Global supply chains have faced a decade of disruptions. The most significant have included the U.S.–China trade war, the COVID-19 pandemic-era consumer goods boom, and the Russia-Ukraine war. While supply chain activity has been more normalized during 2023, there are significant risks heading into 2024, including new industrial and environmental policies and possible labor actions.

Willing to make the investment?

Supply chains need to be more resilient, but questions remain over whether corporations and their investors are willing to make the investments necessary to fortify them. S&P Global Market Intelligence data indicates that gross operating profit margins for manufacturers globally are expected to fall to 10.4% of sales in 2024 from 10.7% in 2022. The decline is expected to be particularly stark for the computing and electronics sector and domestic appliance manufacturing. At the same time, capital expenditures are forecast to exceed gross operating profits by 5% in 2024 after being equal to them in 2022. Reinvesting in capital stock may take priority over spending on supply chains.

One tactic that companies used to hedge against disruption during the pandemic era was to keep more product on hand via elevated inventories. The appeal of this approach is its organizational and operational simplicity. The drawback is that every dollar in the warehouse is a dollar not paying off debt, increasing the dividend, or being invested in growth opportunities. That’s particularly pertinent in a high interest rate environment, and companies may be pulling back from a “just in case” inventory strategy.

Data from the S&P Global Purchasing Managers’ Index (PMI) indicate that inventory stocks for finished manufacturing goods were in retreat for eight of the first nine months of 2023.

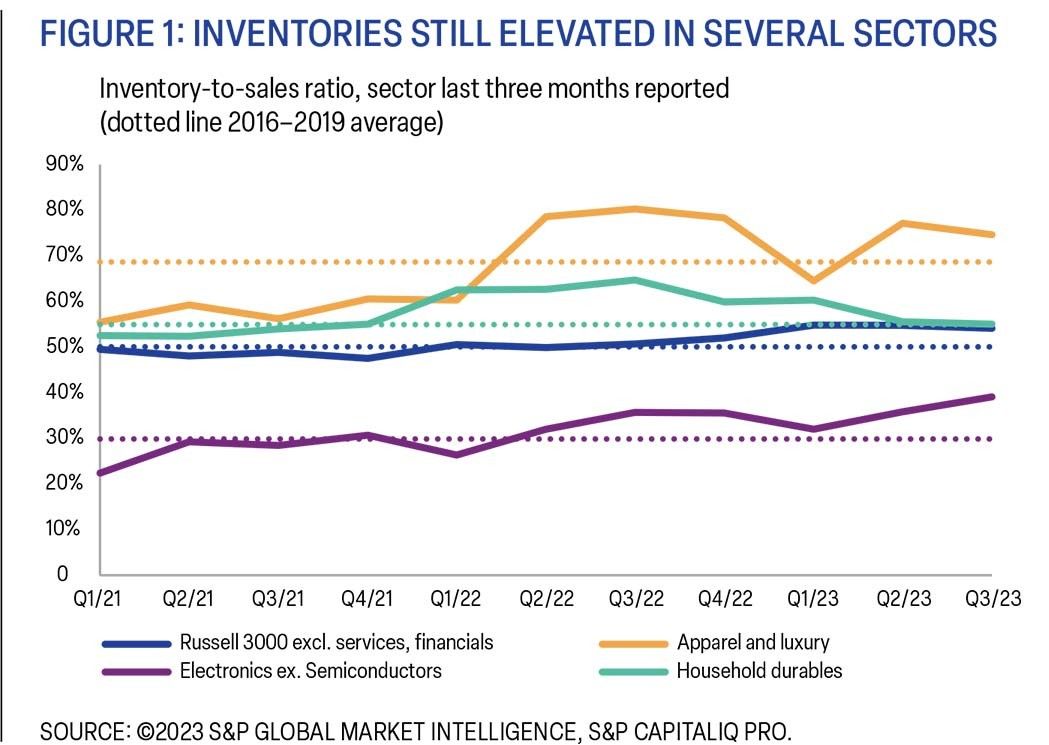

The evidence of “destocking” from corporate financial data, however, is mixed. The inventory-to-sales ratio for the Russell 3000 Index, which measures the performance of the largest 3,000 U.S. companies, seems to elevated, coming in at 54.1% on a trailing three-month basis as of September 30 compared to 50.1% on average for the 2016 to 2019 period (see Figure 1). However, that elevated level is not necessarily evidence of a change in inventory formation practices (such as a move to “just in case” instead of “just in time”), as it is below the 54.8% peak reached in March.

Furthermore, when the index is broken down into its subsections, you see that the increase is caused by just a handful of sectors. While the apparel and electronic sectors are up, household durable goods are closer to balance.

Backsliding on efforts

Another example of some companies’ reluctance to spend on supply chain resilience is the apparent backsliding in supplier diversification efforts. While supplier diversification can reduce the inherent risk of a supply chain, it can come in and out of fashion depending on the need for cost reductions.

Figure 2 shows that the number of suppliers per ultimate consignee for the top 500 U.S. seaborne industrial importers increased by 13% in 2021 compared to 2019. This increase indicates that industrial companies were using more suppliers as a way to deal with the increase in supply chain disruptions during that period.

That trend, however, broadly started to reverse itself in 2022 as the number of suppliers fell below pre-pandemic levels in the 12 months through September 30, 2023. There are a few sectors, such as auto and electronics, that have bucked this trend. But in general, we expect to see less supplier diversification in 2024 as companies push more orders to fewer suppliers in order to get better prices.

Some resilience at (slightly) lower cost

In the absence of significant funds to spend on inventory increases or supplier diversification, firms may look to technological and organizational fixes to provide a degree of resilience at a lower up-front investment cost.

For example, artificial intelligence (AI), if deployed in the correct manner, could provide predictive probabilities of future disruptions. It also may be able to shorten recovery times by indicating where there should be inventory redundancies based on historical data. Other uses include assisting with scenario planning operations and providing optimal distribution routes and alternates based on past and real-time asset data.

More traditional routes to improving organization agility can also help increase supply chain resilience as well as reduce costs. Such short-term, flexibility-based solutions could include: writing contracts that include burden-sharing for unexpected events with suppliers and customers; ensuring production resources can be rapidly retasked from one product to another if demand planning fails; and using alternate components when there is a part or supply shortage.

Additionally, companies that maintain close, ongoing relations with workers may be inherently more resilience than some of their competitors. The ongoing round of labor unrest shows the cost of not staying close to employees.

In summary, while supply chains have returned to normal from an operational perspective in most industries, the roster of risks in 2024 and beyond mean investments in resilience are more important than ever. Evidence from financial and supply chain data suggests firms may not have the ability or willingness to make big-ticket investments in inventory or having multiple sources of supply. Instead, a focus on lower cost investments in technology, staff and customer relations, and flexible operations may be a cheaper route to providing a modicum of resilience.