Last October’s announcement by online retail behemoth Amazon that it is testing Agility Robotics’ humanoid robot, Digit, in its warehouses caused a stir in the global media, sparking numerous news articles and debate about the ethics of using robots to replace human workers. But does Amazon’s announcement point to a rapid adoption of bipedal robots in the near future?

The concept of humanoid robots is not new. In fact they date back at least as far as Ancient Greece, with the mechanical Servant of Philon1, a humanoid automaton that could pour and mix wine and water. However, there has been a sharp rise in recent years in the number of companies developing and trialing humanoid robots, particularly within the warehouse sector. Digit, which can grasp and lift objects, is going to start by moving empty tote boxes as part of Amazon’s efforts to automate its warehouse operations. Similarly, Figure and Boston Dynamics are prototyping humanoid robots for use in distribution centers. Tesla’s Optimus Robot also looks promising for warehouse applications, as it can self-calibrate its arms and legs and has the capability to sort objects fully autonomously. Additionally, the commercial launch of Apollo by tech startup Apptronik is expected to take place in late 2024, and videos have already shown it walking, case picking, palletizing, and unloading trailers.

Yet, in spite of the current chatter around the technology and the flurry of pilots and prototypes, change is unlikely to happen overnight. Most pilot projects take months or even years to reach completion, and rollouts tend to happen in incremental stages. Furthermore, our feeling is that, although we are already starting to see humanoid robots appear in warehouses, some obstacles still exist, particularly in regard to acceptance of humanoid robots by their human co-workers.

Are bipedal robots inevitable?

Warehouse automation solutions in general have been in place for decades, carrying out many physically demanding, menial jobs. For example, automated storage and retrieval systems (AS/RS) are already widely used alongside human workers to deliver much faster rates of order picking and to increase throughput. Furthermore, over the past five years, there has been a steady rise in the development and adoption of mobile automation solutions for the warehouse, such as automated guided vehicles (AGVs) and autonomous mobile robots (AMRs).

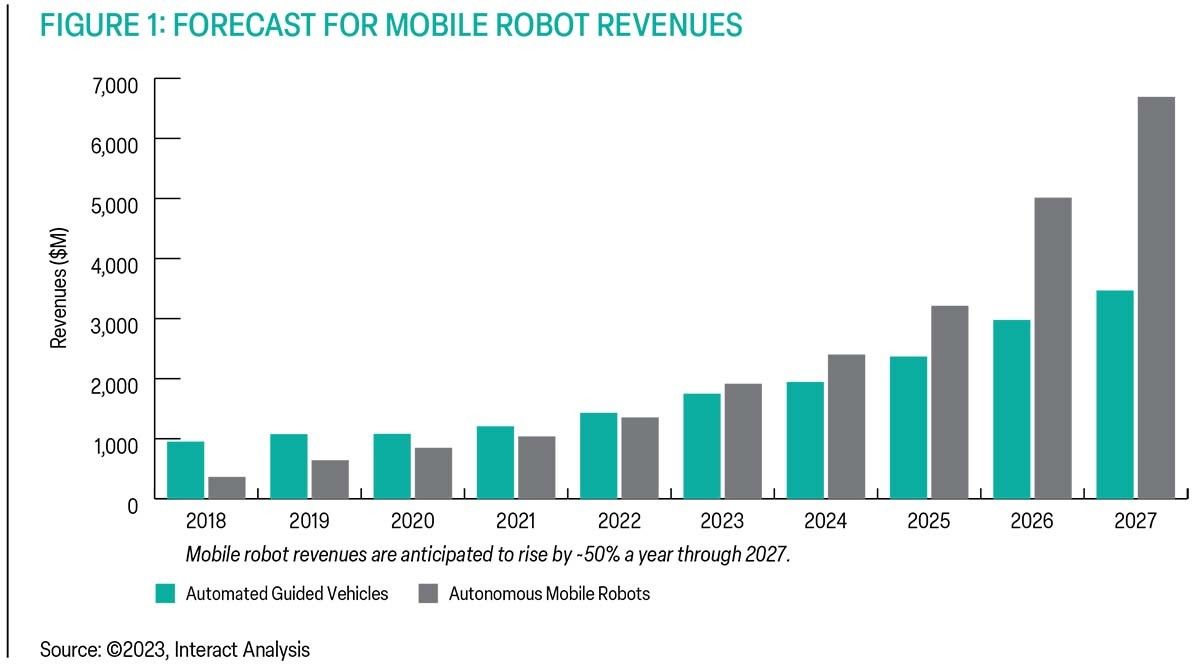

This surge in demand has been in part fueled by the ongoing labor and skills shortages blighting the industry. Research by Interact Analysis shows scarcity of labor remains the biggest driver of demand for mobile robots and the impact of shortages is becoming more acute. As a result of this and other drivers for mobile automation (such as increasing labor costs, e-commerce growth, and the shift to flexible manufacturing), Interact Analysis forecasts shipments of mobile robots will continue growing at an annual rate of approximately 50% until 2027.2 (See Figure 1.)

Similar to AMRs and AS/RS, humanoid robots may simply be another evolutionary stage in the development of technology for the industry. Because of their ability to move and interact with their environment in a similar way to an actual person, humanoid robots have the potential to meet some very specific needs of the modern warehouse while also offering a very different value proposition to traditional robots. Warehousing involves repetitive and physically demanding menial work that often has seasonal peaks in demand. This work often involves interacting with a variety of different products that lack standardization and a uniform shape and size. While traditional robots are very good at doing the same repetitive work over and over again, humanoid robots can be more adaptable (in a similar way to humans) and therefore can be applied to multiple different tasks throughout a warehouse.

