While many executives talk about supply chain excellence, almost all would agree it's easier to talk about than to define.

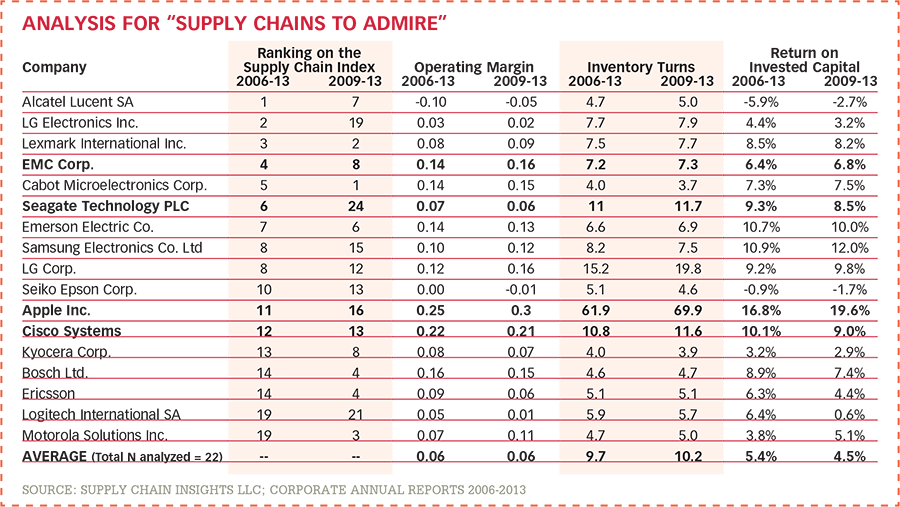

In 2014, a small team at the research company Supply Chain Insights started a project to define excellence in a more objective and quantifiable way. After studying balance sheet patterns for 2,000 companies, we believe that supply chain excellence is defined both by improving year-over-year financial performance versus a peer group and by outperforming the industry on a portfolio of metrics that correlate closely to market capitalization. The metrics we selected were inventory turns, operating margin, and return on invested capital (ROIC).

While we often see companies performing well in one of the three metrics, we believe that supply chain excellence is based on the ability to drive improvement on the complete portfolio—improving all three metrics together. To help companies assess whether they are making progress on improving supply chain performance, we created the Supply Chain Index. The Index provides a score, which represents a company's ability to do three things: balance growth and return on invested capital (growth), improve both operating margin and inventory turns (strength), and provide reliable, predictable operating margins and inventory turns (resiliency). (For more information about the Supply Chain Index, see the Q3/2014 Supply Chain Quarterly article, "The Supply Chain Index: A new way to measure value.")

This is the first in series of columns looking at how companies in a specific industry group perform against these metrics. We are starting with the high tech and electronics industry.

In our general analysis, we were surprised to find how few companies were making balance sheet improvements. In our research, we found that nine out of 10 public companies were not progressing. They could drive improvement in either operating margin or inventory turns, but not both together. Additionally, we discovered that many companies were going backwards, with slippage in metrics performance in two of the key metrics of ROIC, as well as in costs (measured by operating margin), customer service, and inventory. For some, this was caused by uncontrolled complexity, while for others it was the lack of a clear operating strategy.

Surprisingly, the high-tech industry segment has made more progress than other industries in being able to drive improvement in all of the performance metrics. The industry's success has come despite significant obstacles, such as shorter lifecycles, deterioration in prices, rapid advancements in technology, and major shifts in product portfolios. The high-tech industry exemplifies the saying, "when the going gets tough, the tough get going."

Who did it best? To identify the top performers, we developed a list of companies that were performing at levels above those of their peer group on the portfolio of metrics. Based on both supply chain improvement in this portfolio of metrics (as defined by the Supply Chain Index ranking) and performance on ROIC, operating margins, and inventory turns, Apple, Cisco Systems, EMC, and Seagate make Supply Chain Insights' "Supply Chains to Admire" list in high tech and electronics (see the accompanying table), while Intel and TSMC make the list in the semiconductor industries.