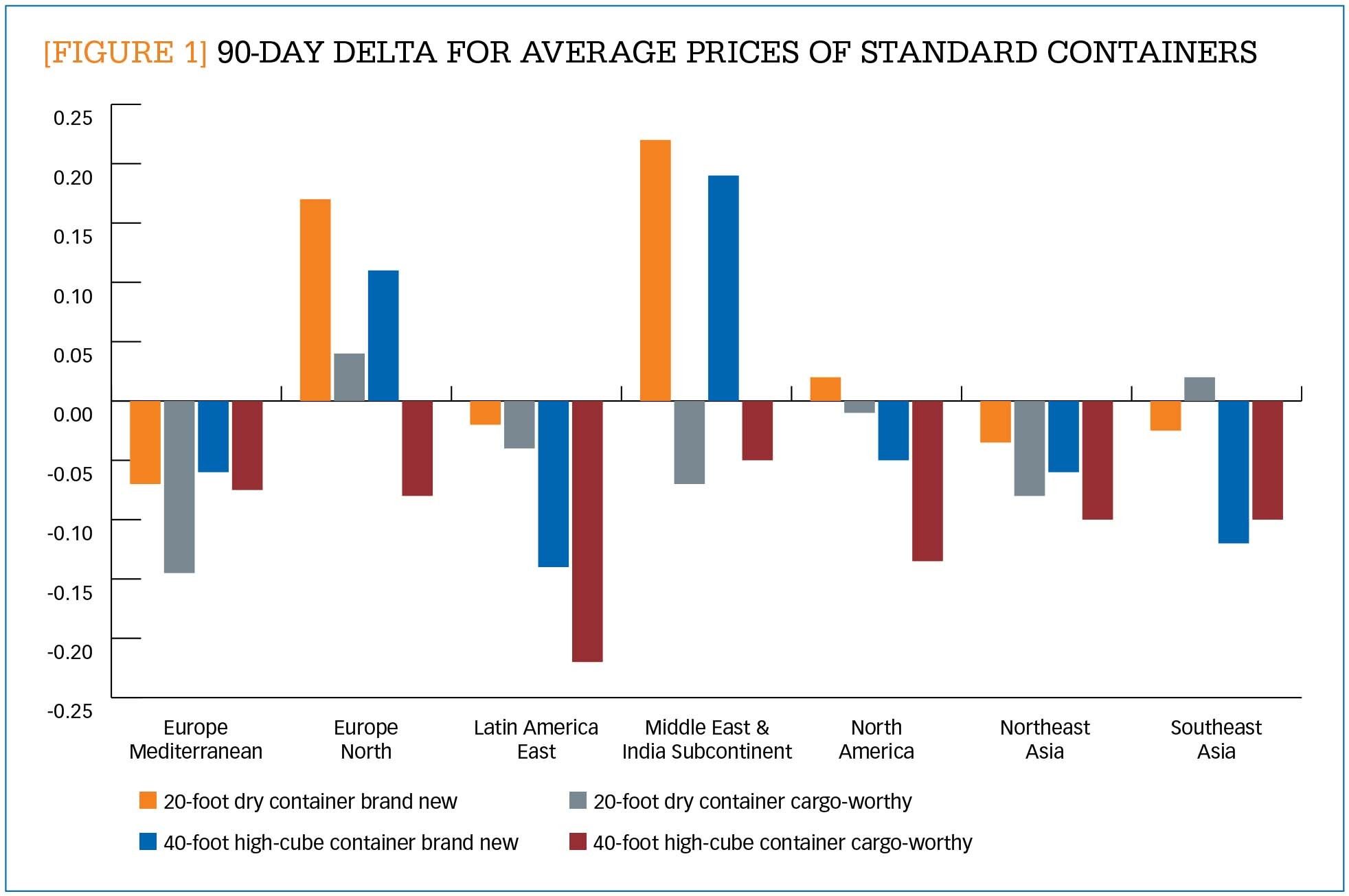

A recent study conducted by Container xChange examined the trends in average container prices for standard containers (new and cargo-worthy) during the second quarter of 2023 (April to June). The study found no significant rise in average container price for either new or cargo-worthy containers during Q2. Figure 1 shows the price development (or “delta”) of average containers on key routes during Q2 2023. Only Northern Europe and the Middle East and Indian Subcontinent regions experienced slight increases in prices. The rest of the regions showed negative (or near flat) trends for standard containers.