Early applications for bipedal robots are likely to include trailer unloading, which is simple, physically demanding, and repetitive, but difficult to complete using traditional robots. While they tend to operate at a slower pace than traditional robots, humanoid robots also offer the potential to be introduced to the workforce during peak periods without requiring substantial operational changes to warehouse workflows or alterations to the layout of the warehouse. In this way, humanoid robots offer greater flexibility than other materials handling solutions, as they can be dropped into existing supply chains alongside human workers. Humanoid robots are able to take on jobs that are unappealing and take a toll on the human body (such as trailer loading/unloading), freeing up employees for more complex, less physically demanding, and more interesting tasks. Additionally, unlike traditional robots, humanoid robots possess a level of mobility and dexterity that allows them to take on multiple different tasks across facilities, workflows, and applications, and to handle the variety of objects found in a typical warehouse.

Given these potential benefits, will humanoid robots see the same sort of growth rate as AMRs and other robotics solutions? That depends on how well they are able to overcome the barriers to adoption. The largest barrier is the high cost of humanoid robots, which means businesses will currently have to wait a long time to achieve a return on their investment. However, another significant barrier is the “uncanny valley” effect, or the feeling of unease or revulsion people feel when they encounter a human-like robot, and the personification of role replacement humanoid robots represent.

Is our unease surmountable?

At the time of Amazon’s announcement, concerns were raised about humanoid robots displacing human workers.3 Similar concerns have been raised in the past about other robotic technology, such as AMRs. But anecdotal evidence indicates people like working alongside AMRs, where the robot carries out menial, physically demanding work, while they act in a supervisory capacity.

However, the very reasons humanoid robots are capable of working so well alongside human workers are also one of the biggest stumbling blocks for their rapid and widespread adoption: their ability to move and function similarly to a human. From the automaton in ETA Hoffman’s nihilistic 1815 short story “The Sandman” to movies and TV shows such as Terminator, Avengers: Age of Ultron, Blade Runner, and Westworld, humanoid robots have been depicted as problematic and, in some cases, apocalyptically so. Coupled with this, humanoid robots appear to cause greater resentment than other forms of autonomous mobile robots because they are role replacement personified. After all, few humans want to be outpaced, outlifted, and outperformed by a robot that looks like a person.

Responding to concerns about job losses, Amazon has emphasized the “hundreds of thousands of new jobs” that have been created as a result of its use of robotic systems, including “700 categories of new job types in skilled roles,” with robots being used to replace the most “menial, mundane, and repetitive” tasks.

Ultimately, companies are unlikely to be deterred from deploying humanoid robots by their appearance. Although Digit walks on two legs and is capable of lifting and moving objects with its arms, we are far from a dystopic future in which sentient robots blend seamlessly into the human population. The bipedal robot has been designed specifically for warehouse automation where the focus is on increasing throughput and filling labor gaps, rather than the complexities of human thought and movement. Indeed, Amazon describes Digit as “a mobile manipulator solution,” and Tye Brady, chief technologist at Amazon Robotics, told reporters in Seattle that people are “irreplaceable” to the company because of their “ability to think at a higher level, the ability to diagnose problems.”

Promising but still some way off

At Interact Analysis, we have charted the steep rise in demand for warehouse automation technology. Many facilities are still operating manually, but companies worldwide plan to increase investment in automation over the coming years. Skills and labor shortages are showing no signs of stopping within the materials handling industry, and mobile robots are being utilized already in a range of different settings. They often provide a solution to repetitive, physically demanding, uncomfortable, and dangerous jobs.

In addition to this, our research indicates the scalability and flexibility to use humanoid robots within existing warehouse operations alongside human workers could provide a unique answer to ongoing skills and labor gaps. There will always be inertia to change regardless of what the automation solution looks like, and it is too early to tell whether in the long-term bipedal robots will become widely used in warehouses. However, it is certainly a possibility. It will be dependent on the success of early pilots, whether ethical concerns can be overcome, and whether other robotics technology is found to be better suited to specific tasks. Amazon has always been a leader in its use of robotics, with the rest of the industry tending to follow (or fail!), so this pilot could be the catalyst for the wider rollout of humanoid robots in the future. Although competition to develop affordable and effective models is growing, the widespread use of humanoid robots in warehousing, if it happens, is clearly some way off.

Notes:

1. G. Georgiopoulos and Kyvrikosaios, D. “Robots, clocks and computers: How Ancient Greeks got there first,” Reuters (Feb. 18, 2020): https://www.reuters.com/article/us-greece-technology-museum-idUSKBN20C1UC/

2. A. Sharma and J. Zhang, “Mobile Robots–2023: An analysis of AGV & AMR demand in logistics and manufacturing applications,” Interact Analysis (2023): https://interactanalysis.com/research/mobile-robots/

3. See for example: C. Jones, “Fears of employee displacement as Amazon brings robots into warehouses,” The Guardian (Oct. 19, 2023): https://www.theguardian.com/technology/2023/oct/18/amazon-robot-warehouses-digit-workers and S. McCallum and C. Vallance, “Amazon trials humanoid robots to ‘free up’ staff,” BBC News (Oct. 19, 2023): https://www.bbc.com/news/technology-67163680