[FIGURE 1] 90-day delta for average prices of standard containers

Enlarge this image

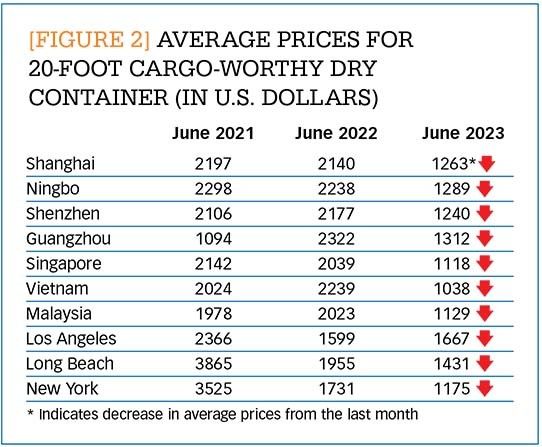

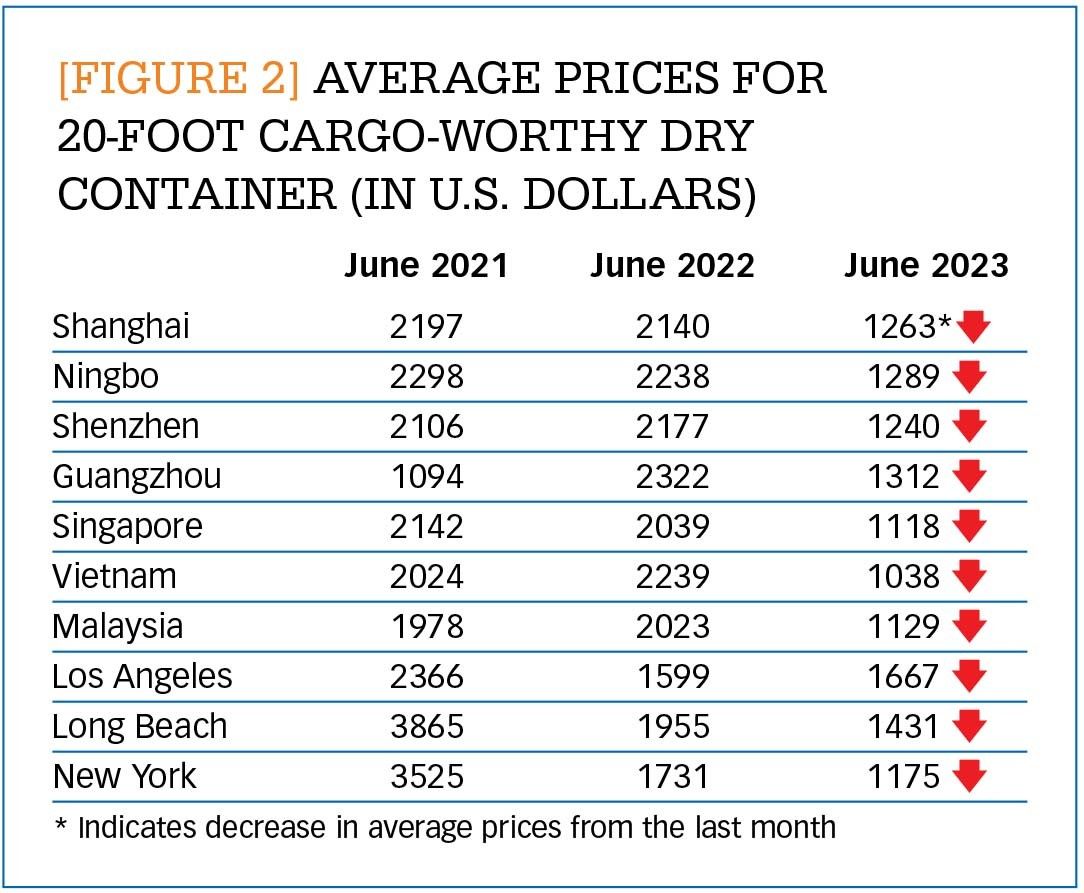

Figure 2 compares average container prices for some of the busiest ports in the world from the Container xChange platform. The prices have fallen to the lowest levels in the last three years of comparison. Clearly, the data indicates poor demand for containers in 2023 up to June.

[FIGURE 2] Average prices for 20-foot cargo-worthy dry container (in U.S. dollars)

Enlarge this image

While container prices have been dropping, operating expenses for container lines have been rising. The main reasons for this increase have been soaring energy prices and labor expenses, neither of which are expected to decrease soon. Additionally, the shipping industry is facing high demurrage and detention charges and various fees related to container storage and transfers. The shortage of container depot space also remains a persistent struggle, with depots charging exorbitant fees that pose additional burdens. Our customers have informed us about terminal tariff hikes in Europe and India, causing further concerns for carriers.

These rising operating costs will likely influence spot freight rates. In the intensely competitive container shipping industry, the minimum price offered in the market tends to align with variable costs. Over the years, variable costs in container transportation have risen by approximately 15% to 25% since 2019, varying depending on the specific trade route. Consequently, the lower threshold of freight rates set by carriers has also increased within the range of 15% to 25%. This presents challenges for shippers, as they now encounter higher variable costs when transporting goods. Despite the significant decrease in average container rates from 2021 to 2023, with a reduction of nearly 85%, the underlying variable costs remain elevated. As a result, it is unlikely that spot freight rates will experience a significant additional decline, as contract rates still have room for further depreciation and remain relatively stable.

Capacity takes center stage

The container shipping market’s recent good years prompted a surge of orders for new and larger container vessels. Research conducted by the maritime consulting company Drewry and the financial services company ING Group estimates that fleet capacity will be increased by 27% due to the new vessels being delivered between 2023 and 2025.1 More than 700 ships are expected to be delivered between 2023 and 2024, with an additional 150 coming in 2025, according to ING and Drewry. Among these orders, 45% are for Neo-Panamax size vessels (12,500-18,000 TEU or twenty-foot equivalent unit) and another 20% are for ultra-large container vessels (ULCV). Feeder vessels (up to 3,000 TEU) make up just over a third of the ordered vessels, representing 8% of the total capacity. The report says these investments are being driven not just by expected future demand but also by a desire among carriers to expand their fleet and introduce larger and more efficient vessels.

Indeed, it is unlikely that the additional capacity will be absorbed by increased demand any time soon. Moreover, as port congestion eases, previously blocked capacity is gradually being freed up. These supply chain improvements could significantly improve supply; especially considering that at the worst point in early 2022 up to 15% of capacity was tied up at the ports. The significant influx of new capacity, combined with sluggish trade growth, could potentially disrupt freight rates. And yet, we do not expect to see extensive order cancellations, as stakeholders will aim to preserve the efficiency gains they have made per unit carried.

That’s not to say that we won’t see capacity cuts. Container liners operating on the Asia–U.S. trade route, for example, have implemented a 14% reduction in capacity due to persistent weak demand and surplus capacity. And more capacity cuts may be on the way. While some container lines and analysts predicted a surge in cargo demand in August—driven by dwindling inventory stocks in the U.S. and the aftermath of recent port operation delays caused by the International Longshore and Warehouse Union (ILWU) strikes—that optimism has not been reflected at the ground level. Shippers, for their part, continue to observe weak demand, with only a slight increase in less-than-container load (LCL) shipments, indicating a lack of strong demand for full container load (FCL) shipments. Furthermore, many shippers have already adopted online spot rates, indicating a shift in their preferred approach to freight rate negotiations. To achieve rate stability, carriers will need to make more substantial capacity cuts, which will test their determination as they strive to push for rate increases in August.

Effective capacity management becomes crucial considering these circumstances. The container liners response to this uncertain scenario is yet to be seen. So far, liners have been driven to secure market share. Vessel utilization levels have already decreased (down to 75% in the first quarter), and freight rates have demonstrated fragility in the second quarter, with the potential for further decline. Given that container liners are financially strong, these circumstances could easily evolve into a prolonged price war.

Note:

1. Rico Lumen and Oleksiy Soroka, “Global container shipping outlook: pressure mounts amid flood of new capacity,” ING Think, ING (June 28, 2023): https://think.ing.com/downloads/pdf/article/global-container-shipping-outlook-pressure-mounts-amid-flood-new-capacity

{kind=link}

{kind=link}